Space to Watch: Construction Tech

Written by Bogdan Cristei of Shack15 Ventures and Tim Yang of Tyche Partners.

Written by Bogdan Cristei of Shack15 Ventures and Tim Yang of Tyche Partners.

Summary:

For an industry with $10 trillion in annual revenue, or about 13% of global GDP, it can be hard to believe that it is one of the least digitized. Labor shortages, building information modeling, advances in machine vision, robotics and AI/ML are all driving up automation adoption in construction.

There are many companies in the space; some, like PlanGrid, killed it — they targeted low-hanging fruit such as digital plan sharing and got acquired by Autodesk for $875M. Others, like Katerra, burned through $3B before flaming out. Entrepreneurs are testing ideas, getting a feel for what works and what doesn’t, and learning from mistakes that have been made.

Modular and prefab approaches are gaining traction, and the construction robotics category is becoming more relevant. Highly fragmented end markets and value chains remain an important issue; enabling technologies that apply across multiple verticals such as teleoperation, microlocation or haptic feedback could make more attractive investments versus one-off solutions.

At the Seed and Pre-Seed stages it is unclear where investors should play to find a winner — the space is inherently risky with limited upside, and there are many look-a-like approaches.

This article is fairly long, please use the table of contents below to go over sections of interest. Feel free to let us know if we made any errors or omitted important information.

Table of Contents:

- Overview

Uncontrolled Environment

Financial Constraints

Lack of R&D

Coordination Issues - Industry Status

- Trends Shaping Construction

- Investment Trends

Funding Raised by Construction Startups ($M)

Construction Startup Funding as a Share of Total VC Funding

Number of Construction Startups Founded

Where is the Funding Going?

Breakdown of Investments by Category - Prefab & Modular Deep Dive

Pros

Cons

Residential

Commercial

Total Addressable Market

Penetration Poised to Improve due to New Regulations

Implications of New Regulations

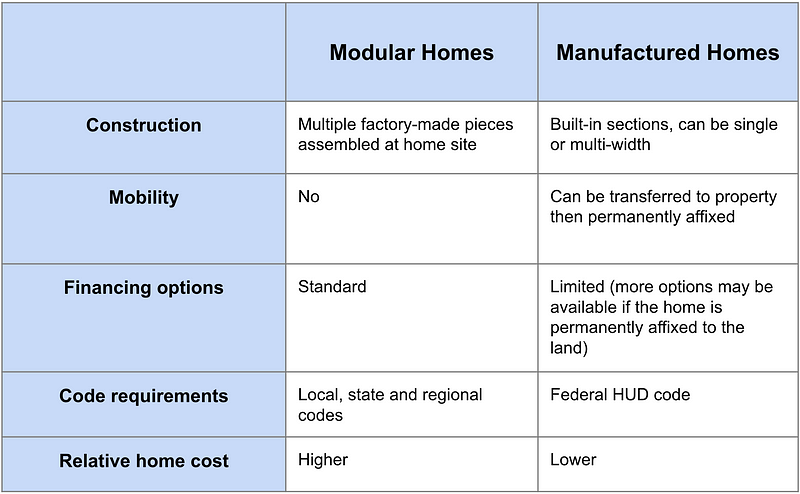

Difference between Modular Homes vs. Manufactured Homes

Permanent Modular Construction Taking off in North America

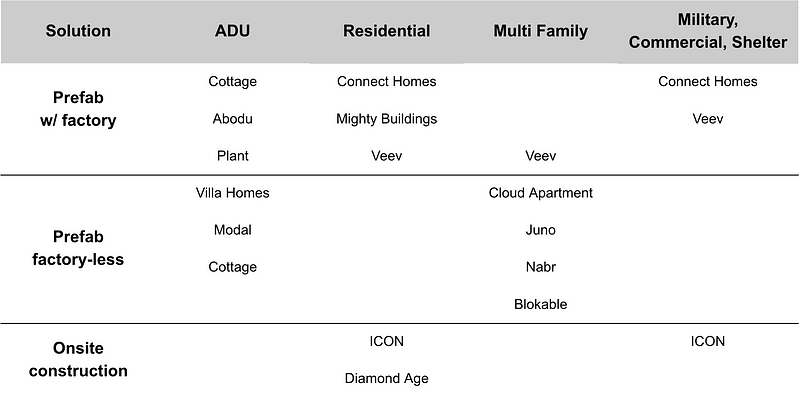

Sub-sectors Require Different Solutions

Custom Solutions Within Key Verticals

Prefab/Modular Companies - Construction Robotics Deep Dive

Overview

Challenges

Opportunities in “Enabling Technologies”

Top Construction Contractors

Construction Robotics Framework

Applying the Framework

Robotics Evaluation Framework by CAComputational Design in AEC

Examples of Companies Working on Enabling Technologies

Examples of Construction Robotics Companies

Others Worth Mentioning - Areas of Improvement for the Construction Tech Industry

- Conclusion

- Appendix

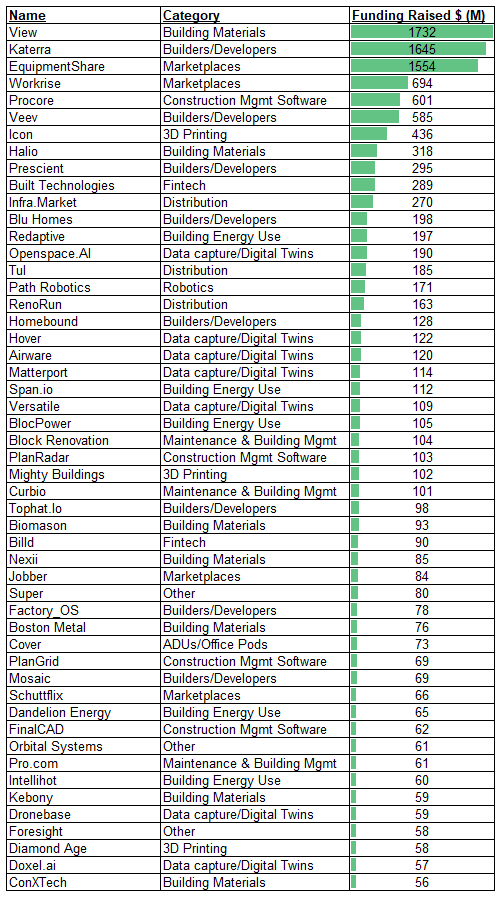

Top 50 construction startups by total funding received [9]

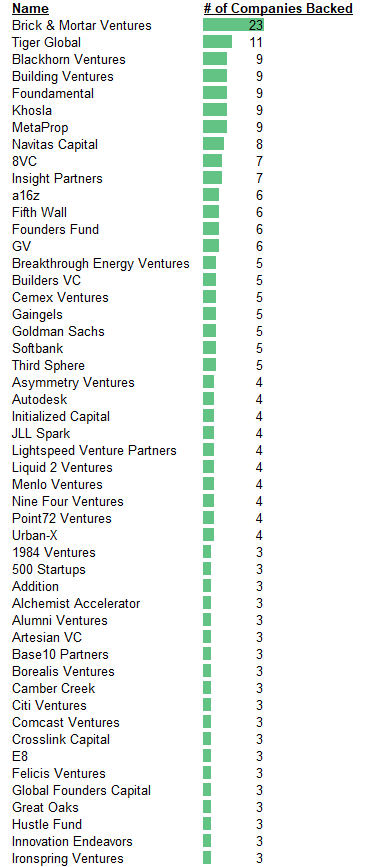

Top 50 VC funds by number of construction startups they’ve backed [9]

