Report: Warehouse Automation Technologies - Market Analysis, Key Players, and Investment Trends

Executive Summary

The warehouse automation industry has emerged as one of the most dynamic and rapidly evolving sectors in modern logistics and supply chain management. As we advance through 2025, the convergence of artificial intelligence, robotics, and advanced material handling systems is fundamentally transforming how goods are stored, retrieved, and distributed across global supply chains. This comprehensive report examines the current state of warehouse automation technologies, analyzes market dynamics, profiles key industry players, and provides detailed insights into investment trends shaping the future of automated warehousing.

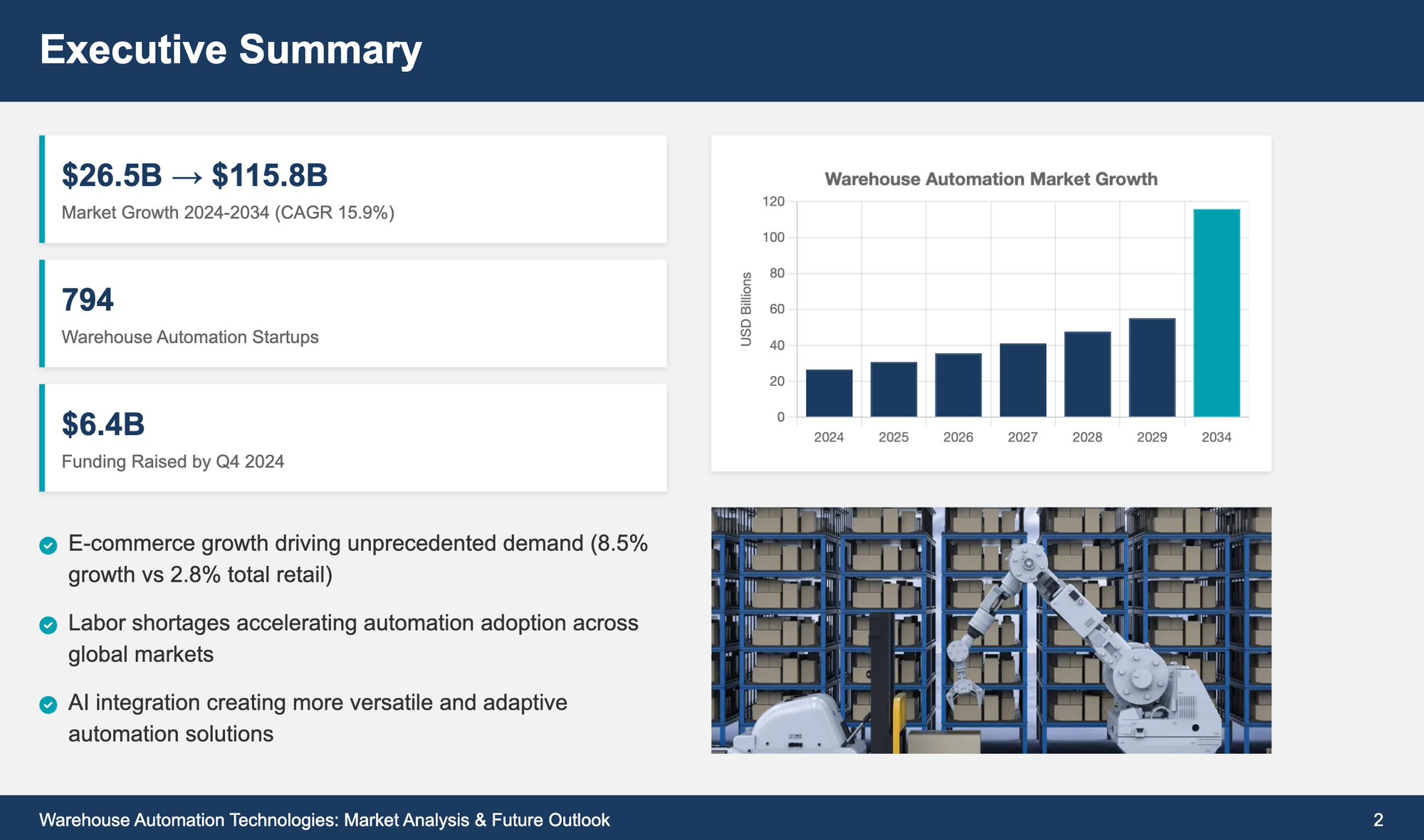

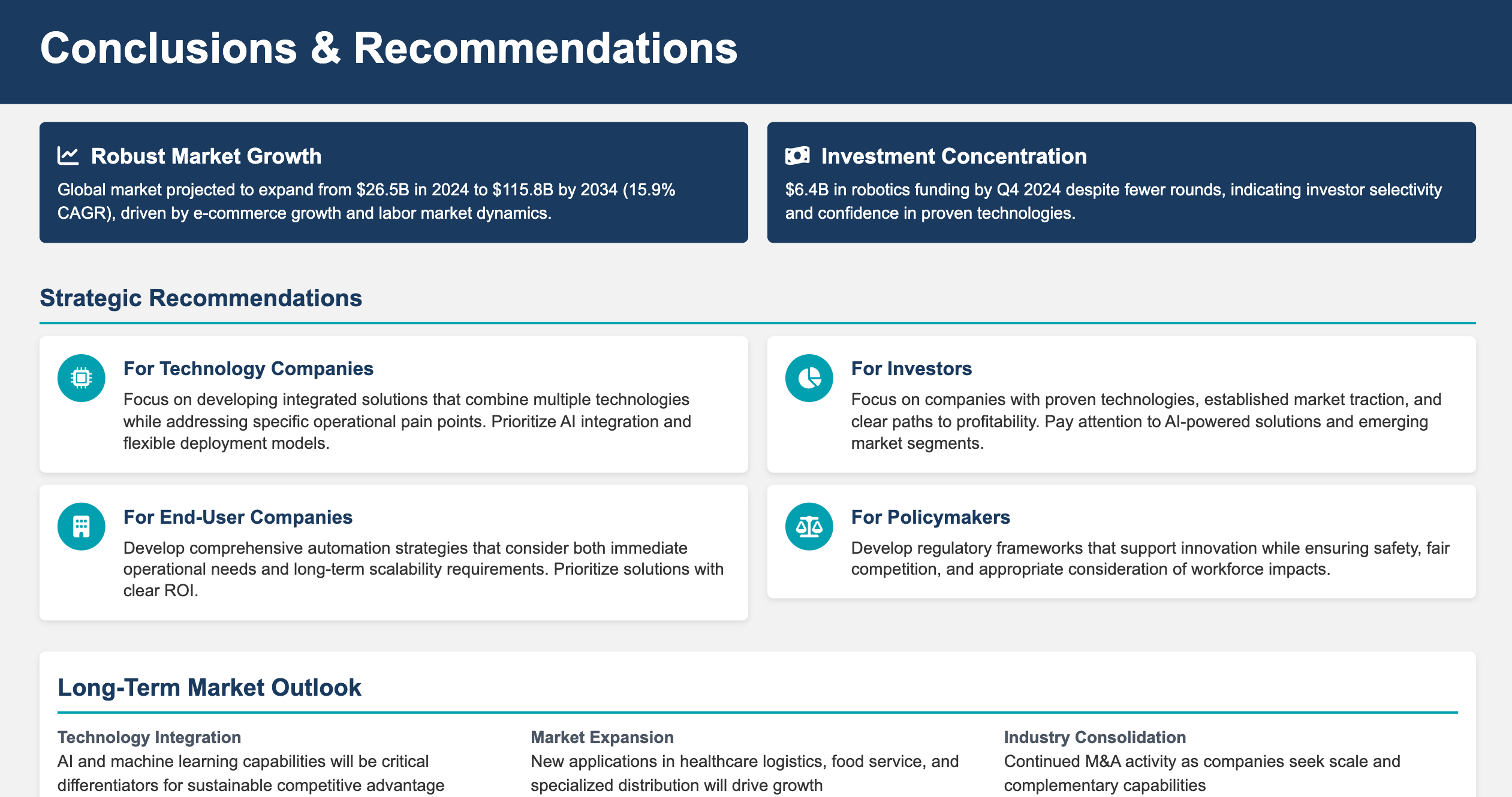

The global warehouse automation market has demonstrated remarkable resilience and growth, with multiple authoritative sources confirming substantial market expansion. According to GM Insights, the market was valued at USD 26.5 billion in 2024 and is projected to reach USD 115.8 billion by 2034, representing a compound annual growth rate (CAGR) of 15.9% [1]. This growth trajectory is further supported by data from The Business Research Company, which reports the market growing from USD 21.42 billion in 2024 to USD 24.09 billion in 2025, with projections reaching USD 42.25 billion by 2029 [2].

The driving forces behind this unprecedented growth are multifaceted and interconnected. The explosive expansion of e-commerce, accelerated by changing consumer expectations for faster delivery times, has created an urgent need for more efficient warehouse operations. Labor shortages across developed economies have further intensified the push toward automation, as companies seek to maintain operational continuity while reducing dependency on human workers for repetitive tasks. Additionally, the integration of artificial intelligence and machine learning technologies has enabled more sophisticated and adaptable automation solutions that can respond dynamically to changing operational requirements.

From a technological perspective, the warehouse automation landscape encompasses a diverse array of solutions, each addressing specific operational challenges. Autonomous Mobile Robots (AMRs) have emerged as a particularly significant category, with the global mobile robot market forecasted to exceed USD 7 billion by 2025 according to Interact Analysis [3]. These systems work alongside traditional Automated Storage and Retrieval Systems (AS/RS), conveyor networks, and increasingly sophisticated robotic picking and sorting solutions to create integrated automation ecosystems.

