Defense Technology Investment Analysis: A Comprehensive Market Report

Prepared by: Bogdan Cristei & Manus AI

Date: June 13, 2025

Executive Summary

The defense technology sector is experiencing an unprecedented transformation, driven by geopolitical tensions, technological breakthroughs, and a fundamental shift in how the Department of Defense approaches innovation. This comprehensive analysis examines the investment landscape, key players, capital flows, and strategic opportunities in defense tech, providing actionable insights for active investors seeking to capitalize on this rapidly evolving market.

Key findings include a resilient funding environment with $9.1 billion invested across 228 deals in 2024 despite broader venture capital slowdowns, the emergence of defense tech unicorns valued at $50 billion combined, and a strategic paradigm shift toward private sector collaboration that is reshaping national security infrastructure. The sector presents compelling investment opportunities across AI and autonomy, hypersonic weapons, directed energy systems, space infrastructure, and cybersecurity, with near-term catalysts including the Air Force's plan for 1,000+ AI-enabled unmanned aircraft systems by 2028 and the Department of Defense's record $1 trillion budget proposal.

1. Investment Thesis: The Defense Tech Renaissance

Why Defense Tech is Gaining Attention Now

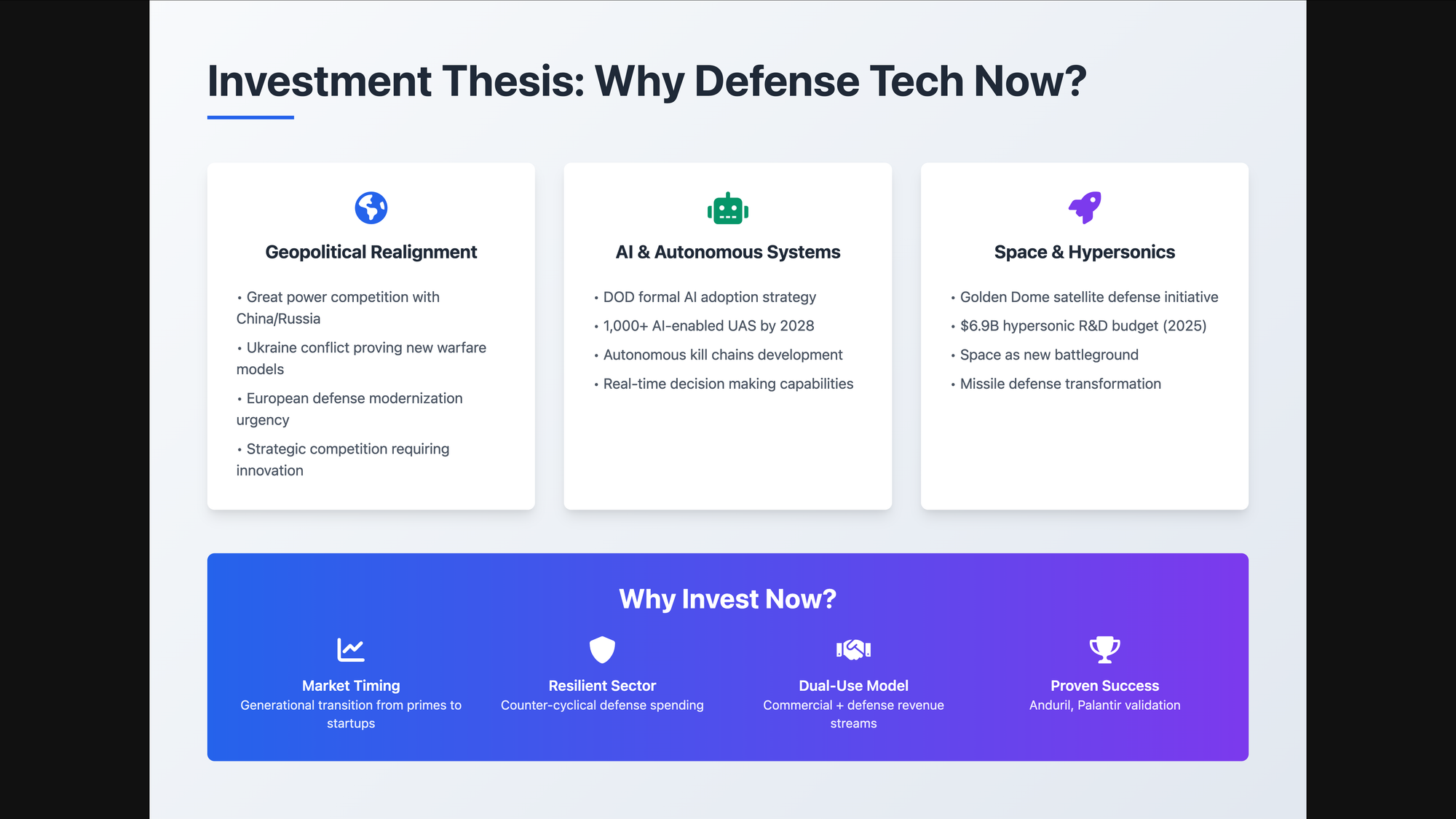

The defense technology sector is experiencing a renaissance driven by converging macro trends that have fundamentally altered the investment landscape. After decades of being dominated by traditional prime contractors, the defense industry is undergoing a technological transformation that presents unprecedented opportunities for venture investors and growth-stage companies.

The primary catalyst for this transformation is the recognition that modern warfare and national security challenges require rapid innovation cycles that traditional defense contractors cannot provide [1]. The Department of Defense has acknowledged this reality, with Defense Secretary Lloyd Austin stating that the Pentagon has great potential to become "a true innovation ecosystem" [2]. This represents a generational paradigm shift from the traditional model where defense innovation was confined to a handful of large prime contractors to one where startups and emerging technology companies play a critical role in national security.

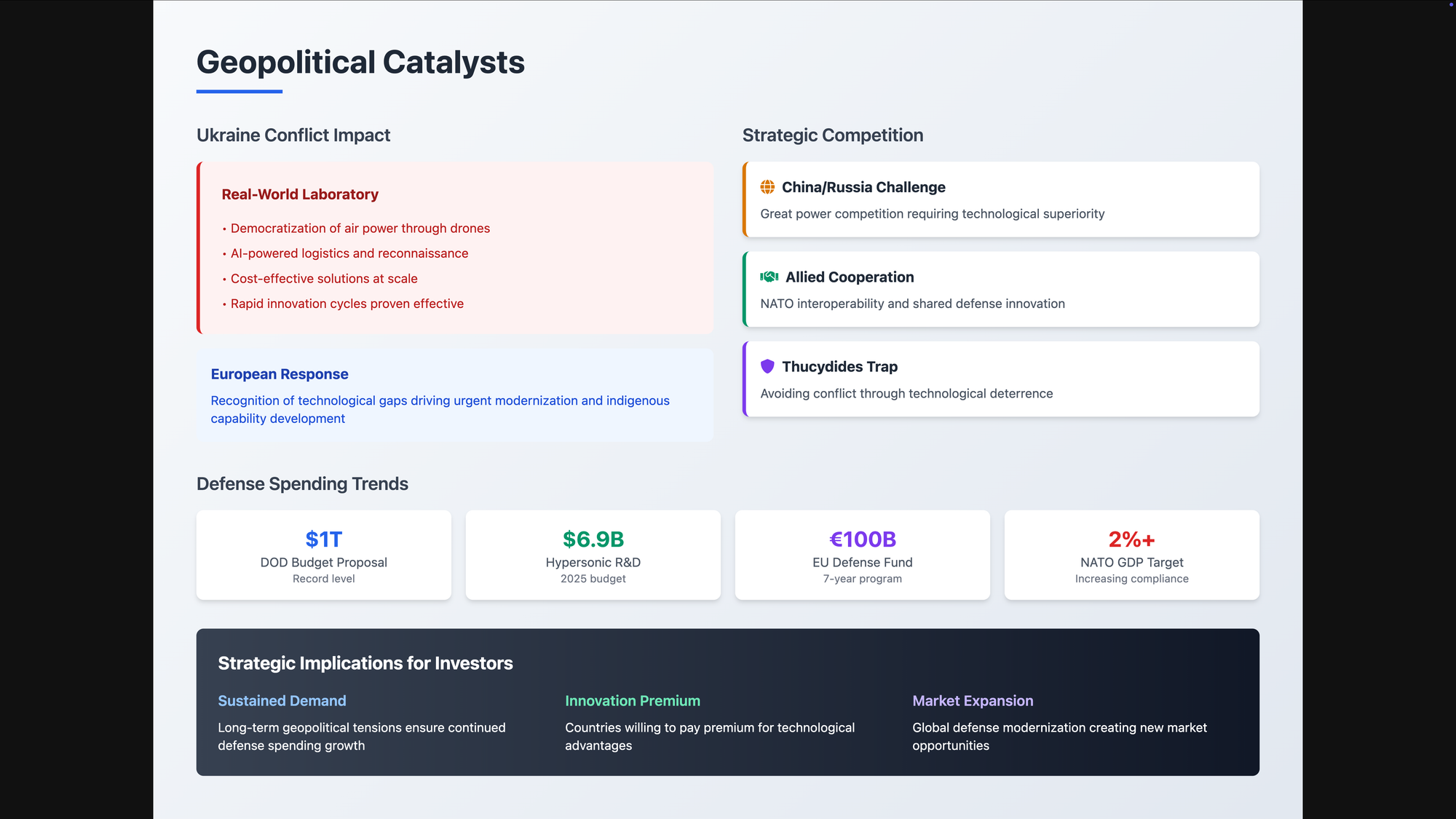

Geopolitical tensions have intensified the urgency for defense innovation. The ongoing conflict in Ukraine has served as a real-world laboratory for defense technologies, demonstrating the effectiveness of autonomous systems, AI-powered decision making, and cost-effective solutions that can be rapidly deployed and scaled [3]. European nations, in particular, are recognizing their technological gaps and the need to modernize defense capabilities, creating new market opportunities for innovative defense tech companies.