Top PropTech Focused VC Funds - References

Prefab & Modular Research

Robotics Research

1. Overview

For an industry with $10 trillion in annual revenue [1], or about 13% of global GDP [7], it can be hard to believe that it is one of the least digitized — only better than agriculture [2]. Why is this the case? Below is an incomplete list of gotchas, but helpful to get the conversation started:

Uncontrolled Environment

- Dynamic worksites — construction worksites are the poster child for “unstructured environments”

- Uncontrolled deployment environments — off-road navigation, irregular terrain, weather conditions

- Dust and dirt — can obscure sensors and damage componentry

- Safety and damage — very heavy equipment moving around can lead to accidents such as “struck-by incidents” — the most common in the industry

Financial Constraints

- Costs and profits — low margins; reports show that GCs make a pre-tax profit of 1% to 2%

- Conservative industry & famously stubborn in its adoption of new technology

- Often no cash flow available to invest in the newest technology — many companies rely on used equipment, typically much cheaper [3] than new equipment while being just about as reliable

- Velocity of cash — capital is tied up for long periods of time; there is a limit to how quickly capital can be turned into new projects — this limits scale and profitability

- Lack of traditional data such as estimates and reviews [4]

Lack of R&D

- Construction general contractors (GSs) usually don’t have research and development (R&D) departments

- Technology implementation is very hard since there are is no R&D for mass production or mass implementation

- Initial customer rollout is critical for scale up

- Slower scaling than in other industries

- Abundant green field for new technologies

Coordination Issues

- Coordinating information between HVAC, plumbing, robotic solutions or scripts for digitalization is not straightforward

- Different trades are also treated differently — there is a pecking order. Carpenters are usually cheaper and widely available; electricians and plumbers tend to be more expensive. Tools are also allocated and funded differently — some trades can expect to have tools provided onsite while others have to bring their own

- Process change — certainty of the scope of work may change when introducing digital or robotic solutions

- Introducing new organizations into the fold that reduce the worker’s scope is difficult

- Training new operators in construction is difficult; training existing operators to perform actions in a different way vs. what they have been used to for the past 10+ years is also difficult

- Workers generally have lower level of tech-focused education

2. Industry Status

Labor shortages (41 percent of the current US construction workforce is expected to retire by 2031), building information modeling (BIM), advances in machine vision, robotics and AI/ML are all driving up automation adoption in construction.

There are many companies in the space. Some, like PlanGrid, killed it — they targeted low-hanging fruit like digital plan sharing and got acquired by Autodesk for $875M. Others, like Katerra, burned through $3B before flaming out; they were working on many things at the same time, and potentially over-complicated the issues at hand, including spending tens of millions of dollars on an ERP system. Some had false starts, some are struggling to raise follow-on rounds due to poor progress, a few are breaking out, and others are just getting started.

Our view is that entrepreneurs had an opportunity to test their ideas, got a feel for what works and what doesn’t, they are learning from each other, and most importantly they are learning from mistakes that have been made thus far. Now is the time to keep an eye on the space as the first winners are starting to emerge, and viable early-stage companies are being formed. We expect to see a high degree of consolidation in the sector, with a limited number of runaway winners.

3. Trends Shaping Construction

- Digital transformation is encouraged by advancements in high definition surveying, geolocation and building information modeling

- Light asset models and easy deployments promised by digital collaboration and mobility tools resulted in high amounts of venture capital funding, especially by new and existing prop-tech funds (more details below)

- Construction IoT and future-proofing are close to an inflection point [5]

4. Investment Trends

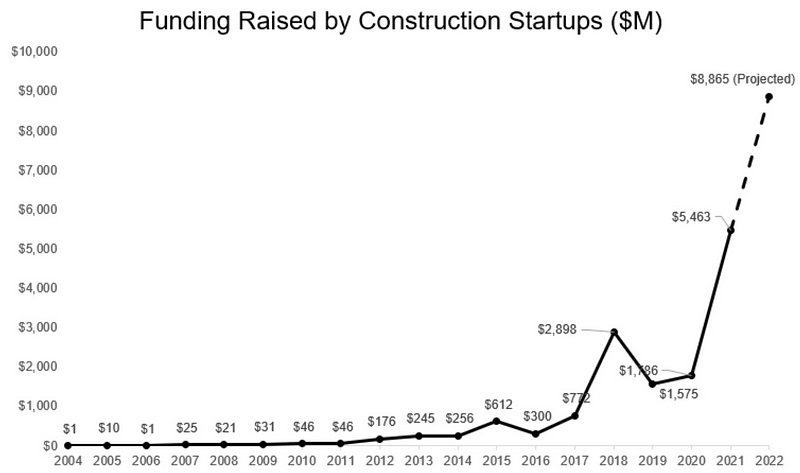

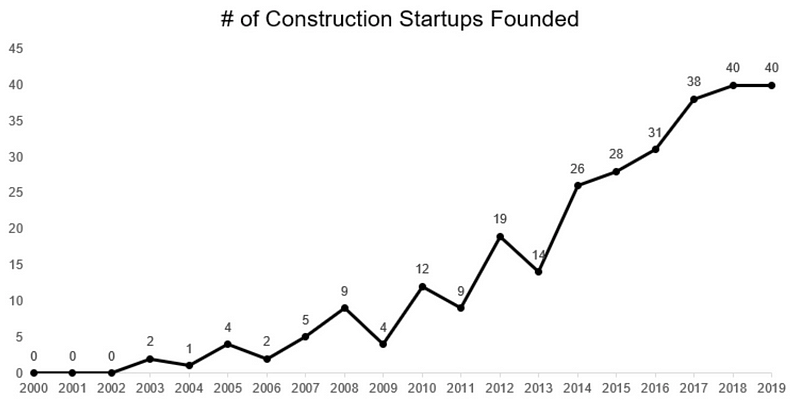

Construction startups raised over $5 billion in 2021, up from under $0.1 billion in 2011. The industry is on track to raise close to $9 billion in 2022 [9]

Funding Raised by Construction Startups ($M)

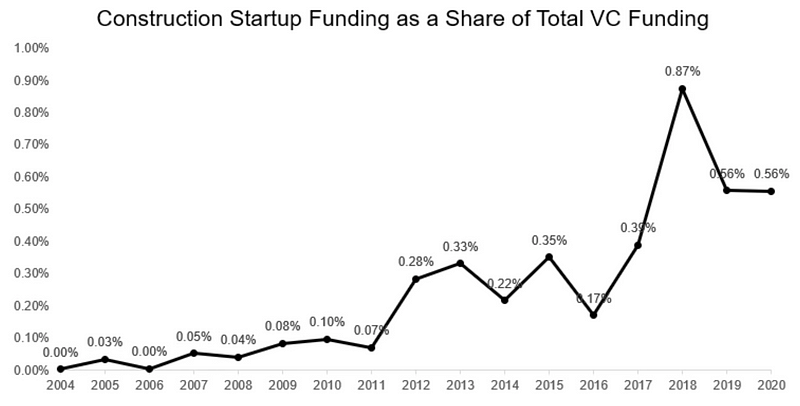

Construction Startup Funding as a Share of Total VC Funding

Construction startup funding is a larger and larger fraction of total venture capital invested

Number of Construction Startups Founded

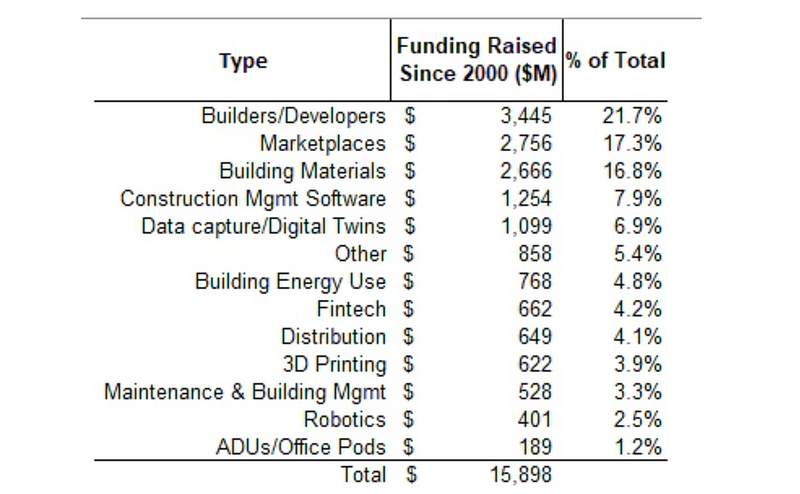

Where is the Funding Going?