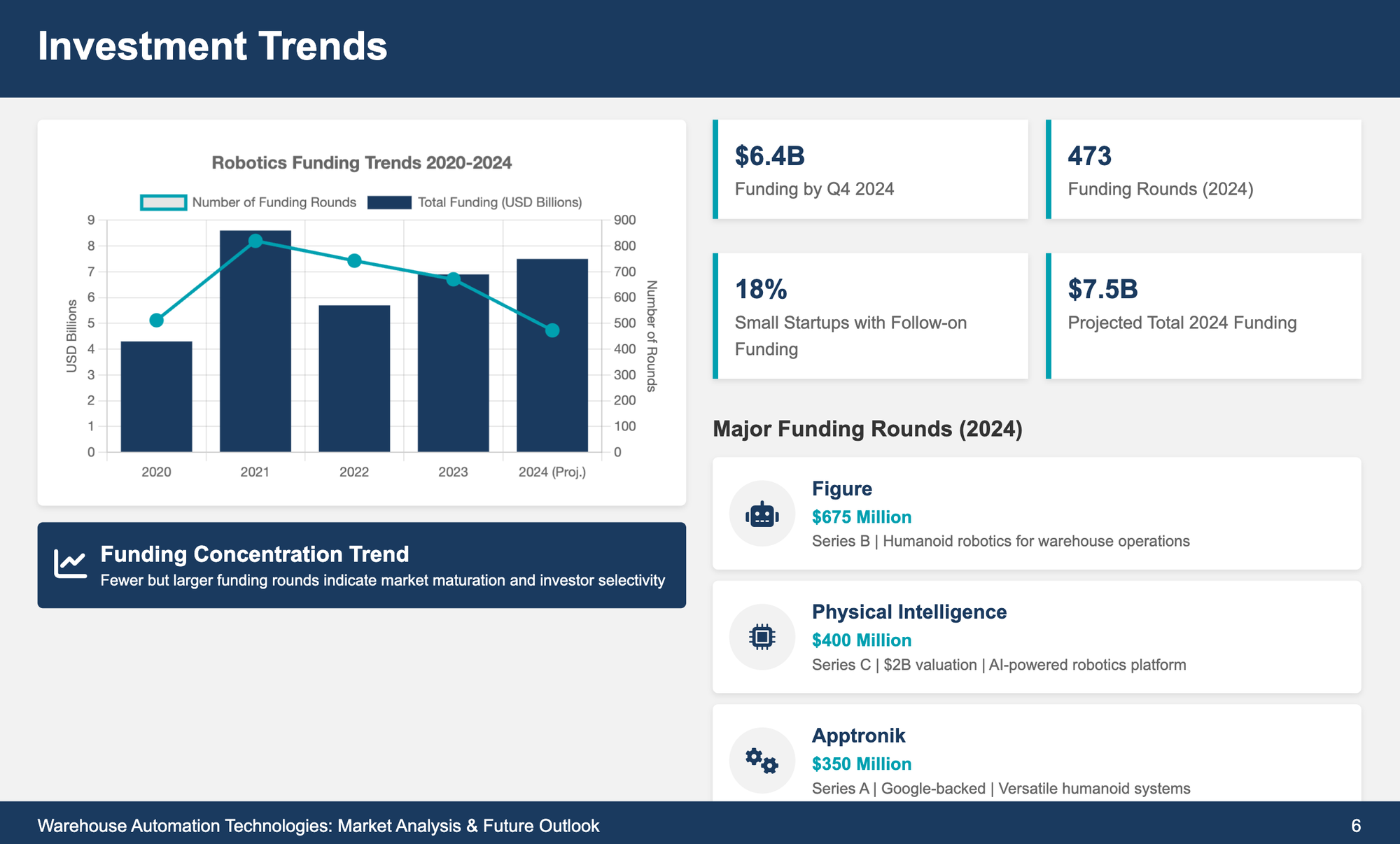

The investment landscape reflects the sector's maturity and growth potential. Robotics startups raised approximately USD 6.4 billion by Q4 2024, tracking toward USD 7.5 billion for the year, significantly exceeding 2023's USD 6.9 billion [4]. However, this funding is becoming increasingly concentrated, with fewer but larger funding rounds, indicating a shift toward more established players and proven technologies. Notable mega-rounds include Figure's USD 675 million raise, Physical Intelligence's USD 400 million at a USD 2 billion valuation, and Apptronik's USD 350 million Series A backed by Google [4].

The competitive landscape is characterized by both established industrial automation giants and innovative startups pushing the boundaries of what's possible in warehouse automation. Amazon continues to lead with over 750,000 robots deployed across its operations network, setting benchmarks for scale and integration [5]. Meanwhile, companies like Symbotic, Geek Plus, and Locus Robotics are driving innovation in specific automation categories, while traditional industrial robotics companies such as ABB, KUKA, and Fanuc adapt their technologies for warehouse applications.

This report provides a comprehensive analysis of these trends and developments, offering insights valuable to industry stakeholders, investors, technology providers, and end-users seeking to understand and navigate the rapidly evolving warehouse automation landscape. Through detailed examination of technological approaches, market dynamics, competitive positioning, and investment patterns, we aim to provide a definitive resource for understanding the current state and future trajectory of warehouse automation technologies.

Table of Contents

- Executive Summary

- Introduction and Market Overview

- Technology Landscape and Approaches

- Market Analysis and Size

- Key Players and Competitive Landscape

- Investment Trends and Funding Analysis

- Regional Analysis and Geographic Distribution

- Future Outlook and Emerging Trends

- Challenges and Opportunities

- Conclusions and Recommendations

- References

Introduction and Market Overview

The warehouse automation industry stands at the intersection of technological innovation and operational necessity, driven by fundamental shifts in global commerce, consumer behavior, and labor markets. As we progress through 2025, the sector has evolved from a niche application of industrial robotics to a comprehensive ecosystem of interconnected technologies that are reshaping the very foundations of modern logistics and supply chain management.

The transformation of warehousing operations represents one of the most significant technological shifts in industrial automation since the advent of manufacturing robotics in the 1960s. Unlike traditional manufacturing automation, which typically focuses on repetitive assembly tasks in controlled environments, warehouse automation must contend with the inherent variability and complexity of logistics operations. This includes handling diverse product types, managing fluctuating demand patterns, accommodating seasonal variations, and integrating with complex supply chain networks that span multiple geographic regions and operational contexts.

The urgency driving warehouse automation adoption has been amplified by several converging factors that have fundamentally altered the operational landscape. The explosive growth of e-commerce, which saw first-quarter 2024 sales increase 8.5% compared to the same period in 2023 while total retail sales grew only 2.8% [2], has created unprecedented pressure on fulfillment operations. This growth pattern reflects a structural shift in consumer purchasing behavior that demands faster delivery times, greater product variety, and more flexible fulfillment options.

Simultaneously, labor market dynamics have created additional pressures that make automation not just attractive but often essential for operational continuity. The warehouse and logistics sector faces persistent labor shortages, with workers in traditional fulfillment centers often walking more than 10 miles per day in search of ordered items [1]. These physically demanding conditions, combined with competitive labor markets and rising wage expectations, have made human-centric operations increasingly challenging to maintain at scale.

The technological foundation enabling modern warehouse automation has reached a level of sophistication that allows for practical implementation across a wide range of operational contexts. Advances in artificial intelligence, particularly in computer vision and machine learning, have enabled robots to handle the complex object recognition and manipulation tasks that were previously the exclusive domain of human workers. Simultaneously, improvements in sensor technology, battery life, and wireless communication have made mobile robotic systems more reliable and cost-effective than ever before.

The integration of these technologies has created what industry experts describe as "Industry 4.0 warehousing," characterized by 24/7 operation capabilities, data-driven decision-making, and scalable logistics solutions [6]. This represents a fundamental departure from traditional warehouse operations, which relied heavily on human judgment and manual processes to manage the complexities of inventory management, order fulfillment, and logistics coordination.

The market response to these technological capabilities has been overwhelmingly positive, with adoption rates accelerating across multiple industry sectors. According to StartUs Insights, the warehousing industry now encompasses over 88,370 companies globally, with more than 4,320 startups actively developing new solutions and technologies [9]. This entrepreneurial activity reflects both the significant opportunities available in the market and the ongoing evolution of technological capabilities that continue to open new possibilities for automation applications.

The scope of warehouse automation has expanded far beyond simple material handling to encompass comprehensive operational optimization. Modern automated warehouses integrate inventory management systems, predictive analytics, real-time monitoring, and adaptive workflow optimization to create highly efficient and responsive logistics operations. These systems can automatically adjust to changing demand patterns, optimize storage configurations, and coordinate complex multi-step fulfillment processes with minimal human intervention.

The economic impact of this transformation extends well beyond individual warehouse operations to influence broader supply chain strategies and competitive dynamics. Companies that successfully implement warehouse automation often achieve significant competitive advantages through reduced operational costs, improved accuracy, faster fulfillment times, and enhanced scalability. These advantages can translate into improved customer satisfaction, increased market share, and stronger financial performance, creating powerful incentives for continued investment in automation technologies.

As we examine the current state of the warehouse automation market, it becomes clear that we are witnessing not just the adoption of new technologies, but the emergence of an entirely new paradigm for logistics and supply chain management. This paradigm shift has profound implications for how companies design their operations, structure their supply chains, and compete in increasingly dynamic and demanding markets.

The following sections of this report will explore in detail the specific technologies driving this transformation, the market dynamics shaping adoption patterns, the competitive landscape of solution providers, and the investment trends that are funding continued innovation and growth in this critical sector of the global economy.

Technology Landscape and Approaches

The warehouse automation technology landscape represents a sophisticated ecosystem of interconnected systems, each designed to address specific operational challenges while contributing to overall efficiency and productivity improvements. Understanding these technologies and their applications is essential for comprehending the current market dynamics and future development trajectories in warehouse automation.