Macro Trends Driving the Defense Tech Surge

Geopolitical Realignment and Strategic Competition

The return of great power competition, particularly with China and Russia, has fundamentally altered defense spending priorities and innovation requirements. The National Security Innovation Base is being called upon to gear up for "long-term strategic competition" [4], requiring technologies that can provide sustained competitive advantages rather than incremental improvements to existing systems.

The Ukraine conflict has demonstrated the democratization of air power through autonomous drones, the effectiveness of AI-powered logistics and reconnaissance systems, and the critical importance of rapid innovation cycles in modern warfare [5]. These lessons are driving defense departments worldwide to seek partnerships with technology companies that can deliver cutting-edge solutions at commercial speeds and scales.

Artificial Intelligence and Autonomous Systems

The integration of artificial intelligence into defense systems represents one of the most significant technological shifts in military history. The Department of Defense has released its formal AI adoption strategy, recognizing that AI and machine learning will be essential for national security objectives [6]. This includes productivity gains from automation, higher quality intelligence outputs, faster assessment capabilities critical in real-time situations, and more accurate insights to drive tactical and strategic decisions.

The Air Force is already preparing for a fleet of over 1,000 AI-enabled unmanned aircraft systems expected to be operational by 2028 [7]. This massive deployment represents not just a technological shift but a fundamental change in how military operations are conducted, creating substantial market opportunities for companies developing autonomous systems, AI software platforms, and supporting infrastructure.

Space as the New Frontier

Space has emerged as a critical domain for national security, with initiatives like Trump's Golden Dome executive order aiming to defend the United States "against ballistic, hypersonic, advanced cruise missiles, and other next-generation aerial attacks" through a network of hundreds of orbiting satellites [8]. This transformation of space into a battleground for missile defense creates opportunities for companies developing satellite technologies, space-based sensors, and orbital defense systems.

Cybersecurity and Digital Warfare

The digital transformation of warfare has made cybersecurity a table stakes requirement for national security. The Biden Administration's Executive Order 14028 on Improving the Nation's Cybersecurity and the Office of Management and Budget's Federal zero trust architecture strategy have created specific requirements and deadlines for cybersecurity modernization [9]. This regulatory environment, combined with increasingly sophisticated threat campaigns, has created a robust market for cybersecurity solutions tailored to defense and government requirements.

The Rationale for Investing in Dual-Use Startups

Dual-use technology companies represent particularly attractive investment opportunities because they can serve both commercial and defense markets, providing multiple revenue streams and reducing dependency on government contracts. These companies often develop technologies for commercial applications first, then adapt them for defense use, allowing them to achieve scale and efficiency advantages that pure-play defense companies cannot match.

The dual-use approach also provides strategic advantages in terms of innovation speed and cost effectiveness. Commercial markets drive rapid iteration cycles and cost optimization that benefit defense applications, while defense contracts provide stable, long-term revenue streams that support continued innovation. Companies like Palantir have demonstrated this model successfully, growing from a defense-focused data analytics company to a broader enterprise software provider with significant commercial revenue [10].

Ethical and Financial Considerations

Investing in defense technology raises important ethical considerations that investors must carefully evaluate. The development of autonomous weapons systems, in particular, has generated significant debate about the role of artificial intelligence in lethal decision-making. However, many investors and entrepreneurs argue that supporting democratic nations' defense capabilities is essential for maintaining global stability and protecting democratic values [11].

From a financial perspective, defense tech investments offer several attractive characteristics. Government contracts typically provide stable, long-term revenue streams with predictable payment schedules. The defense market is also characterized by high barriers to entry once companies establish relationships with government customers, creating sustainable competitive advantages for successful companies.

The sector's resilience during economic downturns is another attractive feature for investors. Defense spending tends to be counter-cyclical, providing stability during periods of economic uncertainty. The current geopolitical environment suggests that defense spending will remain robust for the foreseeable future, supporting continued growth in the sector.

However, investors must also consider the unique challenges of the defense market, including lengthy sales cycles, complex regulatory requirements, and the need for security clearances. Companies must also navigate the political risks associated with defense spending and policy changes that can affect funding priorities.

2. Landscape Overview: Mapping the Defense Tech Ecosystem

Market Structure and Key Players by Stage

The defense technology landscape has evolved from a monolithic structure dominated by traditional prime contractors to a diverse ecosystem spanning early-stage startups to mature public companies. This transformation has created investment opportunities across all stages of company development, each with distinct characteristics and risk-return profiles.