The funding is going to 12 primary categories (see Construction Physics | A Brief History of Construction Startups)

- Builders/Developers (eg Veev, Blokable, Prescient)

- Building Materials (eg View, Carbicrete, Electrasteel)

- ADUs/Office Pods (eg Cover, Adobu, Boxabl)

- Energy Use and Management (eg Redaptive, Dandelion Energy, Domatic)

- Marketplaces (eg Equipmentshare, Amast, BuildZoom)

- Distribution and Logistics (eg RenoRun, Tul, Infra.Market)

- Construction Management Software (eg Procore, Fieldwire, RedTeam)

- Robotics.(eg Dusty, Canvas, Toggle)

- 3D Printing (eg Icon, Mighty Buildings, Branch Technology)

- Fintech (eg Built Technologies, Rigor.build, Levelset)

- Datacapture and Digital Twins (eg OpenSpace.AI, Doxel.AI, Versatile)

- Renovation/Repair/Maintenance (eg Humming Homes, Block Renovation, Made Renovation)

- Other (eg UpCodes, Toric, Shepherd)

Breakdown of Investments by Category

5. Prefab & Modular Deep Dive

Definitions: “Modular construction involves producing standardized components of a structure in an offsite factory, then assembling them onsite. Terms such as offsite construction, prefabrication, and modular construction are used interchangeably and cover a range of different approaches and systems” [5]

Pros

- Faster construction — foundation and walls can be built in a couple of days versus weeks or even months with traditional framing

- Trades like electrical, plumbing, heating or roofing can be more easily integrated in the structural design phase of a project

- Less bodies needed for classical labor such as carpenters, plumbing, HVAC

- Reduced waste and hypothetically reduced costs

Cons

- New challenges in logistics, shipping and maintenance; difficult to ship oversized containers, and expensive to “ship air” — structures that are not fully collapsable

- Increased need of highly specialized people that are hard to find and train

- Regulations for safety and inspections are not caught up and up to date with new technologies (eg concrete structures need to be reinforced)

- Difficult to get approval for permits and maintain them

- In the case of 3D printing (eg ICON, Mighty Buildings) new elements can add components and increase costs

- In some cases post processing is needed which can get expensive quickly

Residential

The majority of prefab companies started with the ADU market as a beachhead; however, as they began taking down-payments and deploying projects they realized they can’t scale as fast as planned due to two main reasons: permitting and customization. The permitting process was more involved and took longer than expected. After the first five or so projects deployed, they also realized they are customizing the units more than planned due to unexpected terrain, piping or electric limitations and logistics expenses and delays. For these reasons, working with developers became a more desirable path. For example Mighty Buildings, Veev and Bone Structure all started in the ADU market, then pivoted away to working with developers instead; currently, prefab companies have ADU offerings but none of them highlight it as a major revenue contribution.

Commercial

The commercial approach makes sense mostly for low height buildings, shelters (eg displaced refugees) or temporary housing. It is hard to envision scalability and factors that could drive a massive rollout. Additionally, margins are likely to be on the lower side due to limited premium elements and very little customization.

Total Addressable Market

Generally we observe a large TAM and low penetration

Combined U.S. and Europe prefab TAM

U.S. TAM

- Single family — $15bn

- Multi family — $20bn

- ADUs — $4bn (20k units annually at $200k ASP)

*assuming US and Europe split evenly

Low Penetration in the U.S.

Prefab penetration remains low in the U.S. due to an unfavorable regulatory environment, high lumber and labor costs, and supply chain inefficiencies.

For more details regarding roles of HUD and NAHB on housing in general, see this article from the Federal Reserve Bank of Minneapolis.

Penetration Is Poised to Improve Due To New Regulations

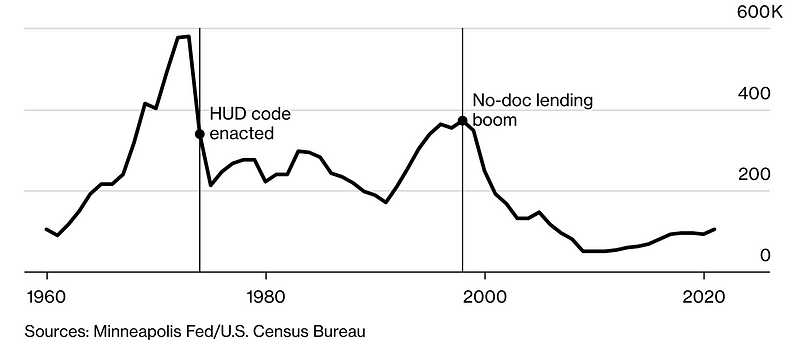

Regulation was a key driver for manufactured homes losing shares to stick-built homes back in 1974.

“At their peak, manufactured homes accounted for 60% of new single-family houses in the U.S; Congress passed a law in 1974 that required the U.S. Department of Housing and Urban Development to come up with a national code for manufactured homes. This national HUD code didn’t work out in the manufacturers’ favor. “ [6]

The current regulatory backdrop could materially improve driven by new government initiatives in 2021, which aim to loosen building code and increase financing options for prefab homes. (For more details regarding roles of HUD and NAHB on housing in general see this article).

Implications of New Regulations

- Industry experts are cautiously optimistic about the overall impact as it has not gotten through congress yet.

- The policy targets to increase supply and demand on low end homes (eg mobile homes and ADUs) rather than high end modular homes (eg Mighty Buildings)

- The Biden administration hopes to see 1 million ADUs in the next five years

- If the new regulation is implemented, mobile homes would look more like regular homes.

- To our knowledge, Villa Homes (more information below) is the only ADU vendor that uses HUD-compliant mobile home capacity to build ADUs. Villa’s key value proposition is that fast ramping can provide stable utilization rates for factories, increasing their bottom line. HUD compliant ADUs should also come with quality guarantees.

Modular Homes vs. Manufactured Homes

There are three scaled manufacturers: Skyline Champion, Cavco, and Clayton. Together they make over 100,000 homes per year. These manufacturers are jointly liable for the home.