Autonomous Mobile Robots (AMRs)

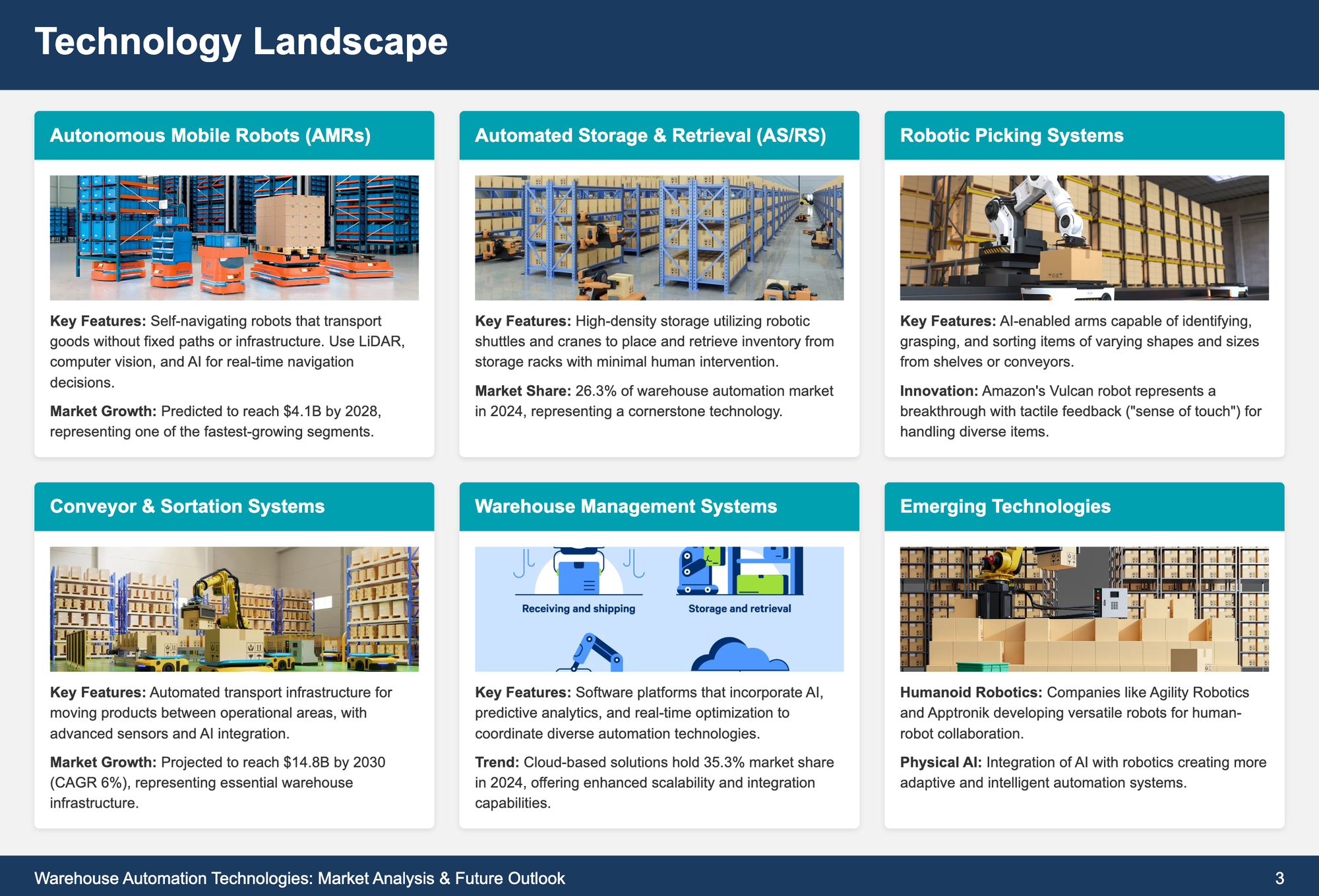

Autonomous Mobile Robots have emerged as one of the most transformative technologies in modern warehouse automation, representing a fundamental shift from fixed infrastructure solutions to flexible, adaptive systems that can navigate dynamically through warehouse environments. Unlike their predecessors, Automated Guided Vehicles (AGVs), which follow predetermined paths or magnetic tape guidance systems, AMRs utilize sophisticated navigation technologies including LiDAR, computer vision, and artificial intelligence to make real-time navigation decisions [6].

The technological sophistication of modern AMRs extends far beyond simple navigation capabilities. These systems incorporate advanced sensor arrays that enable them to detect and avoid obstacles, recognize and interact with human workers, and adapt to changing warehouse layouts without requiring infrastructure modifications. The integration of 5G connectivity has further enhanced AMR capabilities by enabling faster communication speeds and improved reliability, reducing injuries and errors in warehouse operations [2].

Current AMR implementations demonstrate remarkable versatility in their applications. These robots can transport goods between different warehouse areas, carry shelf units on their backs, or be equipped with robotic arms for picking operations. The modular design of many AMR systems allows for rapid reconfiguration to meet changing operational requirements, making them particularly valuable in environments with fluctuating demand patterns or seasonal variations.

The market response to AMR technology has been exceptionally strong, with the autonomous mobile robot market predicted to reach USD 4.1 billion by 2028 [2]. This growth reflects not only the technological maturity of AMR systems but also their proven ability to deliver measurable operational improvements. Companies implementing AMR solutions typically report significant increases in productivity, improved order accuracy, and reduced operational costs.

Advanced AMR systems now incorporate swarm robotics capabilities, where multiple robots collaborate and share data to optimize warehouse floor efficiency [2]. This collective intelligence approach enables more sophisticated task allocation, route optimization, and resource utilization than would be possible with individual robot operations. The implementation of adaptive fieldset technology has further improved AMR visibility and maneuverability, allowing for faster and safer navigation without unnecessary stops.

Automated Storage and Retrieval Systems (AS/RS)

Automated Storage and Retrieval Systems represent the backbone of high-density warehouse automation, utilizing robotic shuttles, cranes, and sophisticated control systems to place and retrieve inventory from storage racks with minimal human intervention. These systems have evolved significantly from their early implementations, now incorporating artificial intelligence and advanced algorithms to optimize storage density and retrieval efficiency [1].

Modern AS/RS implementations demonstrate remarkable sophistication in their operational capabilities. The Exotec Skypod system, for example, can identify and store inventory up to 75% faster than traditional methods by using mobile robots to transport inventory directly to containerized storage systems or employee picking stations [1]. This level of efficiency improvement represents a fundamental transformation in how warehouses can manage inventory storage and retrieval operations.

The integration of AS/RS with other warehouse automation technologies has created powerful synergies that amplify the benefits of individual systems. When combined with warehouse management systems and predictive analytics, AS/RS can automatically optimize storage configurations based on demand patterns, seasonal variations, and product characteristics. This dynamic optimization capability enables warehouses to maximize storage density while minimizing retrieval times and operational costs.

Recent developments in AS/RS technology have focused on improving flexibility and scalability. Modern systems use modular designs that allow for incremental expansion and reconfiguration without disrupting ongoing operations. The incorporation of AI-powered retrieval systems and higher-density storage solutions has enabled companies to significantly increase storage capacity while improving order accuracy and throughput [3].

The market for AS/RS technology continues to expand, with these systems accounting for 26.3% of the warehouse automation market share in 2024 [3]. This significant market presence reflects the proven value of AS/RS in addressing the fundamental challenges of inventory management and space optimization that are central to warehouse operations.

Robotic Picking and Handling Systems

Robotic picking and handling systems represent perhaps the most technically challenging aspect of warehouse automation, requiring sophisticated integration of computer vision, artificial intelligence, and mechanical engineering to replicate and exceed human capabilities in object recognition, grasping, and manipulation. The complexity of this challenge has driven significant innovation in robotics technology, resulting in systems that can handle a wide variety of products with increasing speed and accuracy.

The development of robotic picking systems has been particularly influenced by advances in artificial intelligence and machine learning. Modern picking robots utilize deep learning algorithms to recognize objects, determine optimal grasping strategies, and adapt to variations in product packaging, orientation, and condition. This AI-driven approach enables robots to handle the inherent variability of warehouse operations that previously required human judgment and dexterity.

Amazon's robotic systems exemplify the current state of the art in robotic picking technology. The company's Vulcan robot represents a fundamental leap forward as Amazon's first robot with a sense of touch, capable of picking and stowing items at the highest and lowest levels of inventory pods [5]. This system uses advanced "end of arm tooling" that can understand how much force to apply when picking items, enabling it to handle approximately three-quarters of all item types stored in fulfillment centers.

The integration of vision systems and AI cameras has become essential for modern robotic picking operations. These systems enable object recognition, inventory tracking, and quality inspection, enhancing precision in robotic operations [6]. The combination of visual recognition and tactile feedback allows robots to make sophisticated decisions about how to handle different types of products, from fragile electronics to irregularly shaped items.

Recent developments in picking technology have expanded beyond traditional robotic arms to include mobile picking solutions. Brightpick's Autopicker represents the world's first commercially available autonomous mobile picking robot designed for order fulfillment, allowing for efficient automated picking directly from shelves [6]. This innovation demonstrates the ongoing evolution of picking technology toward more flexible and scalable solutions.

Conveyor and Sortation Systems

Conveyor and sortation systems form the circulatory system of modern automated warehouses, providing the infrastructure for moving products efficiently between different operational areas. While these systems might appear less technologically sophisticated than robotic solutions, modern conveyor systems incorporate advanced sensors, AI integration, and modular designs that make them essential components of comprehensive automation strategies.

The evolution of conveyor technology has focused on improving modularity, sustainability, and integration capabilities. Modern automated conveyors feature energy-efficient motors, lower friction bearings, and variable speed drives that enhance sustainability while reducing operational costs [2]. The implementation of modular designs with pre-programmed controls allows for faster installation and high efficiency in transporting thousands of bins per hour.

Advanced conveyor systems now incorporate sophisticated sensor technology and AI integrations that enable them to detect obstacles and optimize item transportation for greater efficiency [2]. These intelligent conveyor systems can automatically adjust speeds, route products to appropriate destinations, and coordinate with other warehouse automation systems to optimize overall workflow efficiency.

The automated conveyor market is projected to grow from USD 10.4 billion in 2024 to USD 14.8 billion by 2030, reflecting a compound annual growth rate of 6% [2]. This steady growth demonstrates the continued importance of conveyor systems as foundational infrastructure for warehouse automation, even as more sophisticated robotic solutions gain prominence.

Maintenance enhancements have become a significant focus area for conveyor system development. Automated belt-cleaning technology improves safety by preventing contact between blades and belts, extending equipment lifespan and reducing injury risks [2]. These improvements in reliability and safety are essential for maintaining the continuous operation that modern automated warehouses require.

Warehouse Management and Execution Systems

The software layer of warehouse automation, encompassing Warehouse Management Systems (WMS) and Warehouse Execution Systems (WES), provides the intelligence and coordination capabilities that enable diverse automation technologies to work together effectively. These systems have evolved from simple inventory tracking tools to sophisticated platforms that incorporate artificial intelligence, predictive analytics, and real-time optimization capabilities.

Modern warehouse management systems utilize machine learning algorithms to accurately predict demand, optimize order processing, and minimize the risk of stockouts or excess inventory [1]. The integration of AI-driven analytics enables real-time decision-making that can improve automation productivity and efficiency while reducing operational costs. This predictive capability is particularly valuable in managing the complex interactions between different automation systems and optimizing overall warehouse performance.