Late-Stage and Mature Players

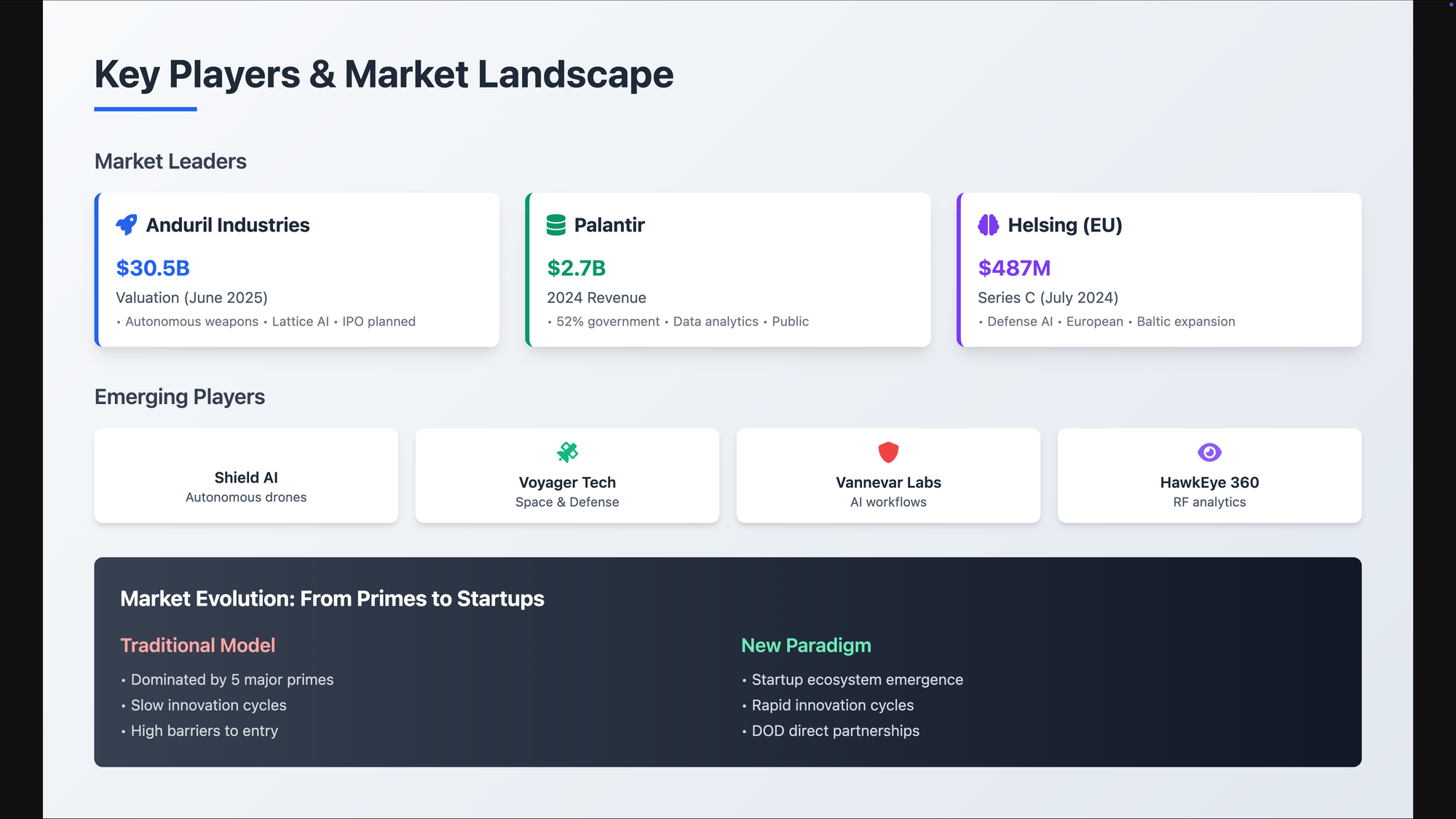

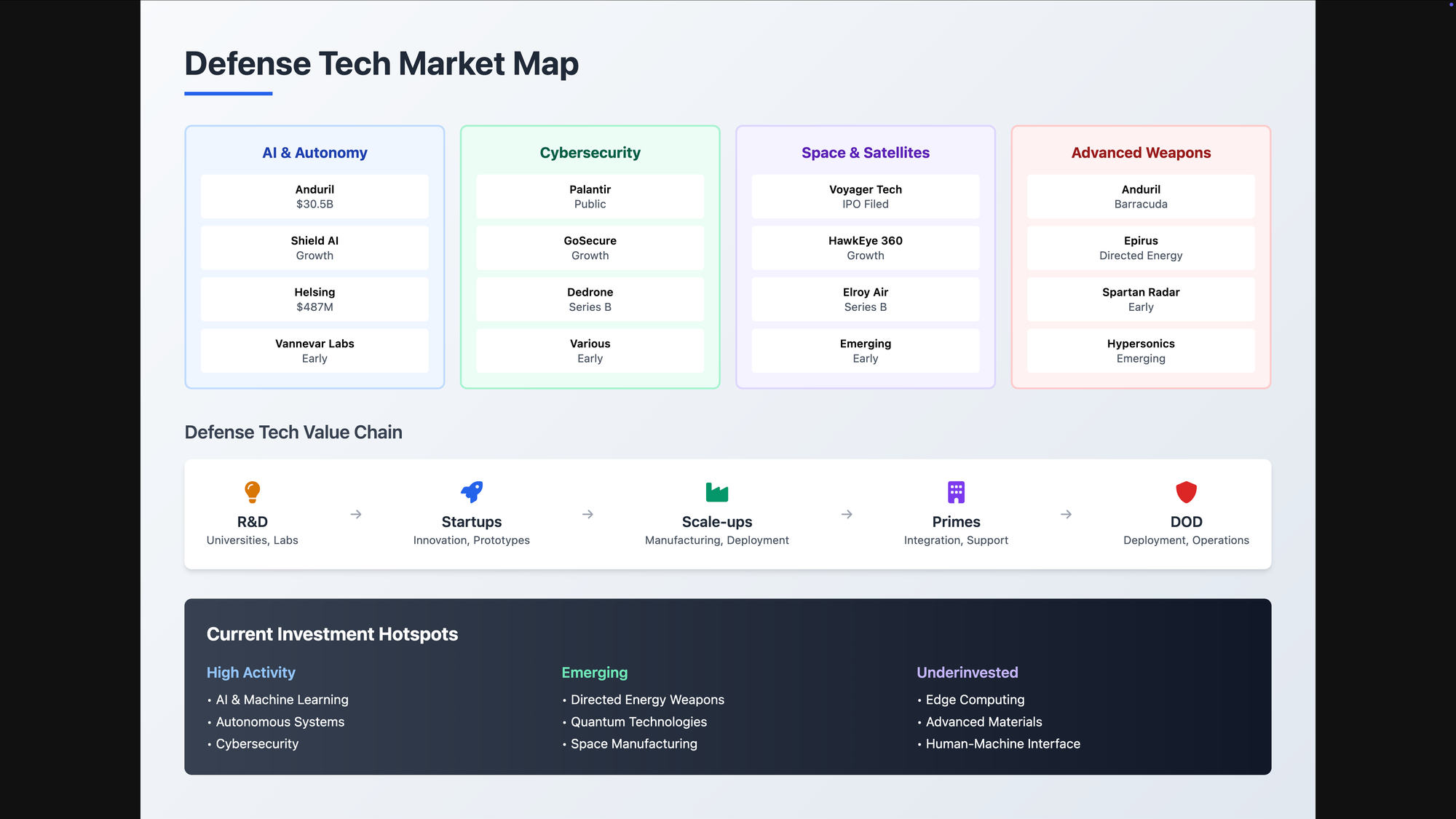

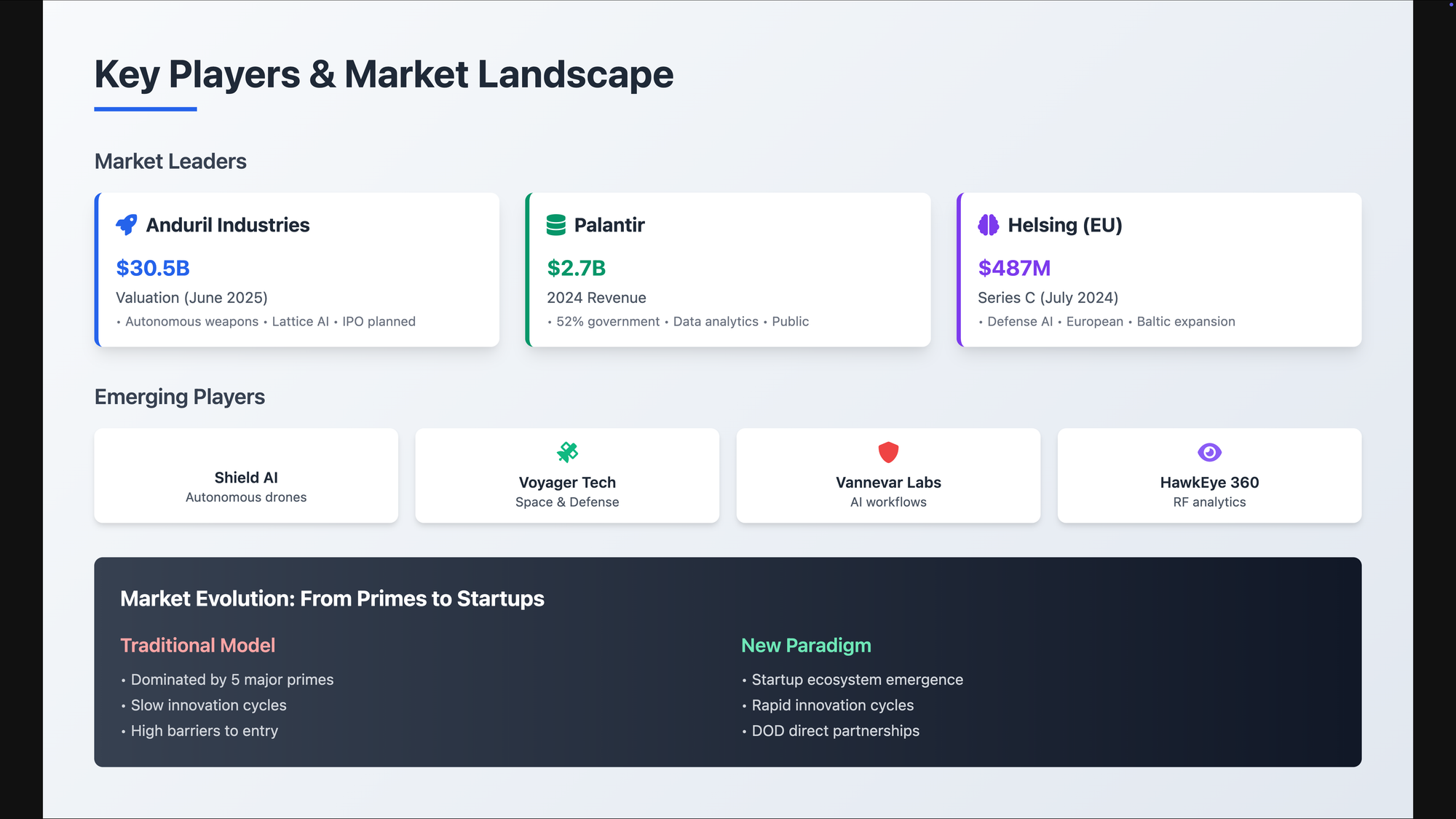

At the apex of the defense tech ecosystem are companies that have achieved significant scale and market validation. Anduril Industries stands as the most prominent example, having recently raised $2.5 billion at a $30.5 billion valuation in June 2025, more than doubling its previous valuation [12]. The company, founded by Palmer Luckey after his departure from Meta, has become a symbol of the new defense tech paradigm, combining cutting-edge technology with innovative manufacturing approaches.

Anduril's success stems from its integrated approach to hardware and software development. The company's Lattice software platform serves as the foundation for its autonomous weapons systems, while its single-flow manufacturing process reduces costs and improves efficiency compared to traditional defense contractors. The Barracuda missile product line exemplifies this approach, using 50% fewer parts and 95% fewer tools than comparable systems, resulting in a 30% reduction in per-unit costs [13].

Palmer Luckey has confirmed that Anduril will "definitely" go public, stating that there is no viable path for a company like Anduril to win significant trillion-dollar defense contracts without being publicly traded [14]. This IPO, when it occurs, will likely serve as a watershed moment for the defense tech sector, potentially unlocking additional capital and legitimizing the space for institutional investors.

Palantir Technologies represents another category of mature defense tech company, having successfully transitioned from a pure-play defense contractor to a diversified enterprise software provider. The company reported $2.7 billion in total revenue for 2024, with government revenue of $1.4 billion representing 52% of total revenue [15]. Palantir's success demonstrates the viability of the dual-use model, where companies can leverage defense contracts to fund innovation while expanding into commercial markets.

Growth-Stage Companies

The growth-stage segment includes companies that have achieved product-market fit and are scaling their operations. Helsing, a German defense AI company, exemplifies this category, having raised $487 million in Series C funding in July 2024 [16]. The company focuses on AI-powered defense solutions for European markets, addressing the growing demand for indigenous defense capabilities in Europe.

Shield AI represents another significant growth-stage player, specializing in autonomous aircraft systems. The company's Hivemind AI software enables drones and other autonomous systems to operate without GPS, creating geographic maps using onboard sensors and cameras [17]. Their V-BAT drone, weighing 125 pounds and measuring 9 feet long, can be deployed within fifteen minutes by a three-person team and is already being used in Ukraine for surveillance and reconnaissance missions.

Early-Stage Startups

The early-stage segment is characterized by companies developing innovative technologies across various defense applications. These companies typically focus on specific technical challenges or market niches, often with dual-use potential. The diversity of early-stage companies reflects the broad scope of defense technology needs, from cybersecurity and data analytics to autonomous systems and advanced materials.

Many early-stage companies are emerging from university research programs or are founded by veterans with deep understanding of defense requirements. These companies often begin by addressing specific pain points identified through military experience, then expand their solutions to broader applications.

Active Venture Capital Firms and Investment Strategies

The defense tech investment landscape is characterized by a mix of specialized defense-focused funds and traditional venture capital firms that have developed defense tech practices. Each category brings different strengths and investment approaches to the sector.

Early-Stage Specialized Funds

Shield Capital has emerged as one of the most prominent early-stage defense tech investors, having closed a $186 million inaugural fund in October 2023 [18]. The firm focuses on companies at the convergence of commercial technology and national security, with investments spanning AI, autonomy, cybersecurity, and space technologies. Shield Capital's portfolio includes over 30 companies, including GoSecure, HawkEye 360, Elroy Air, Vannevar Labs, and Dedrone.

The firm's approach emphasizes mission-focused investing with deep national security expertise. Shield Capital's team includes veteran investors, founders, and national security leaders who can provide strategic guidance beyond capital. This combination of financial resources and domain expertise has made Shield Capital a preferred partner for defense tech entrepreneurs.

Lux Capital represents another significant early-stage investor in defense tech, though with a broader deep tech focus. The firm has invested in companies developing breakthrough technologies across multiple sectors, including defense applications. Lux Capital's approach emphasizes supporting contrarian entrepreneurs working on transformative technologies that can reshape entire industries.