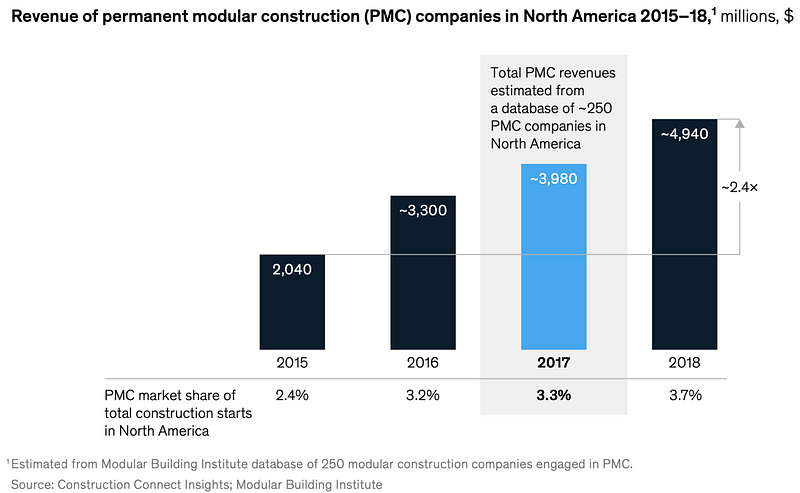

Permanent Modular Construction Taking off in North America

A value chain delivering approximately $11 trillion of global value added and $1.5 trillion of global profit pools looks set for overhaul. There are emerging indications that permanent modular construction is taking off in North America. A $265 billion annual profit pool awaits disrupters [7]

North America 2015–2018 Revenues of Permanent Modular Construction

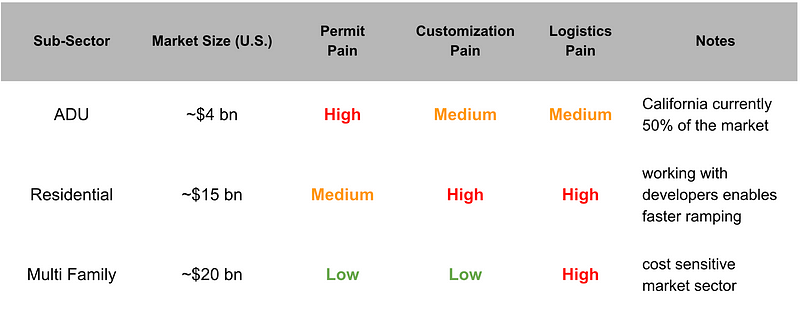

Prefab Key Sub-Sectors & Pain Points

Sub-sectors Require Different Solutions

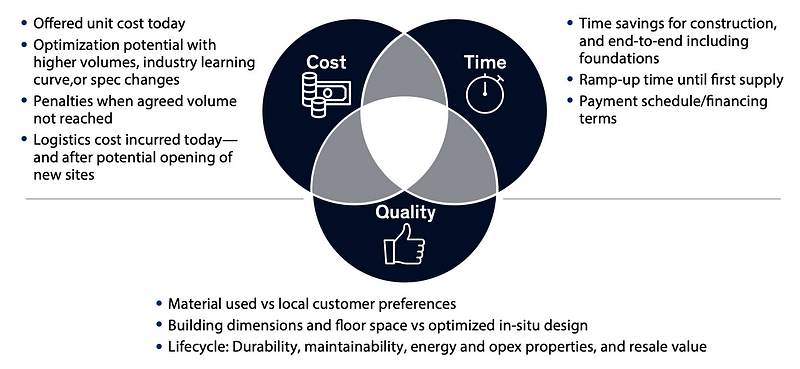

Another key takeaway that we are noticing is the “productization” of the building process given specific levers and limitations. Value creation in the space requires trade-offs between various factors, some of them shown below.

Custom Solutions Within Key Verticals

Prefab & Modular Companies

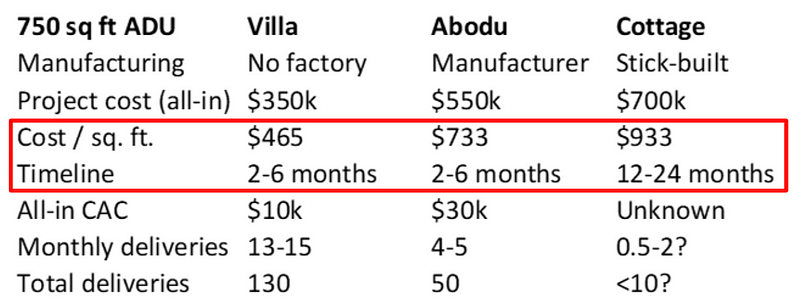

Villa Homes

Factoryless direct to customer platform for ADUs in high property value areas

Backround

- Factoryless, direct to customer, custom ADUs, builder included on website

- Focused on geographies with high property values

- Largest ADU customer of Skyline Champion (one of the top 3 prefab manufacturers)

- Claims to be 2 year ahead of competition in builder relationship and customer traction

- Raised $20M to date; Atomic is largest investor to date. Possibly raising seed extension or Series A

- They claim they are the only provider that uses manufacturers that build to HUD code. Federal standards for ADUs and multifamily developments.

Positives

- Large customer base translates into more detailed cost breakdown for better customer experience

- Good traction among pre-fab — 100+ units delivered since Nov. 2020

- Improved cost and time savings vs. competitors

Negatives

- Platform play with limited technology and barriers of entry

- The ADU market may not be big enough for an IPO

Current Fundraise

- Seed Extension / Series A

- Raised $20M to date

Mighty Buildings

Background

- Automated manufacturing process

- Materials can be shipped in containers — claiming 2 truck loads per full house

- Delivered ~15 ADUs before pivoting to single-family-homes and working with developers

- Similar to others that started in the ADU market, they backed out of ADUs due to complications with permitting and site customization, preferring to work with developers

- Currently working with a mid size developer to build first 3D printed community in Palm Spring

- $150m binding orders

- Currently raising Series C round to build additional capacity

Positives

- 3D printed materials enable architecturally distinct residential homes

- High barriers of entry — proprietary 3D printing technology (UV DLP)

- Claim to reduce onsite construction time by >50%

- Proprietary polymer composite tech

- Lighter & better performing thermal insulation

Negatives

- Pivoted from ADUs to SFH due to market constraints

- Business needs microfactories ($10m each) for regional expansion

Fundraising

- Currently raising Series C

- $100m raised to date

ICON

Background

- On-site 3D printing robots that extrude concrete materials to form structures. The company has large contracts with military, traction with residential buildings as well as with NASA

- The 3D printed structures are starting to look better; they solved the issue of making the walls appear square instead of rounded; cannot tell if the home is 3D printed any longer, unless that is the desired design by user or owner

Positives

- Strong traction with Lennar for a 100 homes community

- Good amount of intellectual property around 3D printing & robotics; hard to copy

- They have material contracts with armed forces and defense, proving they can build very quickly and on the go

- Strong traction with military and NASA

- The company has a good profile for an IPO, including a project with NASA for 3D printing structures on the Moon

Negatives

- Uncontrolled environment with on-site manufacturing still remains an issue

Financials

- Not raising currently

- Raised $392 million of Series B venture funding in a deal led by Tiger Global Management and Norwest Venture Partners on February 18, 2022

- $2bn valuation from last round (Feb 2022)

Cloud Apartments

- Focused on “productized construction “— pre-designed + pre-approved apartment buildings; modular for easy installation; paired with software to rapidly design

- They are using Autovol.com as a partner (competitor to Factory OS, but using more robotics)

- Their version of modular = “snap connections” on site

- Currently raising a Seed round

- Very early still

Modal

- Structured to operate as a Toll Brothers type business, but focused more on customer experience; tech around streamlined process management, portal, builder for their units, financing and layered services

- Their aim is to create a brand (think Marriott)

- On the financing end, they want to become the construction lender of the future. Claims there are no great construction lending products out there yet, and they would like to approach this from a fintech angle

- Currently raising a Seed round

- Very early still

Layer Construction

- 3D printing software and hardware

- Team includes PhDs from Stanford, Princeton, Berkeley National Lab & Cambridge

- Can print dynamically from sides, not just gravity / brick laying type printing