The trend toward cloud-based warehouse management systems has accelerated, with cloud-based solutions holding a 35.3% market share in 2024 [3]. Cloud-based systems offer advantages in terms of scalability, integration capabilities, and access to advanced analytics tools that can enhance warehouse optimization. The ability to integrate with various digital platforms makes cloud-based solutions particularly attractive for e-commerce and third-party logistics providers.

Warehouse execution systems have emerged as a critical component for coordinating real-time operations in highly automated environments. These systems bridge the gap between high-level warehouse management functions and the detailed control of individual automation systems, ensuring that complex multi-step processes are executed efficiently and accurately.

The integration of Internet of Things (IoT) sensors and real-time monitoring capabilities has enhanced the visibility and control that warehouse management systems can provide. These technologies enable continuous monitoring of system performance, predictive maintenance scheduling, and dynamic optimization of warehouse operations based on real-time conditions and performance data.

Emerging Technologies and Future Directions

The warehouse automation technology landscape continues to evolve rapidly, with several emerging technologies showing significant promise for future applications. Humanoid robotics, exemplified by companies like Agility Robotics with their Digit robot and Apptronik's versatile humanoid systems, represents a new frontier in warehouse automation that could enable more flexible and adaptable automation solutions [6].

The integration of augmented reality and virtual reality technologies is creating new possibilities for human-robot collaboration and training. Smart glasses and heads-up displays are enhancing picking accuracy and efficiency by providing workers with real-time information and guidance [2]. Virtual reality technology is being used for training purposes and to provide real and virtual imagery that can reduce errors and minimize distractions during complex tasks.

Artificial intelligence continues to drive innovation across all aspects of warehouse automation. The development of "Physical AI" through partnerships like the one between Kion Group, Nvidia, and Accenture demonstrates the potential for more sophisticated integration of AI capabilities into warehouse operations [6]. These advances promise to enable more adaptive and intelligent automation systems that can respond dynamically to changing operational requirements.

The convergence of these technologies is creating opportunities for more comprehensive and integrated automation solutions that can address the full spectrum of warehouse operations. As these technologies mature and their costs continue to decline, we can expect to see broader adoption across different types of warehouses and operational contexts, further accelerating the transformation of the logistics and supply chain industry.

Market Analysis and Size

The warehouse automation market has demonstrated exceptional growth momentum, establishing itself as one of the most dynamic sectors within the broader industrial automation industry. The convergence of technological advancement, operational necessity, and favorable economic conditions has created a market environment characterized by rapid expansion, significant investment activity, and accelerating adoption across diverse industry sectors.

Global Market Size and Growth Projections

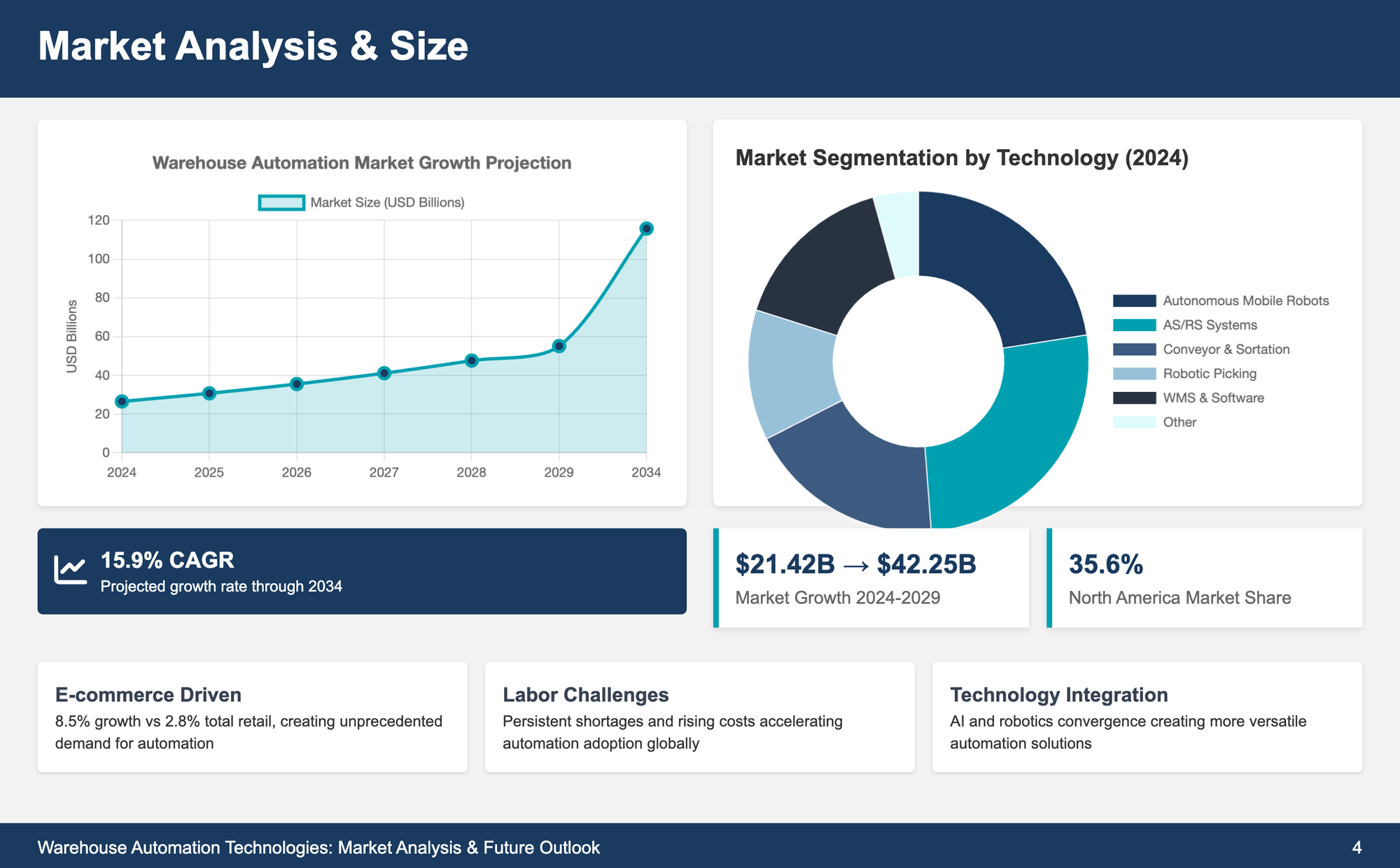

The global warehouse automation market presents a compelling growth story, with multiple authoritative sources providing consistent evidence of substantial market expansion. According to GM Insights, the market was valued at USD 26.5 billion in 2024 and is projected to reach USD 115.8 billion by 2034, representing a compound annual growth rate of 15.9% over the forecast period [1]. This projection reflects not only the current momentum in the market but also the sustained demand drivers that are expected to continue fueling growth throughout the decade.

Alternative market assessments provide additional perspective on the market's scale and trajectory. The Business Research Company reports the market growing from USD 21.42 billion in 2024 to USD 24.09 billion in 2025, with a compound annual growth rate of 12.4%, and projecting continued expansion to USD 42.25 billion by 2029 at a CAGR of 15.1% [2]. While these figures differ in absolute terms, they consistently demonstrate the market's robust growth trajectory and the confidence that industry analysts have in the sector's future prospects.

The variation in market size estimates reflects different methodological approaches and scope definitions used by various research organizations. Some studies focus specifically on hardware components, while others include software, services, and integration costs. Despite these methodological differences, the consistent pattern of double-digit growth rates across all major market research reports provides strong evidence of the market's fundamental strength and growth potential.

The automated warehouse equipment market specifically reached USD 29.6 billion in 2024 and is projected to grow to USD 60.04 billion by 2031 [2]. This segment represents the core hardware components of warehouse automation systems and demonstrates the substantial investment being made in physical automation infrastructure. The growth in this segment reflects both the expansion of automation to new facilities and the upgrading of existing operations with more advanced technologies.

Market Segmentation and Component Analysis

The warehouse automation market exhibits significant diversity in its component structure, with different technology categories experiencing varying growth rates and market dynamics. Understanding these segmentation patterns is essential for comprehending the market's evolution and identifying the most promising areas for future development and investment.

Hardware components continue to represent the largest segment of the warehouse automation market, with projections indicating growth at a CAGR of 15.3% through 2034 [3]. This segment encompasses the physical automation systems including robots, conveyor systems, storage equipment, and control hardware. The continued dominance of hardware reflects the capital-intensive nature of warehouse automation implementations and the ongoing need for physical infrastructure to support automated operations.

The services segment has emerged as a particularly significant component, accounting for 37% of the market share in 2024 [3]. This segment includes installation, maintenance, training, and consulting services that are essential for successful automation implementations. The growth of the services segment reflects the increasing complexity of automation systems and the need for specialized expertise to design, implement, and maintain these sophisticated technologies.

Software components, while representing a smaller absolute market size, are experiencing rapid growth as automation systems become more intelligent and integrated. The trend toward cloud-based solutions is particularly notable, with cloud-based warehouse management systems holding a 35.3% market share in 2024 [3]. This shift toward cloud-based solutions reflects the advantages these systems offer in terms of scalability, integration capabilities, and access to advanced analytics tools.

Technology-Specific Market Dynamics

Different automation technologies are experiencing distinct market dynamics that reflect their maturity levels, application scope, and technological advancement rates. Autonomous Mobile Robots represent one of the fastest-growing segments, with the market predicted to reach USD 4.1 billion by 2028 [2]. This growth reflects the versatility and relatively rapid deployment capabilities of AMR systems compared to more infrastructure-intensive automation solutions.

The automated forklift market demonstrates the evolution of traditional material handling equipment toward automation, with projections showing growth from USD 0.69 billion in 2024 to USD 1.52 billion in 2032 [2]. This segment illustrates how established equipment categories are being transformed through the integration of automation technologies, creating new market opportunities while building on existing operational familiarity.

Automated Storage and Retrieval Systems continue to represent a substantial market segment, accounting for 26.3% of the warehouse automation market share in 2024 [3]. The maturity and proven effectiveness of AS/RS technology has made it a cornerstone of many automation implementations, particularly in high-density storage applications where space optimization is critical.

The multi-directional pallet shuttle market exemplifies the rapid growth potential of specialized automation technologies, with projections showing expansion to USD 772.8 million by 2030 at a remarkable CAGR of 28.3% [2]. This growth rate demonstrates how innovative solutions that address specific operational challenges can achieve exceptional market penetration when they deliver clear value propositions.