Scout Ventures focuses specifically on military and veteran entrepreneurs, providing both capital and mentorship to companies founded by individuals with military backgrounds. This approach leverages the unique insights and networks that military veterans bring to defense technology development.

Later-Stage and Growth Investors

Founders Fund, led by Peter Thiel, has been one of the most active later-stage investors in defense tech. The firm led Anduril's recent $2.5 billion funding round and has a history of supporting companies developing transformative technologies with national security implications [19]. Founders Fund's approach emphasizes supporting companies that can achieve technological breakthroughs rather than incremental improvements.

Andreessen Horowitz (a16z) has developed a significant defense tech practice, investing in companies across the spectrum from cybersecurity to autonomous systems. The firm's approach combines traditional venture capital expertise with specialized knowledge of defense markets and requirements.

DCVC (Data Collective) focuses on deep tech companies with applications across multiple sectors, including defense. The firm's approach emphasizes supporting companies developing breakthrough technologies in areas like artificial intelligence, robotics, and advanced materials.

General Catalyst has expanded its defense tech investments in recent years, recognizing the sector's growth potential and strategic importance. The firm's approach emphasizes supporting companies that can scale rapidly while maintaining technological leadership.

Government and Strategic Investors

In-Q-Tel, the CIA's venture capital arm, plays a unique role in the defense tech ecosystem by providing both capital and strategic guidance to companies developing technologies relevant to intelligence and national security applications. In-Q-Tel's investments often serve as validation for other investors and can provide companies with access to government customers and requirements.

The Defense Innovation Unit (DIU) operates as a bridge between the Department of Defense and the technology sector, providing funding and support for companies developing solutions to specific defense challenges. While not a traditional venture capital firm, DIU's programs often serve as stepping stones for companies seeking to establish relationships with defense customers.

Regional Differences and International Players

The defense tech landscape varies significantly by region, reflecting different regulatory environments, defense spending priorities, and technological capabilities. Understanding these regional differences is crucial for investors seeking to identify opportunities and assess competitive dynamics.

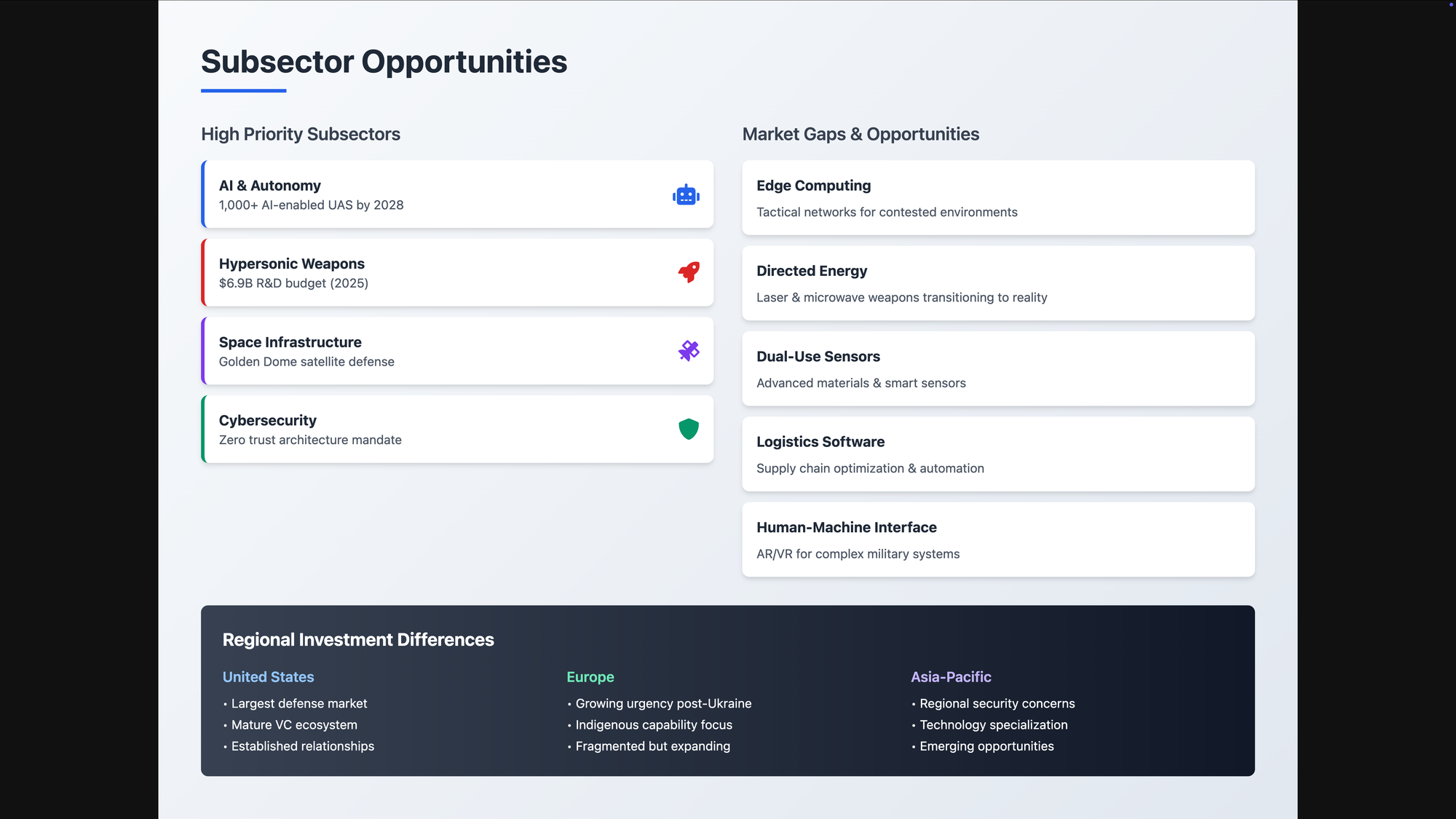

United States Market

The U.S. market remains the largest and most developed defense tech ecosystem, benefiting from substantial defense spending, a robust venture capital industry, and a regulatory environment that supports innovation. The Department of Defense's emphasis on working with startups and non-traditional contractors has created numerous opportunities for emerging companies.

American companies also benefit from access to the world's largest defense market and established relationships with allied nations. The U.S. regulatory framework, while complex, provides clear pathways for companies to obtain necessary security clearances and certifications.

European Market

Europe represents a rapidly growing market for defense tech investment, driven by the recognition that European nations need to develop indigenous defense capabilities. The Ukraine conflict has accelerated this trend, with European governments increasing defense spending and seeking partnerships with technology companies.

Helsing's success in raising $487 million demonstrates the viability of European defense tech companies and the growing investor interest in the region [20]. European companies often focus on developing technologies that can reduce dependence on American defense systems while meeting NATO interoperability requirements.

The European market is characterized by fragmentation across multiple national markets, each with its own regulatory requirements and procurement processes. However, initiatives like the European Defence Fund are working to create more integrated approaches to defense technology development and procurement.

Emerging Markets and International Players

Other regions are also developing defense tech capabilities, though often with different focuses and constraints. Israeli companies have long been leaders in cybersecurity and surveillance technologies, leveraging the country's security challenges to develop innovative solutions with global applications.

Asian markets, particularly South Korea and Japan, are investing heavily in defense technologies as regional security concerns increase. These markets often focus on specific technological areas where they have existing strengths, such as electronics and manufacturing.

3. Capital Flows & Trends: Investment Data and Market Dynamics

Recent Investment Data and Funding Trends

The defense technology sector has demonstrated remarkable resilience in the face of broader venture capital market challenges. According to PitchBook data, defense tech attracted $9.1 billion in investment across 228 deals in 2024, maintaining strong momentum despite a general slowdown in venture capital dealmaking [21]. This performance underscores the sector's strategic importance and the continued confidence of investors in defense tech opportunities.

The 2024 funding levels represent a normalization from the peak years of 2022-2023, when an unprecedented $70 billion was deployed across both years combined [22]. While this represents a decline from peak levels, the current funding environment remains well above historical norms and reflects a more sustainable pace of investment that focuses on companies with proven business models and clear paths to profitability.

Stage-by-Stage Capital Flow Analysis

Early-stage funding has remained particularly robust, with seed and Series A rounds continuing to attract significant investor interest. This reflects the continued emergence of new companies addressing specific defense technology challenges and the recognition that early-stage investments in defense tech can generate substantial returns as companies scale.

Growth-stage funding has become more selective, with investors focusing on companies that have demonstrated clear product-market fit and established relationships with government customers. The success of companies like Anduril and Palantir has provided proof points for the scalability of defense tech businesses, encouraging larger investments in proven companies.

Late-stage funding has been dominated by a few large rounds, particularly Anduril's $2.5 billion Series G round, which alone represents a significant portion of total defense tech funding for 2025 [23]. These large rounds reflect the capital requirements for scaling defense tech companies and the willingness of investors to make substantial commitments to market leaders.

Geographic Distribution of Investment

The United States continues to dominate defense tech investment, accounting for the majority of both deal volume and total funding. This reflects the size of the U.S. defense market, the maturity of the American venture capital ecosystem, and the regulatory environment that supports defense tech innovation.

European investment in defense tech has grown significantly, driven by geopolitical concerns and the recognition that Europe needs to develop indigenous defense capabilities. Helsing's $487 million Series C round represents one of the largest European defense tech funding rounds to date and signals growing investor confidence in European opportunities [24].

Asian markets have seen more limited venture capital investment in defense tech, though this is beginning to change as regional security concerns increase and governments become more supportive of private sector defense innovation.

Merger and Acquisition Activity

The defense tech M&A market has been active, with $5.2 billion recorded across 36 deals in 2024 [25]. This activity reflects the strategic importance of defense technologies and the willingness of both traditional defense contractors and technology companies to acquire innovative capabilities through acquisitions.