- Machine vision algorithm for real-time monitoring; identifies defects like deformation, concrete missing + classifies different types of detects at 1m accuracy

- 20–100 pounds for robot

- Testing now in Europe

- Raising a Seed round

- Very early still

Others Worth Mentioning

- Haus.me

Developer of an autonomous mobile house intended to design and build homes that fit the future. The company’s offerings include intelligent homes, self-sustainable in cold or hot climates, - Modulart

Provider of housing construction services intended to build turnkey houses. The company’s services specializes in prefabricated reinforced concrete houses. - RAD Urban

Example of a modular supplier looking to generate 30 percent savings on high-rise buildings and 20–25 percent on mid-rise projects. The company aims to take 85–90 percent of onsite labor into the factory, where it estimates that labor is twice as productive as building in situ and with significant cost savings on hourly rates - Connect Homes

Pre-fab homes; 13 projects in LA and Bay Area; The single module shelter that the company has developed can be transported and put on site in one day. Based in Los Angeles, CA - Veev

Not the only company using a factory to make buildings, but with a uniquely integrated approach that pulls design, material supply chain, manufacturing, and construction in-house. - Autovol

Modular buildings take 25% to 50% less time to build than traditional methods, which means faster occupancy and return on investment, according to the MBI. Autovol claims to further reduce both time and costs because of their robots. - Also see: Factory OS, Bone Structure, Diamond Age (onsite 3D printing building construction) Branch (3D printed ventilated screen wall) ConnectHomes (prefab ADU), Bumblebee space(modualized furniture) Branch Technology, Apis Cor, AI SpaceFactory, Contour Crafting, Form Found Design, Roin

- Not “HardTech”— software, workflow, platforms for hiring contractors, risk management, payment tools, etc…

Agora (productivity tool for construction workers)

EquipmentShare — Asset tracking

Flexbase — receipt tracking

HqO — workplace engagement tool (property management)

Procore — construction management tool

Trade Hounds — tradepeople hiring marketplace

Placemakr (Whyhotel) — apartment short renting

Rhumbix — construction management tool

Buildingzoom — contractor marketplace

Fieldwire — jobsite management

Evercharge — charging solutions for apartment

Alice — construction planning tool

Helix — building document and measurement tool

Zerokey — spatial measurement tool for IIOT

Foresight — construction worker insurance

Levelset — payment tool for construction worker

Wingtra — mapping and surveying

Curbio — pre-listing staging app

Trade Hounds — tradepeople hiring marketplace

IFM — contractor hiring platform

Siteline — construction payment for contractors

Curri — distribution/logistic platform for construction materials

Handdii — contractor insurance platform

6. Construction Robotics Deep Dive

The category is hot and under-invested, with new entrants such as Raise Robotics (robotics for window facade installations) — new entrants are observing the gaps and need for robotics automation in construction, and they are taking action. One major pain point in addition to the ones already mentioned above, is a highly fragmented end market and value chain; more details on this below.

Overview

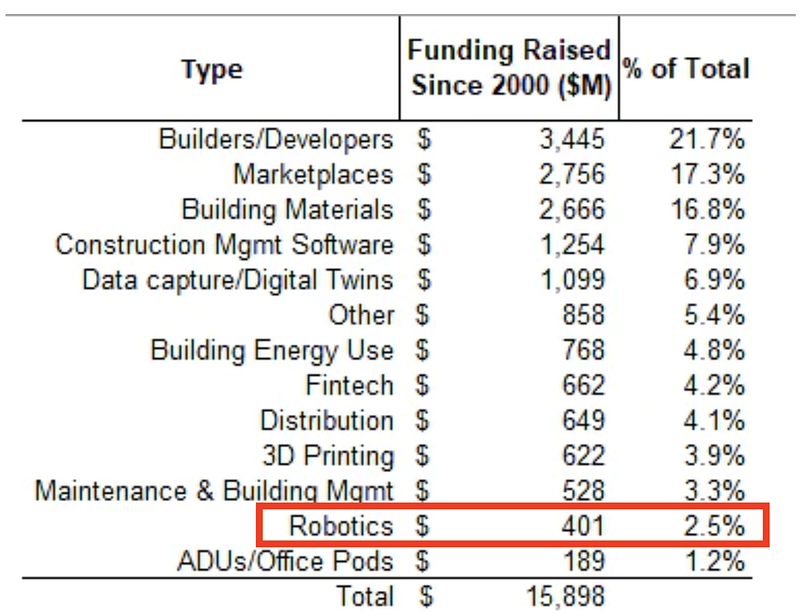

Currently investment in robotics construction as a category is fairly low. If we look at total funding raised per category since the year 2000, “Robotics” is low at 2.5% of total.

Challenges

Within the robotics construction space, investors and entrepreneurs need to think through the following items:

Safety

- Nobody buys a product that does not keep their workers as safe or safer than before deploying the product.

TAM

- Is the TAM large enough? How do we think about TAM?

- What is the total number of robots / units that the market can absorb ?

- Customer repeatability — is the process repeatable?

- Not quite the same as thinking of TAMs in other spaces

Technology Defensibility

- There are two patterns emerging with robotics projects in construction:

1) High barriers of entry but hard to use

2) Low barrier of entry but easy to deploy - Ideally, we’d want something that can be both easy to deploy with high barriers of entry

Speed of Growth

- The land and expand strategy needs to be very clear in construction. It shouldn’t be an area to take risk on, and the entrepreneur needs to have a clear view

- Growth in the space should not be viewed as triple triple double double double — it shouldn’t be thought of like software

- Growth is different — to the outside world, growth in construction feels slow, but there may be very interesting niches

ROI

- There are multiple ways to think of ROI as related to construction projects; mostly revolves around timeline and time savings — if a bill was shrunk by one week, that is a massive dollar amount equivalent; it is easy to understand that saved time = saved cost

- ROI in construction is often calculated project by project, and not in 12–18 months increments

Unions & Project Schedule

- Consider doing due diligence calls with unions — need to make sure they are comfortable with the particular robotic approach, otherwise they can slow down deployment

- As world goes into recession, it plays even more here

- Startups speaking with unions about how to best use the data coming out of projects is usually a good sign. Sometimes they refer to this as “getting really tight with unions” to bring them on early on

- Showing unions how to up-level them, how they can be even more efficient, better, safer, is a great approach.

- Sometimes a robotics approach touches multiple unions such as painters and carpenters in the case of Canvas

- How does the robotics solution fit with and within the other trades?

- What are the schedule implications — is it making the overall schedule schedule longer or shorter?

- How heavy is the robot, how many operators per robot or robots per operator are needed?