End-User Market Analysis

The warehouse automation market serves diverse end-user segments, each with distinct requirements, adoption patterns, and growth trajectories. E-commerce fulfillment centers represent the largest and fastest-growing end-user segment, with market projections indicating growth to USD 31.3 billion by 2034 [3]. This segment's dominance reflects the operational pressures created by e-commerce growth and the need for fulfillment operations that can handle high volumes of small, diverse orders with rapid turnaround times.

Cold storage warehouses represent another significant growth area, holding a 22.6% market share in 2024 [3]. The specialized requirements of temperature-controlled environments, combined with the need to minimize human exposure to harsh conditions, make automation particularly attractive for cold storage applications. The integration of automated temperature-controlled storage systems and AI-driven inventory management is driving innovation in this segment.

Healthcare applications are emerging as a particularly promising end-user segment, driven by the need for precise inventory management, contamination control, and regulatory compliance. The specialized requirements of pharmaceutical and medical device storage and distribution create opportunities for automation solutions that can ensure product integrity while improving operational efficiency.

Manufacturing warehouses continue to represent a substantial market segment, benefiting from the integration of warehouse automation with broader manufacturing automation strategies. The trend toward just-in-time manufacturing and lean inventory management has increased the importance of efficient warehouse operations that can support responsive manufacturing processes.

Regional Market Distribution

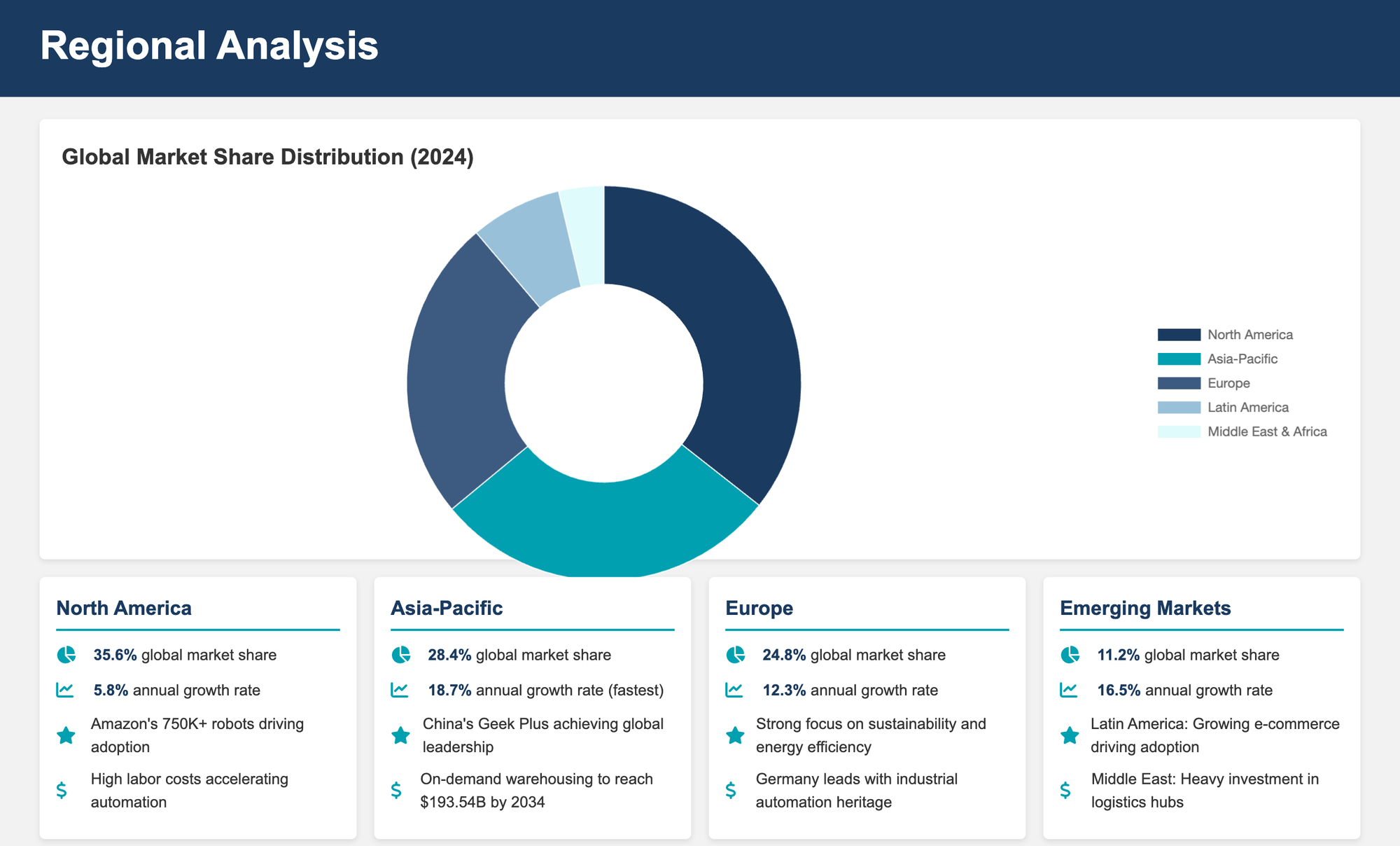

The global warehouse automation market exhibits significant regional variation in terms of market size, growth rates, and adoption patterns. North America represents the largest regional market, accounting for 35.6% of global market share in 2024 [3]. This dominance reflects the region's advanced logistics infrastructure, high labor costs that favor automation adoption, and the presence of major e-commerce companies that are driving innovation in warehouse automation.

Asia-Pacific is expected to be the fastest-growing regional market, driven by rapid industrialization, expanding e-commerce markets, and increasing labor costs in developed Asian economies [2]. The region's manufacturing-centric economy and growing consumer markets create substantial demand for efficient warehouse and distribution operations that can support both domestic consumption and export activities.

The United States warehouse market specifically is expected to grow by 5.8% annually, driven by e-commerce expansion and the need for last-mile delivery solutions [9]. This growth rate reflects the maturity of the U.S. market while demonstrating continued expansion opportunities as automation technologies become more accessible and cost-effective.

The Asia Pacific on-demand warehousing market is projected to reach USD 193.54 billion by 2034 [9], highlighting the significant growth potential in this region. This projection reflects not only the scale of economic development in the region but also the increasing sophistication of logistics and supply chain operations that are driving demand for advanced warehouse automation solutions.

Market Drivers and Growth Factors

The warehouse automation market's growth is driven by a combination of technological, economic, and operational factors that create compelling value propositions for automation adoption. E-commerce growth represents the most significant driver, with first-quarter 2024 e-commerce sales increasing 8.5% compared to the same period in 2023, while total retail sales grew only 2.8% [2]. This differential growth pattern creates operational pressures that favor automation solutions capable of handling high-volume, diverse order fulfillment requirements.

Labor market dynamics provide another critical growth driver, with persistent labor shortages and rising wage costs making automation increasingly attractive from an economic perspective. The physical demands of traditional warehouse work, where employees often walk more than 10 miles per day, combined with competitive labor markets, have made human-centric operations increasingly challenging to maintain at scale [1].

Technological advancement continues to drive market growth by expanding the range of applications where automation can provide value while reducing implementation costs and complexity. The integration of artificial intelligence, improved sensor technologies, and enhanced battery life has made automation systems more reliable, flexible, and cost-effective than previous generations of technology.

Consumer expectations for faster delivery times and greater service levels have created operational requirements that are difficult to meet without automation. The demand for same-day and next-day delivery services requires warehouse operations that can process orders quickly and accurately, capabilities that are enhanced significantly through automation implementation.

The market's growth trajectory reflects the convergence of these factors in creating a compelling business case for warehouse automation across a wide range of operational contexts and industry sectors. As these drivers continue to intensify and automation technologies become more sophisticated and accessible, the market is positioned for continued robust growth throughout the remainder of the decade.