Strategic Acquirer Categories

Traditional defense contractors have been active acquirers, seeking to incorporate new technologies and capabilities into their existing platforms and customer relationships. These acquisitions often focus on software and AI capabilities that can enhance traditional hardware systems.

Technology companies have also been active acquirers, particularly those seeking to expand into defense markets or enhance their existing defense capabilities. These acquisitions often focus on companies with established government relationships and security clearances.

Private equity firms have shown increasing interest in defense tech acquisitions, recognizing the sector's growth potential and the stability of government contracts. Private equity involvement has been particularly notable in cybersecurity and data analytics companies serving defense markets.

Notable Acquisition Trends

Software and AI companies have commanded premium valuations in M&A transactions, reflecting the strategic importance of these capabilities for defense applications. Companies with proprietary AI algorithms or specialized software platforms have been particularly attractive acquisition targets.

Companies with established government relationships and security clearances have also commanded premium valuations, as these assets are difficult to replicate and provide immediate market access for acquirers.

Dual-use companies have been attractive acquisition targets because they provide access to both commercial and defense markets, offering acquirers multiple growth vectors and reduced dependency on government spending cycles.

IPO Trends and Public Market Performance

The defense tech IPO market has been relatively quiet in recent years, though this is beginning to change as companies reach sufficient scale and maturity. Voyager Technologies filed for an IPO in May 2025, potentially valued at up to $1.6 billion, marking one of the few defense tech public offerings in recent years [26].

Anduril's confirmed plans to go public represent a significant catalyst for the sector, as the company's IPO will likely serve as a benchmark for other defense tech companies considering public offerings. Palmer Luckey's statement that there is "no path" to win trillion-dollar defense contracts without being public suggests that other large defense tech companies may follow suit [27].

Public Market Valuation Trends

Existing public defense tech companies have generally performed well, with investors recognizing the strategic importance of defense technologies and the stability of government contracts. Palantir, for example, has maintained strong public market performance despite broader technology sector volatility.

The public markets have shown particular interest in companies with diversified revenue streams that include both government and commercial customers. This dual-use model provides stability and growth potential that pure-play defense companies may lack.

Factors Driving IPO Activity

Several factors are driving increased IPO activity in defense tech. The scale requirements for major defense contracts often necessitate public company status, as government customers prefer working with established, transparent organizations. Access to public capital markets also provides the funding necessary to compete for large-scale defense programs.

The maturation of the defense tech ecosystem has also created a pipeline of companies with sufficient scale and financial performance to support public offerings. As more companies reach this threshold, IPO activity is likely to increase.

Investment Performance and Returns

Defense tech investments have generally delivered strong returns for investors, though performance varies significantly by stage, vintage year, and specific company characteristics. Early-stage investments in companies that have successfully scaled to serve major defense customers have generated particularly strong returns.

Return Drivers

Several factors have driven strong returns in defense tech investments. The stability of government contracts provides predictable revenue streams that support consistent growth and profitability. The high barriers to entry in defense markets create sustainable competitive advantages for successful companies.

The dual-use model has been particularly effective in driving returns, as companies can leverage defense contracts to fund expansion into commercial markets, creating multiple growth vectors and reducing customer concentration risk.

Risk Factors

Defense tech investments also face unique risks that can impact returns. Regulatory changes and shifts in defense spending priorities can affect market opportunities and company performance. The lengthy sales cycles typical in defense markets can delay revenue recognition and impact cash flow.

Security clearance requirements and export control regulations can limit companies' ability to expand internationally or work with certain customers, potentially constraining growth opportunities.

Future Capital Flow Projections

Looking forward, several trends are likely to shape capital flows in defense tech. The continued geopolitical tensions and focus on strategic competition suggest that defense spending will remain robust, supporting continued investment in defense technologies.

The maturation of the defense tech ecosystem is likely to drive increased late-stage and growth investment as more companies reach scale and demonstrate proven business models. This may come at the expense of early-stage investment as investors become more selective about new opportunities.

The success of companies like Anduril and Palantir is likely to attract additional institutional capital to the sector, potentially increasing competition for deals and driving up valuations. However, the specialized nature of defense markets may limit the number of investors willing to develop the necessary expertise and relationships.

4. Opportunity Map: Promising Subsectors and Market Gaps

AI & Autonomy: The Next Frontier of National Security

Artificial intelligence and autonomous systems represent the most transformative opportunity in defense technology, fundamentally changing how military operations are conducted and creating substantial market opportunities for innovative companies. The Department of Defense has formally embraced AI adoption, recognizing that artificial intelligence and machine learning will be essential for achieving national security objectives [28].

The scope of AI applications in defense is vast, encompassing everything from autonomous weapons systems to logistics optimization and intelligence analysis. The Air Force's preparation for a fleet of over 1,000 AI-enabled unmanned aircraft systems by 2028 represents just one example of the massive scale at which AI technologies will be deployed [29].

Autonomous Drone Systems and Swarm Intelligence

The democratization of air power through autonomous drones has emerged as one of the most significant developments in modern warfare. Real-time innovations from the Ukraine conflict have demonstrated the effectiveness of AI-powered drone systems for surveillance, reconnaissance, and precision strikes [30]. These systems can operate without GPS, creating geographic maps using onboard sensors and cameras, allowing them to evade anti-drone frequency-jamming defenses.

Shield AI's Hivemind platform exemplifies the potential of autonomous drone technology. The company's V-BAT drone can be deployed within fifteen minutes by a three-person team and launched vertically from boats or buildings, demonstrating the operational flexibility that autonomous systems provide [31]. The fact that these systems are already being deployed in Ukraine for surveillance and reconnaissance missions validates their real-world effectiveness.

The future battlefield will likely see even greater integration of autonomous systems, including AI-enabled drones flying alongside piloted fighter jets and fully autonomous F-16s designed for human-machine dogfighting. This evolution creates opportunities for companies developing AI software platforms, autonomous hardware systems, and the supporting infrastructure required for large-scale deployment.

AI-Powered Decision Making and Kill Chains

The development of autonomous kill chains represents one of the most significant long-term opportunities in defense AI. These systems enable creating kill chains "by exception near the time of need when that need is much less uncertain" [32]. This paradigm shift from pre-planned operations to real-time, AI-driven decision making has the potential to fundamentally change military strategy and tactics.

Companies developing AI algorithms for real-time threat assessment, target identification, and engagement decision making are positioned to capture significant value as these systems are deployed at scale. The technical challenges are substantial, requiring AI systems that can operate reliably in contested environments while maintaining appropriate human oversight and control.

Hypersonic Weapons and Advanced Propulsion

Hypersonic weapons represent a critical technology area where the United States is working to maintain competitive parity with adversaries like China and Russia. The Department of Defense has requested $6.9 billion in R&D for hypersonic weapons in 2025, up from $4.7 billion in fiscal year 2023, demonstrating the priority placed on these technologies [33].

Hypersonic Glide Vehicles and Cruise Missiles

Unlike traditional ballistic missiles that follow predetermined arcs, hypersonic glide vehicles (HGVs) and hypersonic cruise missiles (HCMs) can maneuver mid-flight at speeds exceeding Mach 5. HGVs are launched by rockets and glide toward targets, while HCMs use air-breathing engines to maintain hypersonic speeds. This maneuverability makes them extremely difficult to intercept and provides significant tactical advantages.

Anduril Industries has emerged as a leader in this space through its innovative approach to missile design and manufacturing. The company's Barracuda product line uses up to 50% fewer parts and 95% fewer tools than existing systems, leading to a 30% reduction in per-unit missile cost [34]. The Barracuda-250 has a range exceeding 370 kilometers when air-launched and over 278 kilometers when ground-launched, with a payload capacity of 16 kilograms.

Manufacturing Innovation and Cost Reduction

The key to success in hypersonic weapons is not just technical performance but also the ability to manufacture these systems at scale and reasonable cost. Anduril's single-flow manufacturing process, similar to approaches used by companies like Toyota, reduces inventory costs, enhances quality, increases flexibility, and boosts productivity [35].

This manufacturing innovation is critical because hypersonic weapons are likely to be consumed in large quantities during conflicts, requiring production capabilities that can scale rapidly. Companies that can combine technical excellence with manufacturing efficiency are positioned to capture significant market share as these weapons are deployed at scale.

Directed Energy Weapons: From Science Fiction to Reality

Directed energy weapons (DEWs) represent an emerging technology area that is transitioning from science fiction to battlefield reality. These systems use concentrated energy to neutralize threats and fall into two main categories: high-energy lasers that emit focused beams of photons, and high-power microwaves that shoot radio-frequency waves to disrupt or destroy electronics [36].

High-Energy Laser Systems

Laser weapons offer high accuracy and low-cost deployment, making them especially effective for prolonged air, sea, and space-based warfare. The cost per shot for laser weapons is significantly lower than traditional kinetic weapons, making them attractive for defending against swarms of low-cost threats like drones.

The technical challenges for laser weapons include power generation, beam control, and thermal management. Companies developing breakthrough technologies in these areas are positioned to capture significant value as laser weapons are deployed more widely.

High-Power Microwave Systems

Microwave weapons can stealthily disable electronics in drones, radio-controlled bombs, or radar systems from a distance. These systems are particularly effective against electronic threats and can provide area denial capabilities without causing permanent damage to infrastructure.

The development of high-power microwave systems requires expertise in radio frequency engineering, power electronics, and antenna design. Companies with capabilities in these areas are well-positioned to address the growing demand for electronic warfare capabilities.

Space Infrastructure and Satellite Defense

Space has emerged as a critical domain for national security, with initiatives like the Golden Dome project envisioning a network of hundreds of orbiting satellites to detect, track, and potentially intercept incoming missiles [37]. This transformation of space into a battleground for missile defense creates substantial opportunities for companies developing space-based technologies.

Satellite Constellations and Space-Based Sensors

The Golden Dome initiative represents a fundamental shift from ground-based radar and interceptors to space-based surveillance and attack systems. This requires the development of large satellite constellations with sophisticated sensors and communication capabilities.