Deployment Depth — Deep vs Wide

- Shallow deployments usually do not work well

- If someone can go deep within a Turner, they can also do it within a Bechtel or Kiewit (more information below)

- 40 deployments at 40 customers is not as good as 40 deployments at 3 customers; need to be able to see how deep a company goes

- Usually “we are just testing it out using our test budget” type of conversations are not a strong indicator of success

Superintendent vs Enterprise

- The internal champion needs to have control over budget

- Trying to sell to folks like superintendents doesn’t usually work — the superintendent approves their own project, but cannot approve other projects

- Often it makes more sense to have an enterprise approach vs. selling to internal champions (more on this below)

The Construction Robotics Market is Highly Fragmented

The construction robotics market can be loosely divided into the following segments:

- Excavation

Process of moving things like earth, rock, etc. with heavy equipment - Foundation

Pouring concrete to distribute the weight of the structure over a large area - Scaffolding

Temporary platform used to elevate and support workers and materials - Bricklaying

Process of laying bricks, concrete or stone to construct the structure of a building - Framing

Fitting together of wood or steel pieces to give structure support - Drywall

Construction material used to wrap columns to conceal steel beam, create walls and ceilings - MEP

Mechanical, electrical and plumbing engineering (incl. HVAC & insulation) - Painting

Finishing items in any residential or commercial project - Drilling

Drilling rounded holes in concrete walls, floors, ceiling, and other structures - Glass

Cutting, installing, removing glass for the purpose of implementing windows, doors, etc. - Flooring

Installing the covering over a floor structure to provide a walkable surface - Roofing

Installation to any above-grade structures to provide weatherproof protection

Opportunities in “Enabling Technologies”

Given the highly fragmented market, designing a robot that captures only a sliver of the value chain could be tricky; the construction industry itself is large, however growth in the space is slow — it would be a safer bet to invest in an enabling technology that applies across multiple verticals such as teleoperation (eg Teleo), microlocation (eg Humatics ) or haptic feedback (eg Boréas Technologies)[2]

Top Construction Contractors

Engineering News Record has a yearly list of the top 400 construction contractors. If a robotics team is good at deploying within the top 20–40 players on this list, then it is safe to expect they can deploy with everyone else. As a point of reference, the first company on the list — Turner — does approx. 1,500 construction projects per year. See complete list here: ENR 2022 Top 400 Contractors

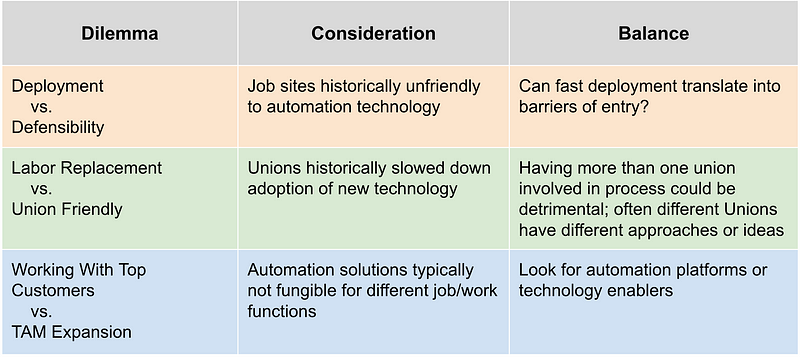

Construction Robotics Framework

We summarize the main considerations into deployment vs defensibility, labor replacement vs union friendly, and top industry players vs TAM expansion.

Applying the Framework

When applying the framework to compare different companies, we look at ease of deployment, barriers of entry, labor replacement, unions, projects with top industry players and TAM Expansion. Example below:

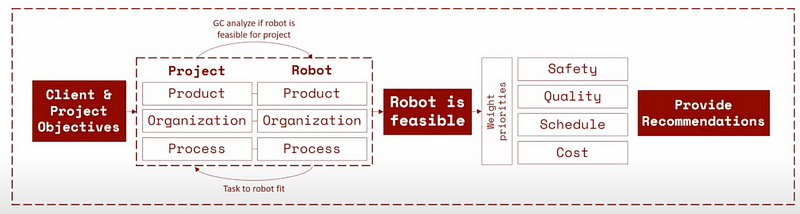

Robotics Evaluation Framework by Center for Augmented Computational Design in AEC

Another example of a framework developed by the Center for Augmented Computational Design in AEC — their “Robotics Evaluation Framework” is based on industry cases and literature review; it covers the following three key points:

A. Client & project objectives

B. Feasibility of robot for the project

C. Recommendations

Examples of Companies Working on Enabling Technologies

Humatics

Microlocation technology with Radio frequency sensors and analytics software

Background

- Until now, microlocation technologies haven’t taken hold because they’ve either suffered from precision problems or have been too expensive to calibrate [8]

- The decision by Apple and Samsung to start including UWB chipsets in their phones is a good indicator of the technology’s future potential [8]

- Currently raising Series C

Dynamic Pick Technology Snapshot

Positives

- Microlocation can enable deeper levels of human-robot collaboration

- They do not rely on optical sensors, and are immune to sunlight, darkness, dust and paint

- Faster than imaging or computer vision

- More suitable for harsh environments

Negatives

- Installation of sensors on both sides of operation is needed

- Sensors need to be installed every few meters

- The second vertical on their roadmap is HealthTech; FDA approvals will be needed; may be slow to roll

Fundraising

- Currently raising Series C in late Q3 / early Q4

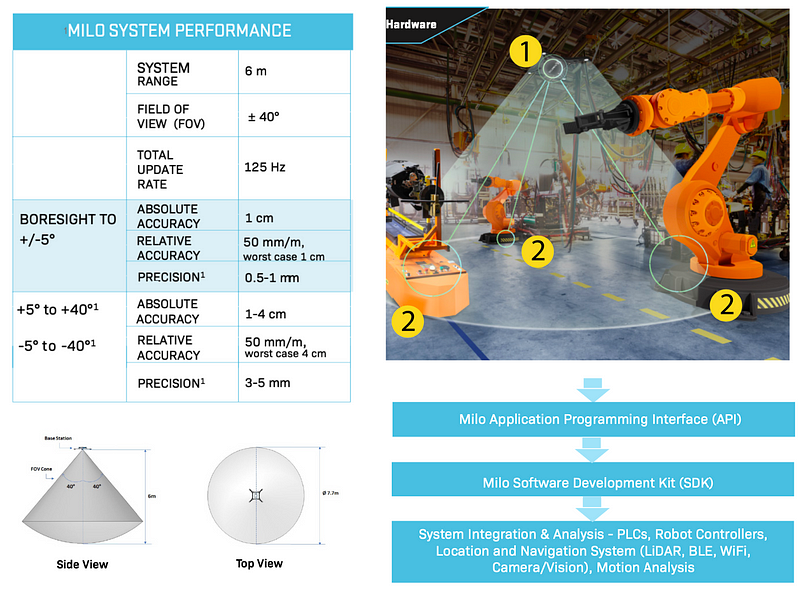

Technology Overview

- Millimeter scale positioning system consisting of one or more base stations and multiple transponders

- The Base Station measures the position of each Transponder within its field of view (FOV) with sub-millimeter precision at a rate that is sufficient for real-time control and other highly demanding applications

- Low-power millimeter-wave signals are used to determine the Transponder’s position

- The Milo Base Station projects a coverage area called the “cone of precision”

- The Transponders may be placed on a variety of objects (e.g., vehicles, robot arms, tools), unlocking the ability to precisely coordinate the actions of disparate systems with one another

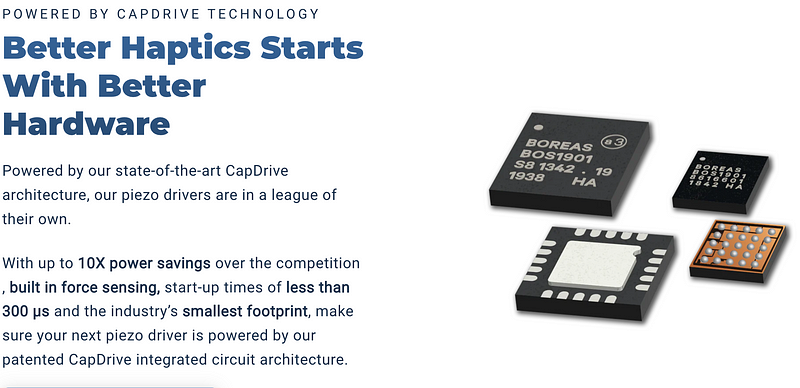

Boréas Technologies

Background

- Integrated circuits for haptic applications

- Low-power piezo haptic driver integrated circuits that can be used in small wearables, mobile devices, car infotainment panels

- High-definition feedback

- Their beachhead is mobile and PC; they claim most PCs will have a haptic trackpad by 2025. We confirmed with the CEO that robotics applications are on their internal roadmap.