Key Players and Competitive Landscape

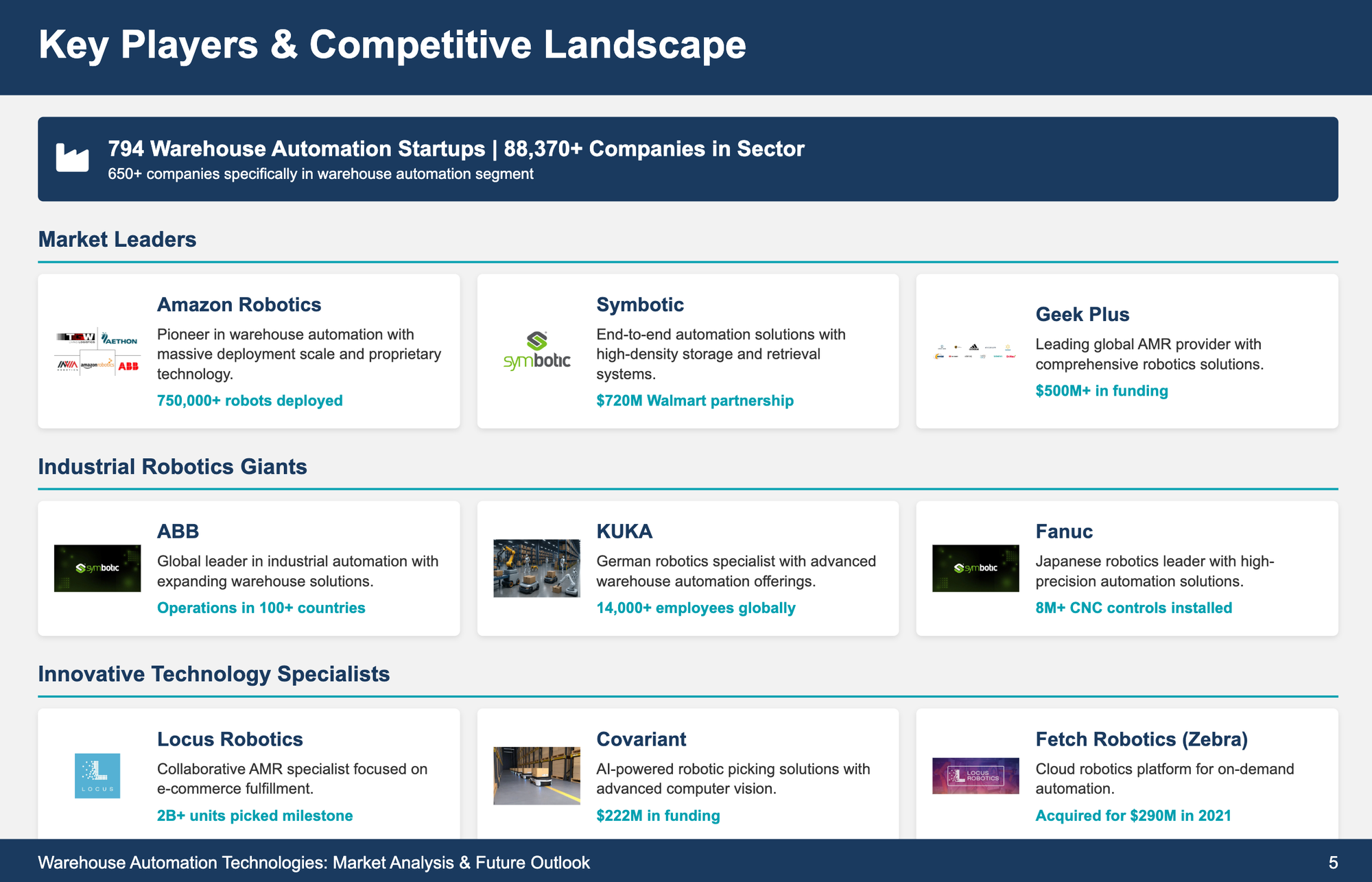

The warehouse automation industry is characterized by a diverse ecosystem of companies ranging from established industrial automation giants to innovative startups pushing the boundaries of robotic and AI technologies. This competitive landscape reflects the multifaceted nature of warehouse automation, where different companies excel in specific technology areas while others pursue comprehensive platform strategies. Understanding the positioning and capabilities of key players is essential for comprehending market dynamics and future development trajectories.

Market Leaders and Established Players

Amazon Robotics stands as the undisputed leader in warehouse automation deployment and innovation, with over 750,000 robots currently operating across its global fulfillment network [5]. The company's approach to automation represents a comprehensive integration strategy that combines proprietary robotic systems with advanced software platforms and operational methodologies. Amazon's latest innovations include the Proteus robot, which represents a significant advancement in autonomous mobile robot technology, and the Sequoia system, which can identify and store inventory up to 75% faster than traditional methods [5].

Amazon's Vulcan robot represents a fundamental technological breakthrough as the company's first robot equipped with a sense of touch, capable of picking and stowing items at the highest and lowest levels of inventory pods [5]. This system utilizes advanced "end of arm tooling" that can determine appropriate force application when handling items, enabling it to manage approximately three-quarters of all item types stored in fulfillment centers. The integration of tactile feedback with computer vision represents a significant advancement in robotic manipulation capabilities.

Symbotic Corporation has emerged as a major force in warehouse automation through its strategic partnership with Walmart and its focus on AI-enabled robotic solutions. The company's recent expansion includes Walmart's acquisition of Symbotic's robotics division for USD 200 million, combined with a USD 520 million investment to develop advanced AI-enabled robotics solutions [6]. This partnership demonstrates the growing recognition of Symbotic's technological capabilities and its potential to transform large-scale retail operations.

Geek Plus has established itself as one of the largest providers of autonomous mobile robots globally, demonstrating the rapid growth potential available to companies that can successfully scale innovative automation technologies [6]. The company's success illustrates the global nature of the warehouse automation market and the opportunities available for companies that can develop cost-effective, scalable solutions for diverse operational environments.

Kion Group (Dematic) represents the convergence of traditional material handling expertise with cutting-edge AI technologies through its partnership with Nvidia and Accenture to develop "Physical AI" integration capabilities [6]. This collaboration demonstrates how established industrial equipment companies are evolving to incorporate advanced AI capabilities into their automation solutions, creating more intelligent and adaptive systems.

Industrial Robotics Giants

The warehouse automation market has attracted significant participation from established industrial robotics companies that are adapting their technologies for logistics applications. ABB Ltd. leverages its extensive experience in industrial automation to provide robotic solutions for palletizing, material handling, and warehouse operations. The company's collaborative robots and advanced control systems are increasingly being deployed in warehouse environments where precision and reliability are critical.

KUKA Group has developed specialized warehouse automation solutions that build on its expertise in automotive and manufacturing robotics. The company's systems are particularly notable for their integration capabilities and ability to work alongside human operators in collaborative environments. KUKA's approach emphasizes flexibility and adaptability, enabling warehouse operations to adjust to changing requirements without extensive system reconfiguration.

Fanuc Corporation brings its reputation for high-precision, high-speed robotic systems to warehouse applications, particularly in areas requiring rapid and accurate material handling. The company's robots are increasingly being deployed in automated picking and packing applications where speed and precision are essential for operational efficiency.

Yaskawa Electric Corporation through its Motoman robotics division provides solutions for welding, assembly, and material handling applications in warehouse environments. The company's focus on reliability and performance has made its systems popular in applications where continuous operation is critical.

Innovative Technology Specialists

Locus Robotics has established itself as a leader in collaborative autonomous mobile robots designed to work alongside human workers in warehouse environments. The company's approach emphasizes human-robot collaboration rather than full automation, creating solutions that can be implemented incrementally while preserving the flexibility that human workers provide for complex tasks.

Covariant represents the cutting edge of AI-powered robotics with its "Covariant Brain" software platform that enables robots to learn and adapt to new tasks through machine learning [6]. Founded by researchers from UC Berkeley and OpenAI, the company exemplifies the application of advanced AI research to practical warehouse automation challenges.

Fetch Robotics, now part of Zebra Technologies, developed cloud-driven autonomous mobile robots that demonstrated the potential for software-centric approaches to warehouse automation. The acquisition by Zebra Technologies reflects the strategic value of combining robotics capabilities with enterprise data capture and automatic identification technologies.

Ocado Group has developed sophisticated automated warehouse systems that integrate multiple technologies into comprehensive fulfillment solutions. The company's acquisition of 6 River Systems from Shopify demonstrates its commitment to expanding its collaborative mobile robotics capabilities while building on its established automated storage and retrieval expertise.

Emerging Players and Disruptive Technologies

Boston Dynamics has entered the warehouse automation market with its Stretch robot, specifically designed for truck unloading and box moving applications [6]. The company's expertise in advanced robotics and dynamic movement capabilities brings new possibilities for handling complex material handling tasks that have traditionally required human workers.

Agility Robotics represents the emerging category of humanoid robotics for warehouse applications with its Digit robot designed for bin retrieval and carrying tasks [6]. The company's approach to humanoid robotics offers the potential for more flexible automation solutions that can adapt to existing warehouse infrastructure without requiring extensive modifications.

Apptronik is developing versatile humanoid robots designed for human-robot collaboration in warehouse environments [6]. The company's recent USD 350 million Series A funding round, backed by Google, demonstrates the significant investor interest in humanoid robotics applications for warehouse automation.

Berkshire Grey focuses on AI-enabled robotic solutions for supply chain automation, emphasizing the integration of artificial intelligence with robotic systems to create more adaptive and intelligent automation solutions. The company's approach demonstrates the growing importance of AI capabilities in differentiating automation solutions.

Brightpick has developed what it claims is the world's first commercial autonomous mobile picking robot, the Autopicker, designed specifically for order fulfillment applications [6]. This innovation represents the ongoing evolution of picking technology toward more integrated and autonomous solutions.

Regional and Specialized Players

Addverb Technologies represents the growing presence of Indian companies in the global warehouse automation market, offering a comprehensive range of solutions including AMRs, AS/RS, sortation systems, and pallet shuttles [6]. The company's success demonstrates the global nature of innovation in warehouse automation and the opportunities for companies to compete based on technological capabilities rather than geographic proximity.

HAI Robotics has developed Autonomous Case-handling Robot (ACR) systems that represent innovative approaches to warehouse automation from the Chinese market [6]. The company's solutions demonstrate the diversity of technological approaches being developed globally and the potential for different regional markets to contribute unique innovations.

GreyOrange provides AI-driven fulfillment automation solutions that emphasize the integration of artificial intelligence with robotic systems to optimize warehouse operations [6]. The company's approach reflects the growing importance of software and AI capabilities in creating competitive advantages in warehouse automation.

Competitive Dynamics and Market Positioning

The competitive landscape in warehouse automation is characterized by several distinct strategic approaches that reflect different perspectives on market opportunities and technological capabilities. Some companies pursue comprehensive platform strategies that aim to provide end-to-end automation solutions, while others focus on specialized technologies that can be integrated with existing systems or solutions from other providers.

The trend toward consolidation through mergers and acquisitions is becoming increasingly prominent, as demonstrated by recent transactions such as Jungheinrich's acquisition of Storage Solutions Inc. and Walmart's investment in Symbotic [2]. These transactions reflect the strategic value of combining complementary technologies and capabilities to create more comprehensive automation solutions.

Innovation cycles in the warehouse automation market are accelerating, with companies increasingly focusing on AI integration, machine learning capabilities, and adaptive systems that can respond dynamically to changing operational requirements. The emphasis on "Physical AI" and intelligent automation represents a significant evolution from earlier generations of warehouse automation that relied primarily on predetermined programming and fixed operational parameters.

The competitive landscape is also being shaped by the increasing importance of software and data analytics capabilities. Companies that can effectively combine hardware capabilities with sophisticated software platforms and AI-driven optimization are gaining competitive advantages over those that focus primarily on hardware solutions.

Partnership strategies are becoming increasingly important as companies recognize the complexity of developing comprehensive automation solutions independently. Strategic partnerships between technology companies, system integrators, and end-users are creating new opportunities for innovation and market development while enabling companies to leverage complementary capabilities and expertise.

The emergence of humanoid robotics as a potential disruptive technology is creating new competitive dynamics, with companies like Agility Robotics and Apptronik challenging traditional approaches to warehouse automation. While these technologies are still in early stages of commercial deployment, they represent potential paradigm shifts that could significantly alter competitive positioning in the warehouse automation market.

As the market continues to evolve, competitive success will increasingly depend on companies' abilities to integrate multiple technologies effectively, provide comprehensive solutions that address diverse operational requirements, and adapt quickly to changing market conditions and technological developments. The companies that can successfully navigate these challenges while continuing to innovate and scale their operations are positioned to capture the significant growth opportunities available in the expanding warehouse automation market.