Companies developing small satellites, space-based sensors, and satellite communication systems are positioned to benefit from this trend. The technical challenges include developing satellites that can operate reliably in contested space environments while maintaining the precision required for missile defense applications.

Space Domain Awareness and Debris Tracking

As space becomes more congested and contested, the ability to track and characterize objects in space becomes increasingly important. Companies developing space domain awareness capabilities, including ground-based and space-based sensors, are addressing a critical need for national security.

The commercial space industry's rapid growth has created additional demand for space domain awareness capabilities, providing dual-use opportunities for companies in this space.

Cybersecurity and Digital Warfare

Cybersecurity has become a table stakes requirement for national security, with the Biden Administration's Executive Order 14028 and the Office of Management and Budget's Federal zero trust architecture strategy creating specific requirements and deadlines for cybersecurity modernization [38].

Zero Trust Architecture and Network Security

The implementation of zero trust architecture across federal agencies requires sophisticated cybersecurity solutions that can verify and authenticate every user and device attempting to access network resources. This creates opportunities for companies developing identity management, network security, and endpoint protection solutions.

The complexity of modern IT environments, including cloud, on-premise, and hybrid deployments, requires cybersecurity solutions that can operate across multiple environments while maintaining consistent security policies.

AI-Powered Threat Detection and Response

The increasing sophistication of cyber threats requires AI-powered solutions that can detect and respond to attacks in real-time. Companies developing machine learning algorithms for threat detection, automated incident response, and predictive security analytics are addressing critical needs in the defense cybersecurity market.

The challenge is developing AI systems that can operate effectively against adversarial AI, where attackers are also using artificial intelligence to evade detection and enhance their capabilities.

Market Gaps and Investment Opportunities

Several market gaps present attractive investment opportunities for companies that can address unmet needs in the defense technology ecosystem.

Edge Computing and Tactical Networks

Military operations often occur in environments with limited or unreliable network connectivity, creating demand for edge computing solutions that can process data locally and operate independently of centralized systems. Companies developing ruggedized edge computing platforms and tactical networking solutions are addressing critical operational needs.

Dual-Use Sensors and Advanced Materials

The development of advanced sensors and materials with both commercial and defense applications presents attractive dual-use opportunities. Companies developing breakthrough sensor technologies, advanced composites, and smart materials can serve multiple markets while reducing dependency on defense spending cycles.

Logistics Software and Supply Chain Optimization

Military logistics and supply chain management present significant opportunities for software companies that can optimize complex, global supply chains while meeting security and regulatory requirements. The scale and complexity of military logistics create substantial value creation opportunities for companies that can deliver meaningful efficiency improvements.

Human-Machine Interface Technologies

As military systems become more complex and autonomous, the need for effective human-machine interfaces becomes increasingly important. Companies developing augmented reality, virtual reality, and advanced user interface technologies for military applications are addressing critical needs for operational effectiveness.

Regional Investment Differences

Investment opportunities in defense tech vary significantly by region, reflecting different regulatory environments, defense spending priorities, and technological capabilities.

United States Opportunities

The U.S. market offers the largest and most diverse set of opportunities, with substantial defense spending and a regulatory environment that supports innovation. American companies benefit from access to the world's largest defense market and established relationships with allied nations.

European Market Development

Europe represents a rapidly growing market driven by the recognition that European nations need indigenous defense capabilities. The fragmentation across multiple national markets creates both challenges and opportunities, with companies that can navigate multiple regulatory environments positioned to capture significant market share.

Emerging Market Potential

Other regions are developing defense tech capabilities, often focusing on specific technological areas where they have existing strengths. These markets may offer opportunities for companies seeking to expand internationally or access specialized capabilities and talent.

5. Future Outlook: Evolution and Strategic Implications

Near-Term Catalysts (1-3 Years)

The defense technology sector is positioned for significant growth in the near term, driven by several catalysts that are already beginning to materialize. The most immediate driver is the operational deployment of AI-enabled systems across multiple domains, with the Air Force's plan for over 1,000 AI-enabled unmanned aircraft systems by 2028 serving as a concrete milestone [39].

AI and Machine Learning Integration

The Department of Defense's formal AI adoption strategy is moving from planning to implementation, creating immediate opportunities for companies developing AI solutions for defense applications. This includes productivity gains from automation of manual tasks, higher quality output documents and work products, faster speed to assessment in real-time situations, and more accurate insights to drive tactical and strategic decisions [40].

The integration of AI into existing defense systems represents a massive modernization effort that will require substantial investment in both new technologies and the integration services necessary to deploy them effectively. Companies with proven AI capabilities and experience working with government customers are positioned to capture significant value from this transition.

Cybersecurity Modernization Mandates

The federal zero trust architecture strategy requires agencies to meet specific cybersecurity standards and objectives, creating immediate demand for cybersecurity solutions tailored to government requirements [41]. The complexity of implementing zero trust across diverse IT environments creates opportunities for companies that can provide comprehensive solutions and integration services.

The increasing sophistication of cyber threats, particularly from nation-state actors, is driving demand for advanced cybersecurity capabilities that can operate effectively in contested environments. This creates opportunities for companies developing AI-powered threat detection, automated incident response, and advanced encryption technologies.

Space Infrastructure Development

The Golden Dome initiative and other space-based defense programs are moving from concept to implementation, creating immediate opportunities for companies developing satellite technologies, space-based sensors, and ground support systems [42]. The scale of these programs requires substantial private sector participation, creating opportunities for both established space companies and emerging startups.

Medium-Term Evolution (3-7 Years)

The medium-term outlook for defense technology is characterized by the maturation of emerging technologies and the evolution of defense-private sector partnerships. This period will likely see the full operationalization of autonomous systems, the deployment of hypersonic weapons at scale, and the establishment of space as a primary domain for military operations.

Defense-Private Innovation Partnerships

The relationship between the Department of Defense and private sector technology companies will continue to evolve, with traditional prime contractors increasingly serving as system integrators rather than technology developers. This shift creates opportunities for technology companies to establish direct relationships with government customers while leveraging the integration and program management capabilities of traditional contractors.

The success of companies like Anduril and Palantir in scaling to serve major defense customers will encourage other technology companies to enter the defense market, increasing competition but also expanding the overall market size. This evolution will likely lead to new partnership models and acquisition strategies as traditional defense companies seek to incorporate innovative technologies.

Autonomous Systems Proliferation

The medium term will see the widespread deployment of autonomous systems across air, land, sea, and space domains. This includes not just individual autonomous platforms but also coordinated swarms and human-machine teams that can operate effectively in complex, contested environments.

The technical challenges of deploying autonomous systems at scale will create opportunities for companies developing supporting technologies, including AI software platforms, communication systems, and maintenance and logistics solutions. The need for interoperability across different autonomous systems will also create opportunities for companies developing standards and integration platforms.

Hypersonic Weapons Deployment

The medium term will likely see the operational deployment of hypersonic weapons by multiple nations, creating both offensive and defensive requirements. The need for hypersonic defense systems will drive investment in detection, tracking, and interception technologies, while the deployment of offensive hypersonic weapons will require supporting infrastructure and logistics capabilities.

The manufacturing scale-up required for hypersonic weapons deployment will create opportunities for companies that can provide cost-effective production capabilities while maintaining the precision and reliability required for these advanced systems.

Long-Term Moonshots (7+ Years)

The long-term outlook for defense technology includes several transformative technologies that could fundamentally change the nature of warfare and national security. These moonshot technologies represent both the greatest opportunities and the highest risks for investors willing to support breakthrough innovation.

Autonomous Kill Chains and Lethal Autonomous Weapons

The development of fully autonomous weapons systems that can identify, track, and engage targets without human intervention represents one of the most significant and controversial developments in defense technology. These systems would enable creating kill chains "by exception near the time of need when that need is much less uncertain" [43].

The technical challenges are substantial, requiring AI systems that can operate reliably in contested environments while maintaining appropriate ethical and legal constraints. The development of these systems will also require new frameworks for human oversight and control, creating opportunities for companies developing human-machine interface technologies and decision support systems.

Quantum Defense and Post-Quantum Cryptography

Quantum computing represents both a threat and an opportunity for defense applications. The development of quantum computers capable of breaking current encryption standards will require the deployment of post-quantum cryptography across all defense systems. This transition will create substantial opportunities for companies developing quantum-resistant security technologies.

Quantum technologies also offer potential advantages for defense applications, including quantum sensors with unprecedented precision, quantum communication systems that are inherently secure, and quantum computing capabilities for optimization and simulation problems. Companies developing practical quantum technologies for defense applications are positioned to capture significant value as these technologies mature.

Space-Based Manufacturing and Resource Utilization

The long-term development of space-based manufacturing capabilities and resource utilization could fundamentally change the economics of space-based defense systems. The ability to manufacture and maintain defense systems in space would enable the deployment of much larger and more capable space-based platforms.

This development would create opportunities for companies developing space-based manufacturing technologies, resource extraction capabilities, and the supporting infrastructure required for sustained space-based operations.

Implications of Private Companies as Primary Defense Suppliers

The increasing role of private companies as primary defense suppliers represents a fundamental shift in the defense industrial base with significant strategic implications. This transformation offers both opportunities and risks that must be carefully managed to ensure national security objectives are met.

Positive Strategic Implications

The involvement of private companies in defense technology development brings several strategic advantages. Private companies typically operate with faster innovation cycles than traditional defense contractors, enabling more rapid development and deployment of new capabilities. The commercial technology sector's emphasis on cost optimization and efficiency can also reduce the cost of defense systems while improving their performance.

Private companies also bring access to cutting-edge commercial technologies that can be adapted for defense applications. The dual-use model allows companies to leverage commercial markets to fund continued innovation while providing defense customers with access to the latest technological developments.

Strategic Risks and Mitigation Strategies

The increased reliance on private companies for critical defense capabilities also creates strategic risks that must be carefully managed. The potential for conflicts between commercial and national security interests could affect companies' willingness to prioritize defense requirements over commercial opportunities.