- Raising Series B Fall 2022

Positives

- Technology is applicable to many different verticals including teleoperation of underwater vehicles, gaming, AR/VR, robotics, health, safety related tech and others

- Real, hard to copy patents and intellectual property

- Truly “HardTech” technology with hardware + software components

Negatives

- Market readiness and timing is difficult to define for this sector; AR/VR was overhyped for a while and still slightly behind on delivering mass-market products, although progressing quicker at present

- Supply chain dependencies may slow down market adoption and hitting deliverables given current macro environment

Fundraising

- Raised $6.5 million of Series A2 venture funding from undisclosed investors on April 22, 2022

- Currently in discussions for series B

Technology Overview

- BOS1901 piezo driver integrated circuit can be up to 10 times more efficient than legacy haptic technologies like ERM and LRA

- The BOS1901 is the first ultra-low-power piezo driver to create feedback and sense force from the same piezo actuator

- The near-instantaneous start-up time of our BOS1901 piezo drivers is ideal for creating high-definition haptic effects

Examples of Construction Robotics Companies

Raise Robotics

- Raise Robotics aims to eliminate all delays and injuries on the construction site by developing a robotic workforce that operates under human supervision

- Technology will build upon the industry’s adoption of BIM to enable machines to construct entire buildings to spec

- To start, they are targeting the facades market, where use of 3D modeling is widespread

- Very early, definitely one to keep an eye on for future rounds

Light YX

- Projects laser from blueprints onto construction surfaces to assist field workers during construction; 2D and 3D projections provided

- They are partially automating the workers, making them more efficient

- Claims increased productivity 400% and decreases rework of up to 70%

- Light YX vs. Dusty Robotics: projects layouts on floor, ceiling or walls vs floor only; Dusty’s printing layout so far is not flexible, and needs to have a clean floor, which is difficult with construction sites

- Currently raising a Seed round

SkyCurrent

- Robot as a service model to automate high-rise building cleaning; key rationale is safety concern of workers

- 1:6 FTE replacement ratio; 80% gross margin

- Same business model as existing subcontractors, POs done same way as currently but cheaper

- Raas model

- Can withstand high winds, wind tunnel tested; can boost motors on ducted fans to increase adhesion if necessary

- Current length constraint is ~350 feet of cable / 30 stories max, but working on improving

- Rope access is being regulated out of existence, swing stage preferred by regulators

- Currently raising a Seed round

- Main concern is limited TAM, potentially good lifestyle business

BotBuilt

- Our personal opinion is that Botbuilt is not taking the right approach. They are using universal arm robots to build a very simple structure

- Given what they are doing, there is really no need for heavy and expensive universal robot arms (No clear need for six axis of movement, or capability to lift very heavy items)

- These type of universal arm robots move rather slowly even when compared to human movement

- We think there is a real opportunity to design a new robotic system specifically designed to do this type of work

Others Worth Mentioning

- Canvas

Developer of robotic technology designed to improve the quality of construction on infrastructure. The company’s technology empowers the current workforce to be productive and free from repetitive, physically taxing, and dangerous tasks, enabling construction companies to improve the quality and affordability of buildings, simultaneously improving the working conditions of the people who build these spaces. - Built Robotics

Company’s automated guidance systems can be installed on existing equipment from any manufacturer, while maintaining complete manual operation capabilities. Tasks: digging trenches, excavating foundations, and grading building pads. Fleet can be managed via a web-based platform, which lets remote equipment operators to supervise the robots. - NOVARC

Welding is toxic environment, workers are 3 meters away, they check welding quality right away with machine vision; normal welding is 45min-1hr for typical pipe welding; with Novarc, it takes 10 minutes; but issue remains with 1 person per 1 robot. - Rugged Robotics (competitor to Dusty Robotics)

Modernizing the commercial construction sector, starting with a “layout Roomba” that marks architectural and engineering designs directly onto unfinished concrete floors, has raised $9.4 million in Series A funding co-led by BOLD Capital Partners and Brick & Mortar Ventures. - Also see: Offsitek(competitor to BotBuilt), SkyMul (rebar tying), TyBot (rebar tying), Dusty Robotics (layout robot), Versatile (smart crane), Fastbrick Robotics, Envelope (zoning visualization)

Teleoperation & Safety

- Telexistence

Developer of robotic technologies designed to be the systematic innovator of scale in robotics. The company’s online remote control robotics technology transmits, accumulates, and analyzes everything from visual and auditory to tactile information, enabling users to act freely in remote environments and expanding the presence of human beings - Cobalt Robotics

Teleop robotics for human-robot interaction in commercial buildings - Also see: Teleo, SafeAI, Formant, Phantom, Clear Path Robotics

Platforms and Enabling Technologies

- FORT Robotics

Developer of wireless functional safety systems designed to ensure human safety around autonomous machines. The company’s solutions help builders and users of robotic systems to accelerate development, mitigate threats, and stay in control, providing construction, agriculture, and manufacturing businesses with a sufficient level of safety and reliability - Freedom Robotics

Developer of a cloud-based software infrastructure platform designed for modern robotics applications. The company offers mission-critical software infrastructure to enable the next generation of robotics companies to build, operate, support, and scale robots and robotic fleets, enabling robotic companies to bring their product to market with minimal resources. - Forcen

Forcen has developed ForceFilm, a flexible, durable haptic sensor that it said provides “human-level touch” to surgical robots and other systems.

Inspection Automation

- DOXEL

Continuous performance monitoring and predictive insights to stay one step ahead of delays and cost overruns; See Surveyor — Doxel partners with project teams using state of the art technology to capture hundreds of thousands of sq.feet of your project, every week — we call this our digital surveyor. - Skydio

Skydio Skills perform complex tracking, navigation and obstacle avoidance maneuvers while maintaining cinematic composition — all with the press of a button - FlyAps

Inspection Company for construction, Oil & Gas; attaching sensors to drones and looking for leaks etc; construction sector very slow for them due to regulation issues - Also see: OpenSpace — project progress and inspection tool; VEERUM — work site monitoring; YNOMIA — real time construction data; Cumulus — project workflow digitization; SafeHub — IoT for building safety; Verkada — building safety (commercial building security cameras)

Window Cleaning

High Rise Window-Install

Exoskeletons

- Verve Motion

The technology behind SafeLift has been developed at Harvard over the past decade, and is based on the latest advances in robotics, apparel design, and movement science. The suit applies assistance in parallel with the user’s muscles and responds to their movement in milliseconds. - See also: Ekso Bionics

Demolition

7. Areas of Improvement for the ConstructionTech Industry

There is an opportunity for the construction industry to better manage transparency and risk sharing in contracts. The current status quo is to see contracts as “adversarial opportunities to hand off risks” [2] However, contracts could be recast as tools for “fair sharing of risks and rewards” [2] so as to help all sides succeed and avoid delays — be it plumbing, HVAC, mechanical, lighting, painting, project management, etc… Owners and contractors should be able to “share equitably the benefits that arise from the adoption of technological and process innovations” [2]. Risks are often passed to other areas of the value chain instead of being addressed, and players make money from claims rather than from good delivery. [7]

Misaligned contractual structures and incentives

Per McKinsey, “The multitude of stakeholders in a project rarely collaborate well because of misaligned incentives. Owners often tender projects at the lowest cost and pass on risks such as soil properties or rising prices for materials that they might better handle or absorb themselves. Engineers are often paid as a percentage of total construction cost, limiting their desire to apply design-to-cost and design-to-constructability practices. General contractors are often only able to make profits via claims, so rather than highlighting design issues early in a project they often prefer charging for change orders later. Incentives and discounts from distributors and material suppliers to subcontractors obscure material prices” [7]

8. Conclusion

Even companies with every possible advantage have a tough time in the construction industry (think Procore, Katerra or View)

At the Seed and Pre-Seed stages, it is unclear where investors should play to find a winner in the construction tech space — it is inherently risky with limited upside, and there are many look-a-like approaches —unless the investor reaches full conviction, it is probably safer to wait to invest at series B/C.