Investment Trends and Funding Analysis

The warehouse automation sector has emerged as one of the most attractive investment destinations within the broader robotics and industrial automation landscape, characterized by substantial funding rounds, increasing investor sophistication, and a shift toward more concentrated investment in proven technologies and established companies. Understanding these investment patterns is crucial for comprehending market dynamics and anticipating future development trajectories.

Overall Funding Landscape and Market Dynamics

The robotics funding landscape in 2024 demonstrated remarkable resilience and growth, with robotics startups raising approximately USD 6.4 billion by Q4 2024, tracking toward USD 7.5 billion for the full year [4]. This figure significantly exceeded 2023's total of USD 6.9 billion, indicating sustained investor confidence in robotics technologies despite broader economic uncertainties. However, this growth came with an important caveat: the funding was increasingly concentrated among fewer companies, with only 473 funding rounds in 2024 compared to 671 in the previous year [4].

This concentration trend reflects a maturing market where investors are becoming more selective, focusing on companies with proven technologies, clear market traction, and scalable business models. The shift toward larger, less frequent funding rounds indicates that the market is moving beyond the early experimental phase toward more substantial commercial deployments and proven value propositions.

The warehouse automation segment specifically has benefited from this trend toward larger funding rounds, with several companies achieving significant mega-rounds that demonstrate investor confidence in the sector's growth potential. Notable examples include Figure's USD 675 million raise, Physical Intelligence's USD 400 million funding at a USD 2 billion valuation, and Apptronik's USD 350 million Series A round backed by Google [4]. These substantial funding rounds reflect both the capital-intensive nature of robotics development and the significant market opportunities that investors perceive in warehouse automation.

Sector-Specific Investment Patterns

The warehouse automation investment landscape exhibits distinct patterns that reflect the diverse technological approaches and market applications within the sector. Autonomous mobile robots have attracted particularly strong investor interest, with companies in this category consistently achieving substantial funding rounds. The versatility and relatively rapid deployment capabilities of AMR systems make them attractive to investors seeking technologies with broad market applicability and shorter time-to-market cycles.

Healthcare robotics has emerged as a particularly promising investment category, with industry experts identifying it as the next major robotics success story following warehouse automation [4]. This trend is supported by significant exit activity, including Johnson & Johnson's USD 3.4 billion acquisition of Auris Health and Stryker's USD 1.65 billion acquisition of Mako Surgical, which have validated the commercial potential of robotics applications in healthcare settings.

The investment focus on AI-powered robotics has become increasingly pronounced, with investors particularly enthusiastic about companies developing versatile, multi-purpose robots with advanced artificial intelligence capabilities [4]. This preference reflects the recognition that AI integration is essential for creating automation solutions that can adapt to diverse operational requirements and provide sustainable competitive advantages.

Funding Challenges and Market Realities

Despite the overall positive funding environment, warehouse automation companies face unique challenges that distinguish them from software-focused startups. The hardware-plus-software nature of robotics development requires significantly higher upfront capital investments, longer development cycles, and more complex validation processes [4]. These factors contribute to what industry observers describe as the "timeline problem," where robotics companies typically require years to progress from laboratory prototypes to commercial products.

The capital-intensive nature of robotics development has created a challenging environment for early-stage companies, with only 18% of small warehousing tech startups securing follow-on funding in 2024 according to CB Insights [3]. This statistic highlights the importance of achieving significant milestones and demonstrating clear market traction to secure continued funding support.

Market adoption uncertainties add another layer of complexity to the funding landscape. Even companies with proven technologies often face challenges in achieving rapid customer adoption due to the costs and integration complexity associated with warehouse automation implementations. In uncertain economic conditions, potential customers are taking longer to make purchasing decisions and delaying expensive equipment purchases, creating additional market risk that investors must consider [4].

Alternative Funding Mechanisms and Market Evolution

The traditional venture capital model is no longer the only option for warehouse automation companies seeking capital. Direct-to-investor fundraising through regulations such as Reg A+ and Reg CF is opening new funding pathways that allow both accredited and non-accredited investors to participate in robotics company investments [4]. These alternative funding mechanisms are particularly attractive for hardware-intensive companies that require substantial capital but may not fit traditional VC investment profiles.

Regulation A+ allows companies to raise up to USD 75 million annually while providing a potential path to listing on national exchanges, creating opportunities for warehouse automation companies to access broader investor bases [4]. This funding mechanism has proven particularly effective for companies with clear commercial applications and established customer bases.

The success of companies like Monogram Orthopaedics, which successfully transitioned from startup to Nasdaq listing using alternative funding methods, demonstrates the viability of these approaches for robotics companies [4]. This example provides a roadmap for warehouse automation companies seeking to access capital markets while maintaining greater control over their funding processes.

Corporate Investment and Strategic Partnerships

Corporate investment has become an increasingly important component of the warehouse automation funding landscape, with major companies establishing dedicated investment funds and partnership programs to access innovative technologies. Amazon's USD 1 billion Industrial Innovation Fund represents one of the most significant corporate investment initiatives in the sector, providing direct investments to emerging technology companies developing solutions relevant to Amazon's operations [6].

Strategic partnerships between technology companies and end-users are creating new funding and development opportunities that combine financial investment with market access and operational validation. Symbotic's partnership with Walmart, which included both acquisition and investment components totaling USD 720 million, exemplifies how strategic relationships can provide both funding and market validation for innovative automation technologies [6].

The trend toward corporate venture capital investment reflects the recognition by major companies that external innovation is essential for maintaining competitive advantages in rapidly evolving markets. These corporate investors often provide not only capital but also market access, operational expertise, and validation that can be crucial for technology companies seeking to scale their operations.

Geographic Distribution and Regional Trends

Investment activity in warehouse automation exhibits significant geographic concentration, with certain regions demonstrating particular strength in attracting funding and developing innovative companies. The United States continues to dominate in terms of absolute funding amounts, benefiting from a mature venture capital ecosystem and the presence of major technology companies and logistics operators.

Asia-Pacific markets are demonstrating increasing investment activity, driven by rapid economic development, expanding e-commerce markets, and growing recognition of the importance of logistics automation for economic competitiveness. Companies like Geek Plus have demonstrated the potential for Asian companies to achieve global scale and attract international investment.

European markets are showing strong growth in warehouse automation investment, with companies like Exotec and various German automation specialists attracting significant funding rounds. The European focus on sustainability and energy efficiency is creating opportunities for automation companies that can demonstrate environmental benefits alongside operational improvements.

Investment Outlook and Future Trends

The investment outlook for warehouse automation remains positive, supported by fundamental market drivers that are expected to continue strengthening throughout the remainder of the decade. The ongoing growth of e-commerce, persistent labor market challenges, and continued technological advancement create a favorable environment for continued investment in automation technologies.

However, investors are becoming increasingly sophisticated in their evaluation criteria, focusing on companies that can demonstrate clear paths to profitability, scalable business models, and sustainable competitive advantages. The emphasis on proven technologies and established market traction suggests that future funding will be concentrated among companies that have successfully navigated the transition from development to commercial deployment.

The emergence of new funding mechanisms and the increasing involvement of corporate investors are creating a more diverse and sophisticated funding ecosystem that can better support the capital-intensive nature of warehouse automation development. This evolution in funding approaches is expected to accelerate the development and deployment of innovative automation technologies while providing more sustainable funding pathways for companies in the sector.

The integration of artificial intelligence and machine learning capabilities is becoming a critical factor in investment decisions, with investors increasingly focused on companies that can demonstrate advanced AI capabilities and the potential for continuous improvement through data-driven optimization. This trend suggests that future investment will favor companies that can effectively combine hardware capabilities with sophisticated software platforms and AI-driven functionality.

As the market continues to mature, we can expect to see continued consolidation through mergers and acquisitions, creating opportunities for investors to realize returns while enabling companies to achieve the scale and capabilities necessary to compete in an increasingly sophisticated and demanding market environment. The companies that can successfully navigate this evolving funding landscape while continuing to innovate and scale their operations are positioned to capture the significant opportunities available in the expanding warehouse automation market.

Regional Analysis and Geographic Distribution

The global warehouse automation market exhibits significant regional variations in adoption patterns, technological preferences, market maturity, and growth trajectories. These regional differences reflect diverse economic conditions, labor market dynamics, regulatory environments, and industrial development patterns that influence how warehouse automation technologies are developed, deployed, and scaled across different geographic markets.

North American Market Leadership

North America maintains its position as the largest regional market for warehouse automation, accounting for 35.6% of global market share in 2024 [3]. This dominance reflects several structural advantages that have positioned the region at the forefront of automation adoption. The presence of major e-commerce companies, particularly Amazon, has created a demonstration effect that has accelerated adoption across the broader logistics industry. Amazon's deployment of over 750,000 robots across its fulfillment network has not only validated the effectiveness of warehouse automation but also created competitive pressures that drive adoption among other logistics operators [5].

The United States warehouse market specifically is expected to grow by 5.8% annually, driven by e-commerce expansion and the increasing demand for last-mile delivery solutions [9]. This growth rate reflects both the maturity of the U.S. market and the continued opportunities for expansion as automation technologies become more accessible and cost-effective. The sophisticated logistics infrastructure in North America, combined with high labor costs that favor automation adoption, creates favorable conditions for continued market growth.

The regulatory environment in North America has generally been supportive of automation adoption, with relatively few restrictions on robotic systems and a business culture that embraces technological innovation. The presence of major technology companies and research institutions has also contributed to the region's leadership in developing advanced automation technologies, particularly in areas such as artificial intelligence and machine learning applications.

Canadian markets are demonstrating strong growth in warehouse automation adoption, driven by the need to remain competitive with U.S. logistics operations and the challenges of serving a geographically dispersed population efficiently. The integration of Canadian operations with broader North American supply chains has accelerated the adoption of automation technologies that can provide seamless cross-border logistics capabilities.

Asia-Pacific: The Fastest-Growing Market

Asia-Pacific has emerged as the fastest-growing regional market for warehouse automation, driven by rapid industrialization, expanding e-commerce markets, and increasing labor costs in developed Asian economies [2]. The region's manufacturing-centric economy and growing consumer markets create substantial demand for efficient warehouse and distribution operations that can support both domestic consumption and export activities.

The Asia Pacific on-demand warehousing market is projected to reach USD 193.54 billion by 2034 [9], highlighting the significant growth potential in this region. This projection reflects not only the scale of economic development in the region but also the increasing sophistication of logistics and supply chain operations that are driving demand for advanced warehouse automation solutions.