The dependency on private sector innovation also creates vulnerabilities if key companies are acquired by foreign entities or if their commercial businesses fail. This requires careful attention to supply chain security and the development of alternative sources for critical capabilities.

Regulatory and Oversight Implications

The evolution toward private companies as primary defense suppliers will require new regulatory frameworks and oversight mechanisms. Traditional defense acquisition processes may need to be adapted to work effectively with companies that operate primarily in commercial markets.

The need for security clearances and export control compliance will also require new approaches that can accommodate the global nature of modern technology companies while maintaining appropriate security standards.

Market Structure Evolution

The defense technology market structure will continue to evolve as new players enter the market and existing companies adapt to changing requirements. This evolution will create both opportunities and challenges for investors and companies operating in the space.

Consolidation and Partnership Trends

The medium to long term will likely see increased consolidation in the defense tech sector as companies seek to achieve the scale necessary to compete for major defense programs. This consolidation may take the form of traditional acquisitions, strategic partnerships, or new hybrid models that combine the strengths of different types of organizations.

The success of companies like Anduril in achieving substantial scale while maintaining innovation capabilities will likely encourage other companies to pursue similar growth strategies, potentially leading to increased competition for acquisition targets and partnership opportunities.

New Business Model Development

The defense tech sector will likely see the development of new business models that better align private sector capabilities with defense requirements. This could include outcome-based contracting, technology-as-a-service models, and public-private partnerships that share both risks and rewards.

These new business models will require companies to develop new capabilities in areas like program management, risk assessment, and customer relationship management while maintaining their core technological advantages.

6. Strategic Recommendations for Investors

Why Invest in Defense Tech Now

The current environment presents a compelling opportunity for investors to enter the defense technology sector. The convergence of geopolitical tensions, technological breakthroughs, and structural changes in defense procurement creates a unique window for generating substantial returns while supporting national security objectives.

The sector's demonstrated resilience during broader market downturns provides portfolio diversification benefits, while the long-term nature of defense spending cycles offers stability that is increasingly rare in technology investing. The Department of Defense's $1 trillion budget proposal and the global increase in defense spending provide a substantial and growing market for innovative companies [44].

Market Timing Considerations

The defense tech sector is experiencing a generational transition from traditional prime contractors to innovative technology companies. Early investors in this transition are positioned to capture significant value as new market leaders emerge and mature. The success of companies like Anduril and Palantir has validated the investment thesis and created a roadmap for other companies to follow.

The current funding environment, while more selective than peak years, provides opportunities for disciplined investors to access high-quality companies at reasonable valuations. The normalization of funding levels has eliminated some of the froth that characterized peak investment periods while maintaining strong fundamentals.

Strategic Value Creation Opportunities

Defense tech investments offer multiple vectors for value creation beyond traditional financial returns. Companies that successfully serve defense markets often develop capabilities and relationships that can be leveraged for expansion into adjacent markets, creating additional growth opportunities.

The dual-use nature of many defense technologies provides natural expansion paths into commercial markets, reducing customer concentration risk while expanding total addressable markets. This diversification can support higher valuations and more stable growth profiles than pure-play defense companies.

Risk Assessment and Mitigation Strategies

Defense tech investing involves unique risks that require careful assessment and mitigation strategies. Understanding these risks and developing appropriate mitigation approaches is essential for successful investing in the sector.

Regulatory and Political Risks

Defense spending is subject to political cycles and policy changes that can affect funding priorities and market opportunities. Changes in administration or shifts in geopolitical focus can impact specific programs or technology areas, affecting company performance and investment returns.

Mitigation strategies include diversifying across multiple technology areas and customer segments, focusing on companies with broad applicability across different defense requirements, and maintaining awareness of political and policy developments that could affect the sector.

Technology and Execution Risks

Defense technologies often involve complex technical challenges with uncertain development timelines and costs. Companies may face difficulties in scaling their technologies or meeting performance requirements, leading to program delays or cancellations.

Mitigation strategies include thorough technical due diligence, focusing on companies with proven development capabilities and experienced management teams, and maintaining realistic expectations about development timelines and costs.

Market Access and Customer Concentration Risks

Success in defense markets often requires establishing relationships with government customers and obtaining necessary security clearances and certifications. Companies may face challenges in accessing customers or may become overly dependent on specific programs or customers.

Mitigation strategies include focusing on companies with diversified customer bases, strong government relationships, and clear paths to expanding their customer reach. Supporting companies in developing the capabilities necessary to serve multiple customers and markets can also reduce concentration risk.

Suggested Investment Strategies

Successful defense tech investing requires strategies that account for the unique characteristics of the sector while leveraging the opportunities it presents. Different investment approaches may be appropriate depending on investor objectives, risk tolerance, and investment horizon.

Dual-Use First Strategy

Prioritizing companies with dual-use technologies that can serve both commercial and defense markets provides several advantages. These companies typically have larger total addressable markets, reduced customer concentration risk, and multiple paths to value creation. The commercial market validation can also provide confidence in the underlying technology and business model.

Companies like Palantir have demonstrated the effectiveness of this approach, using defense contracts to fund development while expanding into commercial markets. This strategy requires identifying technologies with clear commercial applications and management teams capable of executing across multiple markets.

B2G vs B2B2G Approach

Investors must decide whether to focus on companies that sell directly to government customers (B2G) or those that work through traditional defense contractors (B2B2G). Each approach has distinct advantages and risks that must be carefully evaluated.

Direct government sales (B2G) can provide higher margins and stronger customer relationships but require significant investment in government relations capabilities and security clearances. Working through traditional contractors (B2B2G) can provide faster market access and reduced regulatory burden but may limit margins and customer relationships.

A balanced approach that includes companies pursuing both strategies can provide portfolio diversification while capturing the advantages of each approach.

Regional Focus Considerations

Geographic focus can provide advantages in terms of market knowledge, regulatory understanding, and network effects. However, the global nature of defense markets and the increasing importance of allied cooperation suggest that a purely domestic focus may limit opportunities.

U.S.-focused strategies benefit from the largest defense market and most developed venture capital ecosystem but face increasing competition and potentially higher valuations. European strategies can access growing markets with less competition but may face regulatory complexity and smaller market sizes.

A global approach that includes companies from multiple regions can provide diversification benefits while accessing the best opportunities regardless of location.

Lessons from Previous Defense Innovation Cycles

Historical analysis of defense innovation cycles provides valuable insights for current investors. Previous cycles have demonstrated both the potential for substantial returns and the risks associated with defense tech investing.

Cold War Innovation Lessons

The Cold War period saw substantial government investment in defense technologies that later found commercial applications, including the internet, GPS, and various semiconductor technologies. Companies that successfully transitioned these technologies to commercial markets generated substantial returns for investors.

The lesson for current investors is the importance of identifying technologies with broad applicability beyond their initial defense applications. Companies that can leverage defense funding to develop technologies with commercial potential are positioned to generate superior returns.

Post-Cold War Consolidation

The end of the Cold War led to substantial consolidation in the defense industry as reduced spending forced companies to merge or exit the market. This period demonstrated the importance of scale and diversification for surviving market downturns.

Current investors should focus on companies with sustainable competitive advantages and diversified revenue streams that can weather potential changes in defense spending priorities.

9/11 and Homeland Security Boom

The September 11 attacks created new market opportunities in homeland security and counterterrorism technologies. Companies that could quickly adapt their technologies to address these new requirements generated substantial returns.

This cycle demonstrates the importance of agility and adaptability in defense tech companies. Investors should focus on companies with flexible platforms that can be adapted to address evolving threats and requirements.

Portfolio Construction and Risk Management

Constructing a successful defense tech portfolio requires balancing exposure across different technology areas, company stages, and risk profiles. Diversification across these dimensions can help manage risk while capturing upside from the sector's growth.

Technology Area Diversification

Spreading investments across different technology areas reduces the risk of being overly exposed to specific technical or market risks. A balanced portfolio might include companies developing AI and autonomous systems, cybersecurity solutions, space technologies, and advanced materials.

Each technology area has different risk-return profiles and development timelines, providing natural diversification benefits. Maintaining exposure to both emerging technologies and more mature areas can balance growth potential with stability.

Stage Diversification

Including companies at different development stages provides exposure to different risk-return profiles. Early-stage companies offer higher potential returns but greater execution risk, while later-stage companies provide more stability but potentially lower returns.

A balanced approach might include a mix of seed and Series A companies for high-growth potential, Series B and C companies for balanced risk-return, and later-stage companies for stability and near-term liquidity opportunities.

Geographic and Customer Diversification

Including companies serving different geographic markets and customer segments can reduce concentration risk and provide exposure to different growth drivers. This might include U.S. companies serving the Department of Defense, European companies addressing NATO requirements, and companies serving allied nations' defense needs.

Customer diversification within the defense market can also provide risk management benefits, reducing exposure to specific program cancellations or budget cuts.

Conclusion

The defense technology sector presents a compelling investment opportunity driven by geopolitical tensions, technological innovation, and structural changes in defense procurement. The sector's demonstrated resilience, substantial market size, and strategic importance provide a foundation for sustained growth and attractive returns.

Successful investing in defense tech requires understanding the unique characteristics of the sector, including regulatory requirements, customer dynamics, and technology development cycles. Investors who develop expertise in these areas and construct appropriately diversified portfolios are positioned to generate substantial returns while supporting critical national security objectives.

The current environment, characterized by strong fundamentals, reasonable valuations, and clear growth catalysts, provides an attractive entry point for investors seeking exposure to this strategic sector. The emergence of successful companies like Anduril and Palantir has validated the investment thesis and created a roadmap for future success.