Another approach could be to bet on something crazy and aggressivewith unlimited upside, like an all-together new type of housing approach such as suburban Yurt farms, a modular community that is super eco friendly and tech forward with combinations of “robotics + live + work” enhancements, or an “over 55” community look-a-like but built from the ground up for younger folks with families.

9. Appendix:

Top 50 construction startups by total funding received [9]

Top 50 VC funds by number of construction startups they’ve backed [9]

Top PropTech Focused VC Funds

Navitas |navitascap.com

JLL Spark | spark.jll.com

Builders | builders.vc

UIF | urbaninnovationfund.com

Fifty Years | fiftyyears.com

MetaProp | www.metaprop.vc

Brick&Mortar | brickmortar.vc

Fifth Wall | FifthWall VC

Suffolk | www.suffolk-tech.com

10. References

[1] Robotics Business Review | Autonomous Construction Solutions Advance as Industry Specific Challenges Addressed

[2] Imagining construction’s digital future; Capital Projects and Infrastructure June 2016; McKinsey Productivity Sciences Center, Singapore

[3] catused.cat.com |3 Reasons to Consider Used Equipment; In the market for a machine? See why Cat Used® Equipment may be your best option.

[4] Center for Augmented Computational Design in AEC; Talk 5: Cynthia Brosque - Comparative analysis of robotic and traditional construction methods

[5] McKinsey | Modular construction: From projects to products

June 18, 2019

[6] Bloomberg.com | Biden’s New Housing Plan: Fire Up the House Factories

[7] McKinsey | The Next Normal In Construction, June 2020

[8] Nanalyze | Microlocation and The Internet of Moving Things

[9] Construction Physics | A Brief History of Construction Startups

Prefab & Modular Research

[10] Forbes | Forget Everything You Know, Modular Will Be Worth It

Modular construction has had a rough time getting large scale adoption. Making it work may take ditching all past practices to start new, and if you can do that, it promises to pay off big.

Apr 16, 2021

[11] Turner Center | First Ever Statewide ADU Owner Survey Shows Growth, Room for Improvement — Terner Center

Accessory dwelling units (ADUs) have become an increasingly popular housing choice in California in recent years. This boom was buoyed by state legislative changes over the last several years that removed barriers to constructing ADUs. As recent research from University of California, Berkeley’s Terner Center and Center for Community Innovation

Apr 22nd, 2021

[12] Fast Company | Can Blu Homes Fulfill the Promise of Prefab?

A Boston start-up says its method will at last fulfill the promise of cheap manufactured homes.

Oct 6, 2009

[13] Fast Company | Prefab was supposed to fix the construction industry’s biggest problems. Why isn’t it everywhere?

The Canadian company Bone Structure can produce zero net energy homes months faster than a traditional builder. But its challenges highlight the difficulty of disrupting the entrenched construction industry.

Oct 8th, 2020

[14] CB Insights Research | The Future Of Housing: From Home Building To City Planning, Tech Giants & Startups Are Reimagining Where & How We Live

Major US technology companies are constructing corporate housing, self-sufficient towns, and even entire urban neighborhoods. Adding to the mix, insurgent startups are also redefining how the homes of the future will be built.

Jun 14th, 2018

[15] Crunchbase News | Autodesk Scoops Up PlanGrid For $875M As Construction Tech Exits Heat Up

Autodesk, Inc. said today it plans to acquire cloud-based software startup PlanGrid for $875 million “net of cash.”

Nov 20th, 2018

[16] WSJ | How a SoftBank-Backed Construction Startup Burned Through $3 Billion

The downfall of Katerra shows how the Silicon Valley strategy of growth at any cost can backfire in complicated industries like real estate.

June 29, 2021

[17] Construction Dive | Modular builder CEO: ‘Katerra’s failure was spectacular’

The head of Volumetric Building Companies shares why he purchased the bankrupt firm’s California factory and how he will avoid similar pitfalls.

Nov. 24, 2021

[18] minneapolisfed.org | Solving the Housing Crisis will Require Fighting Monopolies in Construction | Federal Reserve Bank of Minneapolis

Dec 11, 2020

[19] procore.com | The Most Dangerous Jobs in Construction

Proper training and safety protocols on the jobsite go a long way to reducing the number of fatal injuries suffered on the job.

[20] Bridgit | Top 12 highest-paid construction jobs — Bridgit

In this article, we’ll take a look at 12 of the highest-paid construction jobs to give you an idea of the promising opportunities available in this rapidly-growing sector.

Oct 16th, 2020

[21] Medium | How 3D Printing Could Disrupt the Housing Industry

A new generation of startups are determined to disrupt the housing industry. Innovative early-stage ventures are striving to automate…

Sep 3rd, 2021

Robotics Research

[22] Robot Enthusiast | Seamless transitions between autonomous robot capabilities and human intervention in construction robotics — Robot Enthusiast

Congratulations to the winners of the best paper award of the International Association for Automation and Robotics in Construction 2021. The team around Cynthia Brosque, Elena Galbally, Prof. Martin Fischer, […]

Mar 15th 2022

[23] The Robot Report | SRI on the future of robotics

Currently, teleoperation technologies aren’t available in situations where they may be of most use, such as on battlefields, because of distance and bandwidth issues.

Jan 25th 2022

[24] Robotics Business Review | How Microlocation Will Open New Frontiers for Robotics, Smart Cities

Humatics CEO David Mindell talks with Robotics Business Review about how millimeter-based precision, called microlocation, will help self-driving cars, industrial robotics, and smart city development.

Jul 11th, 2018

[25] Construction Dive | Strong contech funding rounds kick off the year

Construction technology firms, including high-profile companies such as The Boring Co., have pulled in millions over the past four months.

April 27, 2022

[26] Global News Wire | Construction Robots Market — Growth, Trends, COVID-19 Impact, and Forecasts (2021–2026)

The construction robot market is expected to grow at a CAGR of approximately 13. 56% during the forecast period from 2021 to 2026.

April 15, 2021

[27] Robotics Business Review | 5 Ways Robotics Will Disrupt the Construction Industry in 2019

From improving efficiency and performing redundant tasks, here’s how robotics can help the construction industry automate many of its manual processes.

Jan 23rd, 2019

[28] Automate | 3 Ways Robots Are Making Construction Safer

Construction robots have the potential to prevent accidents and transform the industry — if they’re used properly.

5–14–2020

[29] The Robot Report | Freedom Pilot, Resource Monitor built to enable rapid robot deployment

Freedom Robotics said its cloud-based Freedom Pilot and Resource Monitor can speed robot deployment, development, and management across verticals.

Aug 3rd, 2020

[30] The Robot Report | ForceFilm from Forcen brings sensitivity to robots, surgical instruments

Forcen has developed ForceFilm, a flexible, durable haptic sensor that it said provides “human-level touch” to surgical robots and other systems.

Jun 27th, 2020