China represents the largest individual market within the Asia-Pacific region, with companies like Geek Plus achieving global leadership positions in autonomous mobile robot technology [6]. The Chinese market benefits from a combination of large-scale manufacturing operations, rapidly growing e-commerce markets, and government policies that support automation and technological advancement. The presence of major technology companies and the availability of skilled engineering talent have contributed to China's emergence as both a major market for warehouse automation and a source of innovative automation technologies.

Japan's warehouse automation market is characterized by particularly sophisticated applications driven by severe labor shortages and a cultural emphasis on precision and efficiency. Japanese companies have been pioneers in developing advanced robotics technologies, and this expertise is increasingly being applied to warehouse automation applications. The integration of Japanese precision manufacturing capabilities with warehouse automation requirements has created opportunities for highly sophisticated and reliable automation solutions.

India represents one of the most promising emerging markets for warehouse automation, driven by rapid economic growth, expanding e-commerce markets, and increasing integration with global supply chains. Companies like Addverb Technologies demonstrate the potential for Indian companies to develop competitive automation technologies while serving both domestic and international markets [6]. The large scale of the Indian market and the availability of engineering talent create opportunities for significant growth in warehouse automation adoption.

European Market Sophistication

The European warehouse automation market is characterized by sophisticated applications, strong emphasis on sustainability and energy efficiency, and advanced integration with broader industrial automation strategies. European companies have been leaders in developing energy-efficient automation solutions and integrating sustainability considerations into automation system design.

Germany represents the largest individual European market, benefiting from its strong industrial automation heritage and the presence of major automation technology companies. German companies like KUKA and Schaefer Systems have leveraged their expertise in industrial automation to develop sophisticated warehouse automation solutions that emphasize precision, reliability, and integration capabilities [2].

The United Kingdom market has been driven by the growth of e-commerce and the need to maintain competitive logistics operations in a high-cost labor environment. Brexit has created additional pressures for efficient logistics operations that can manage complex cross-border requirements while maintaining operational efficiency.

France and other Western European markets are demonstrating strong growth in warehouse automation adoption, driven by labor market constraints and the need to remain competitive in global markets. The emphasis on sustainability in European markets has created opportunities for automation solutions that can demonstrate environmental benefits alongside operational improvements.

Eastern European markets are experiencing rapid growth in warehouse automation adoption as these economies integrate more fully with Western European supply chains and develop their own domestic e-commerce markets. The availability of skilled technical talent and lower implementation costs in these markets create opportunities for cost-effective automation deployments.

Emerging Markets and Development Opportunities

Latin American markets are beginning to demonstrate significant potential for warehouse automation adoption, driven by growing e-commerce markets and the need to improve logistics efficiency in challenging geographic environments. Brazil represents the largest market in the region, with opportunities for automation solutions that can address the unique challenges of serving a large, geographically dispersed population.

Middle Eastern markets, particularly the Gulf states, are investing heavily in logistics infrastructure and automation technologies as part of broader economic diversification strategies. The emphasis on developing these regions as global logistics hubs creates opportunities for sophisticated warehouse automation implementations that can serve both regional and international markets.

African markets represent longer-term opportunities for warehouse automation adoption as these economies develop and integrate more fully with global supply chains. The unique challenges of African logistics environments create opportunities for innovative automation solutions that can operate effectively in challenging conditions while providing cost-effective operational improvements.

Regional Technology Preferences and Specializations

Different regions exhibit distinct preferences for specific automation technologies that reflect local market conditions, operational requirements, and technological capabilities. North American markets tend to favor comprehensive automation solutions that emphasize scalability and integration with advanced software platforms. The presence of major technology companies has driven demand for AI-powered automation solutions that can provide sophisticated optimization capabilities.

Asian markets often emphasize cost-effectiveness and rapid deployment capabilities, with strong demand for modular automation solutions that can be implemented incrementally. The manufacturing focus of many Asian economies has created demand for automation solutions that can integrate effectively with production operations and support just-in-time logistics requirements.

European markets typically emphasize sustainability, energy efficiency, and compliance with stringent regulatory requirements. This focus has driven demand for automation solutions that can demonstrate environmental benefits and operate effectively within complex regulatory frameworks.

The regional variations in technology preferences create opportunities for automation companies to develop specialized solutions that address specific regional requirements while building on core technological capabilities that can be adapted for different markets.

Future Outlook and Emerging Trends

The warehouse automation industry stands at the threshold of a transformative period characterized by accelerating technological advancement, expanding market adoption, and the emergence of new paradigms that promise to reshape the fundamental nature of logistics and supply chain operations. Understanding these emerging trends and their potential implications is essential for stakeholders seeking to navigate the evolving landscape and capitalize on future opportunities.

Technological Convergence and Integration

The future of warehouse automation will be increasingly defined by the convergence of multiple advanced technologies that create synergistic effects and enable capabilities that exceed the sum of their individual components. The integration of artificial intelligence, machine learning, computer vision, and advanced robotics is creating automation solutions that can adapt dynamically to changing operational requirements and continuously improve their performance through experience and data analysis.

The concept of "Physical AI," exemplified by partnerships such as the collaboration between Kion Group, Nvidia, and Accenture, represents a fundamental shift toward more intelligent and adaptive automation systems [6]. These systems will be capable of learning from operational data, predicting maintenance requirements, optimizing performance parameters, and adapting to new tasks without extensive reprogramming or reconfiguration.

The integration of Internet of Things (IoT) sensors and edge computing capabilities is enabling real-time monitoring and optimization of warehouse operations at unprecedented levels of granularity. These technologies allow for continuous tracking of system performance, environmental conditions, and operational efficiency, enabling predictive maintenance and dynamic optimization that can significantly improve overall system reliability and performance.

Humanoid Robotics and Advanced Manipulation

The emergence of humanoid robotics represents one of the most significant potential paradigm shifts in warehouse automation. Companies like Agility Robotics with their Digit robot and Apptronik with their versatile humanoid systems are developing robots that can perform tasks in environments designed for human workers without requiring extensive infrastructure modifications [6]. This capability could dramatically expand the range of applications where automation can provide value while reducing the barriers to automation adoption.

The development of advanced manipulation capabilities, exemplified by Amazon's Vulcan robot with its sense of touch, is enabling robots to handle increasingly complex and delicate tasks that were previously the exclusive domain of human workers [5]. These advances in tactile feedback and force control are opening new possibilities for automated picking, packing, and quality control operations.

The integration of advanced computer vision and AI-powered object recognition is enabling robots to handle the inherent variability of warehouse operations more effectively. Future systems will be capable of recognizing and manipulating objects they have never encountered before, adapting their handling strategies based on visual and tactile feedback, and learning from each interaction to improve future performance.

Sustainability and Environmental Considerations

Sustainability considerations are becoming increasingly important drivers of warehouse automation development and adoption. Future automation systems will need to demonstrate not only operational efficiency improvements but also environmental benefits through reduced energy consumption, optimized space utilization, and minimized waste generation.

The development of energy-efficient automation systems is becoming a critical competitive factor, with companies increasingly focused on solutions that can reduce overall energy consumption while improving operational performance. Advanced battery technologies, regenerative braking systems, and intelligent power management are enabling more sustainable automation operations.

The integration of renewable energy sources with warehouse automation systems is creating opportunities for carbon-neutral or carbon-negative logistics operations. Solar panels, wind generation, and energy storage systems are being integrated with automation infrastructure to create self-sufficient operations that can operate independently of traditional power grids.

Scalability and Accessibility

Future developments in warehouse automation will focus increasingly on making these technologies more accessible to smaller operations and more scalable for rapid deployment. The trend toward modular, plug-and-play automation solutions is reducing the complexity and cost of automation implementations while enabling more flexible and adaptable systems.

Cloud-based automation platforms are enabling smaller companies to access sophisticated automation capabilities without requiring substantial upfront investments in infrastructure and expertise. These platforms provide automation-as-a-service models that can scale dynamically with operational requirements while providing access to advanced analytics and optimization capabilities.

The development of standardized interfaces and communication protocols is enabling better integration between automation systems from different vendors, reducing vendor lock-in and enabling more flexible and cost-effective automation implementations.

Market Expansion and New Applications

The warehouse automation market is expected to expand beyond traditional logistics applications to encompass new sectors and use cases that were previously considered unsuitable for automation. Healthcare logistics, pharmaceutical distribution, and food service operations are emerging as significant growth areas where specialized automation solutions can provide substantial value.

The integration of warehouse automation with broader supply chain optimization is creating opportunities for end-to-end automation solutions that can optimize operations across multiple facilities and transportation networks. These integrated approaches promise to deliver greater efficiency improvements than isolated automation implementations.

The development of micro-fulfillment centers and distributed logistics networks is creating new applications for compact, high-density automation solutions that can operate effectively in urban environments and provide rapid delivery capabilities for e-commerce operations.

Challenges and Opportunities

The warehouse automation industry faces a complex landscape of challenges and opportunities that will shape its development trajectory and determine which companies and technologies achieve long-term success. Understanding these factors is crucial for stakeholders seeking to navigate the evolving market and make informed strategic decisions.

Technical and Implementation Challenges

The integration complexity of modern warehouse automation systems represents one of the most significant challenges facing the industry. As automation solutions become more sophisticated and comprehensive, the technical expertise required for successful implementation increases correspondingly. Companies must navigate complex interactions between hardware systems, software platforms, and existing operational processes while ensuring that new automation capabilities integrate effectively with legacy systems and established workflows.

The challenge of handling product variability continues to constrain automation applications in many warehouse environments. While advances in computer vision and AI have improved robots' ability to recognize and manipulate diverse objects, the infinite variety of products, packaging types, and handling requirements in modern warehouses still presents significant technical challenges that require ongoing innovation and development.

Maintenance and reliability requirements for warehouse automation systems are becoming increasingly demanding as operations become more dependent on automated systems for continuous operation. The need for predictive maintenance capabilities, rapid fault diagnosis, and minimal downtime requirements creates ongoing challenges for system designers and operators.

Economic and Financial Considerations

The capital-intensive nature of warehouse automation implementations continues to present barriers to adoption, particularly for smaller operations and companies with limited access to capital. While the total cost of ownership for automation systems has generally decreased over time, the upfront investment requirements remain substantial and require careful financial planning and justification.