References

[1] McKinsey & Company. "Creating a modernized defense technology frontier." February 12, 2025. https://www.mckinsey.com/industries/aerospace-and-defense/our-insights/creating-a-modernized-defense-technology-frontier

[2] Bessemer Venture Partners. "Roadmap: Defense Tech." January 28, 2024. https://www.bvp.com/atlas/roadmap-defense-tech

[3] Sifted. "How Ukraine changed defence tech." https://sifted.eu/articles/how-ukraine-changed-defence-tech

[4] Center for Strategic and International Studies. "A Strategic Approach to Defense Investment." March 26, 2018. https://www.csis.org/analysis/strategic-approach-defense-investment

[5] Forbes. "Defense Tech Boom: Autonomous Drones, Lasers, And Hypersonic Missiles." June 9, 2025. https://www.forbes.com/sites/garthfriesen/2025/06/09/defense-tech-boom-autonomous-drones-lasers-and-hypersonic-missiles/

[6] Bessemer Venture Partners. "Roadmap: Defense Tech." January 28, 2024. https://www.bvp.com/atlas/roadmap-defense-tech

[7] Forbes. "Defense Tech Boom: Autonomous Drones, Lasers, And Hypersonic Missiles." June 9, 2025. https://www.forbes.com/sites/garthfriesen/2025/06/09/defense-tech-boom-autonomous-drones-lasers-and-hypersonic-missiles/

[8] Forbes. "Defense Tech Boom: Autonomous Drones, Lasers, And Hypersonic Missiles." June 9, 2025. https://www.forbes.com/sites/garthfriesen/2025/06/09/defense-tech-boom-autonomous-drones-lasers-and-hypersonic-missiles/

[9] Bessemer Venture Partners. "Roadmap: Defense Tech." January 28, 2024. https://www.bvp.com/atlas/roadmap-defense-tech

[10] Palantir Technologies. "Q4 2024 Business Update." https://investors.palantir.com/news-details/2025/Palantir-Reports-Fourth-Quarter-and-Full-Year-2024-Financial-Results/default.aspx

[11] Bessemer Venture Partners. "Roadmap: Defense Tech." January 28, 2024. https://www.bvp.com/atlas/roadmap-defense-tech

[12] TechCrunch. "Anduril raises $2.5B at $30.5B valuation led by Founders Fund." June 5, 2025. https://techcrunch.com/2025/06/05/anduril-raises-2-5b-at-30-5b-valuation-led-by-founders-fund/

[13] Forbes. "Defense Tech Boom: Autonomous Drones, Lasers, And Hypersonic Missiles." June 9, 2025. https://www.forbes.com/sites/garthfriesen/2025/06/09/defense-tech-boom-autonomous-drones-lasers-and-hypersonic-missiles/

[14] CNBC. "Anduril's Palmer Luckey says the company will 'definitely' go public." June 10, 2025. https://www.cnbc.com/2025/06/10/anduril-palmer-luckey-ipo.html

[15] Palantir Technologies. "Q4 2024 Business Update." https://investors.palantir.com/news-details/2025/Palantir-Reports-Fourth-Quarter-and-Full-Year-2024-Financial-Results/default.aspx

[16] TechCrunch. "Defence AI startup Helsing raises $487M Series C, plans Baltic expansion to combat Russian threat." July 11, 2024. https://techcrunch.com/2024/07/11/defence-ai-startup-helsing-raises-487m-series-c-plans-baltic-expansion-to-combat-russian-threat/

[17] Forbes. "Defense Tech Boom: Autonomous Drones, Lasers, And Hypersonic Missiles." June 9, 2025. https://www.forbes.com/sites/garthfriesen/2025/06/09/defense-tech-boom-autonomous-drones-lasers-and-hypersonic-missiles/

[18] Shield Capital. Company website. https://shieldcap.com/

[19] TechCrunch. "Anduril raises $2.5B at $30.5B valuation led by Founders Fund." June 5, 2025. https://techcrunch.com/2025/06/05/anduril-raises-2-5b-at-30-5b-valuation-led-by-founders-fund/

[20] TechCrunch. "Defence AI startup Helsing raises $487M Series C, plans Baltic expansion to combat Russian threat." July 11, 2024. https://techcrunch.com/2024/07/11/defence-ai-startup-helsing-raises-487m-series-c-plans-baltic-expansion-to-combat-russian-threat/

[21] PitchBook. "2024 Vertical Snapshot: Defense Tech Update." July 5, 2024. https://pitchbook.com/news/reports/2024-vertical-snapshot-defense-tech-update

[22] JPMorgan. "Defense Tech Innovation and the Role of Startups." September 20, 2024. https://www.jpmorgan.com/insights/investing/investment-trends/defense-tech-innovation-and-the-role-of-startups

[23] TechCrunch. "Anduril raises $2.5B at $30.5B valuation led by Founders Fund." June 5, 2025. https://techcrunch.com/2025/06/05/anduril-raises-2-5b-at-30-5b-valuation-led-by-founders-fund/

[24] TechCrunch. "Defence AI startup Helsing raises $487M Series C, plans Baltic expansion to combat Russian threat." July 11, 2024. https://techcrunch.com/2024/07/11/defence-ai-startup-helsing-raises-487m-series-c-plans-baltic-expansion-to-combat-russian-threat/

[25] PitchBook. "2024 Vertical Snapshot: Defense Tech Update." July 5, 2024. https://pitchbook.com/news/reports/2024-vertical-snapshot-defense-tech-update

[26] Reuters. "Defense and space tech firm Voyager reveals annual revenue in IPO filing." May 16, 2025. https://www.reuters.com/markets/deals/defense-space-tech-firm-voyager-technologies-files-us-ipo-2025-05-16/

[27] CNBC. "Anduril's Palmer Luckey says the company will 'definitely' go public." June 10, 2025. https://www.cnbc.com/2025/06/10/anduril-palmer-luckey-ipo.html

[28] Bessemer Venture Partners. "Roadmap: Defense Tech." January 28, 2024. https://www.bvp.com/atlas/roadmap-defense-tech

[29] Forbes. "Defense Tech Boom: Autonomous Drones, Lasers, And Hypersonic Missiles." June 9, 2025. https://www.forbes.com/sites/garthfriesen/2025/06/09/defense-tech-boom-autonomous-drones-lasers-and-hypersonic-missiles/

[30] Forbes. "Defense Tech Boom: Autonomous Drones, Lasers, And Hypersonic Missiles." June 9, 2025. https://www.forbes.com/sites/garthfriesen/2025/06/09/defense-tech-boom-autonomous-drones-lasers-and-hypersonic-missiles/

[31] Forbes. "Defense Tech Boom: Autonomous Drones, Lasers, And Hypersonic Missiles." June 9, 2025. https://www.forbes.com/sites/garthfriesen/2025/06/09/defense-tech-boom-autonomous-drones-lasers-and-hypersonic-missiles/

[32] U.S. Department of Defense. "How the Mind-Tech Nexus will Win Future Wars." April 18, 2025. https://media.defense.gov/2025/Apr/18/2003694020/-1/-1/1/B-188 HMW FINAL 4.8.25 - WITH 508 CHECK.PDF

[33] Forbes. "Defense Tech Boom: Autonomous Drones, Lasers, And Hypersonic Missiles." June 9, 2025. https://www.forbes.com/sites/garthfriesen/2025/06/09/defense-tech-boom-autonomous-drones-lasers-and-hypersonic-missiles/

[34] Forbes. "Defense Tech Boom: Autonomous Drones, Lasers, And Hypersonic Missiles." June 9, 2025. https://www.forbes.com/sites/garthfriesen/2025/06/09/defense-tech-boom-autonomous-drones-lasers-and-hypersonic-missiles/

[35] Forbes. "Defense Tech Boom: Autonomous Drones, Lasers, And Hypersonic Missiles." June 9, 2025. https://www.forbes.com/sites/garthfriesen/2025/06/09/defense-tech-boom-autonomous-drones-lasers-and-hypersonic-missiles/

[36] Forbes. "Defense Tech Boom: Autonomous Drones, Lasers, And Hypersonic Missiles." June 9, 2025. https://www.forbes.com/sites/garthfriesen/2025/06/09/defense-tech-boom-autonomous-drones-lasers-and-hypersonic-missiles/

[37] Forbes. "Defense Tech Boom: Autonomous Drones, Lasers, And Hypersonic Missiles." June 9, 2025. https://www.forbes.com/sites/garthfriesen/2025/06/09/defense-tech-boom-autonomous-drones-lasers-and-hypersonic-missiles/

[38] Bessemer Venture Partners. "Roadmap: Defense Tech." January 28, 2024. https://www.bvp.com/atlas/roadmap-defense-tech

[39] Forbes. "Defense Tech Boom: Autonomous Drones, Lasers, And Hypersonic Missiles." June 9, 2025. https://www.forbes.com/sites/garthfriesen/2025/06/09/defense-tech-boom-autonomous-drones-lasers-and-hypersonic-missiles/

[40] Bessemer Venture Partners. "Roadmap: Defense Tech." January 28, 2024. https://www.bvp.com/atlas/roadmap-defense-tech

[41] Bessemer Venture Partners. "Roadmap: Defense Tech." January 28, 2024. https://www.bvp.com/atlas/roadmap-defense-tech

[42] Forbes. "Defense Tech Boom: Autonomous Drones, Lasers, And Hypersonic Missiles." June 9, 2025. https://www.forbes.com/sites/garthfriesen/2025/06/09/defense-tech-boom-autonomous-drones-lasers-and-hypersonic-missiles/

[43] U.S. Department of Defense. "How the Mind-Tech Nexus will Win Future Wars." April 18, 2025. https://media.defense.gov/2025/Apr/18/2003694020/-1/-1/1/B-188 HMW FINAL 4.8.25 - WITH 508 CHECK.PDF

[44] PitchBook. "Defense VCs firm up investment priorities with $1T budget." May 2, 2025. https://pitchbook.com/news/articles/defense-startups-vc-dod-budget-priorities-dual-use

This report was prepared by Bogdan Cristei and Manus AI based on comprehensive research and analysis of publicly available sources. The information contained herein is for informational purposes only and should not be construed as investment advice. Investors should conduct their own due diligence and consult with qualified professionals before making investment decisions.

Slides: