The Future of Warehouse Automation: From Robotic Induction to Full-Path Solutions

A comprehensive analysis of the $13.7 billion opportunity reshaping warehouse operations through emerging technologies and market disruption

Executive Summary

The warehouse automation industry stands at a critical inflection point where traditional material handling equipment (MHE) approaches are reaching their operational and economic limits. While conventional automation systems have addressed labor challenges, they have simultaneously created new bottlenecks and inefficiencies that significantly impact overall facility performance. This comprehensive analysis reveals how emerging technologies, particularly full-path automation, represent a paradigm shift that addresses these systemic issues while creating unprecedented market opportunities.

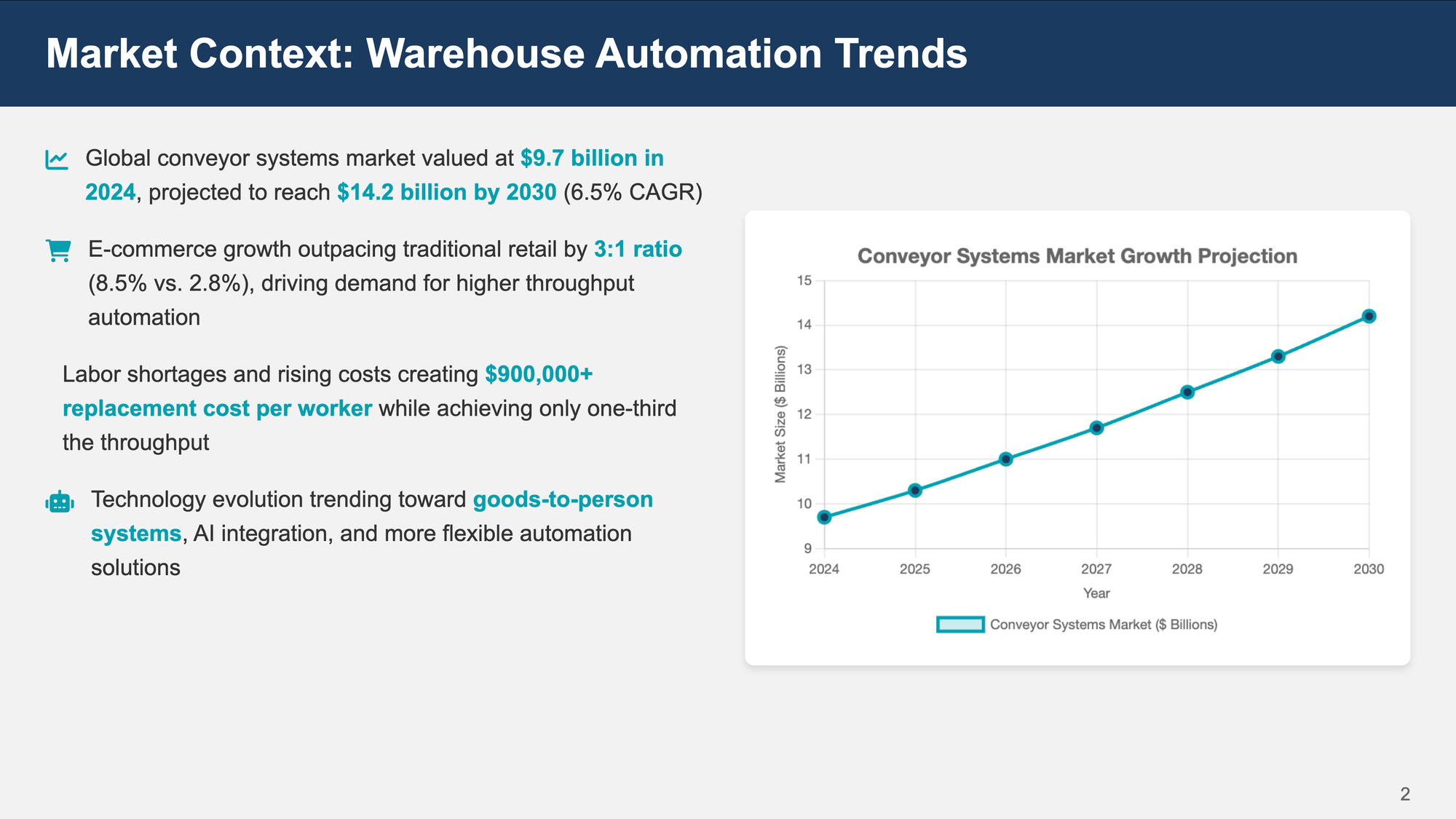

The global warehouse automation market, valued at $27.4 billion in 2024 and projected to reach $69.5 billion by 2030, encompasses multiple technology segments that are experiencing varying degrees of disruption. The conveyor systems market alone represents $9.7 billion in 2024, growing to $14.2 billion by 2030, while the robotic induction systems segment adds another $4.0 billion, creating a combined addressable market of $13.7 billion for technologies that can eliminate traditional system limitations.

Recent industry analysis reveals that traditional approaches to warehouse automation are reaching diminishing returns, with replacement costs often exceeding $900,000 per human worker while achieving only one-third the throughput. This economic reality, combined with the operational challenges of maintaining complex MHE systems, creates a compelling case for alternative approaches that can deliver superior performance at lower total cost of ownership.

Full-path automation technology emerges as the most promising solution to these challenges, maintaining continuous custody of individual items from pick to final destination using intelligent shuttles operating on track-based infrastructure. This approach eliminates the need for intermediate handling, reduces maintenance requirements, and provides superior throughput characteristics compared to traditional systems while simultaneously eliminating the need for expensive robotic induction systems that currently represent a significant market segment.

Market Context and Industry Dynamics

The Current Warehouse Automation Landscape

The warehouse automation market operates within a complex ecosystem of competing technologies, each addressing specific aspects of the fulfillment process. Automated Storage and Retrieval Systems (ASRS) have become the dominant approach for goods-to-person operations, with major implementations focusing on reducing worker movement and increasing pick density. These systems typically feature three-dimensional storage cubes with robotic systems that bring entire shelves or storage pods to human workers stationed at pick positions.

Current market leaders have established significant positions through comprehensive system integration capabilities. Amazon Robotics (formerly Kiva Systems) has deployed hundreds of thousands of mobile robots across their fulfillment network, fundamentally changing how e-commerce fulfillment operates. Traditional material handling companies such as Dematic, Vanderlande, BEUMER Group, and Honeywell Intelligrated continue to dominate large-scale installations through their ability to design, implement, and support complex automation systems over extended periods.

The market has evolved toward increasingly sophisticated solutions that combine multiple automation technologies, including robotic picking, automated packaging, and intelligent sortation systems. However, this evolution has also increased system complexity and created new challenges that impact both operational efficiency and economic performance.

Economic Drivers and Market Forces

The economic drivers for warehouse automation continue to intensify as e-commerce growth outpaces traditional retail by a factor of three to one. E-commerce sales are growing at 8.5% annually compared to just 2.8% for total retail sales, creating sustained demand for warehouse automation that can handle the complexity, speed, and accuracy requirements of modern fulfillment operations.

Labor shortages in key distribution markets have driven wage inflation while simultaneously reducing the available workforce for manual operations. These trends create sustained demand for automation solutions, but also highlight the importance of selecting technologies that can deliver long-term value rather than simply replacing human workers with expensive robotic alternatives.

The sophistication of modern warehouse operations would surprise most people outside the industry. Today's facilities process thousands of different products with varying sizes, weights, and handling requirements while maintaining accuracy rates exceeding 99.5% and throughput rates measured in tens of thousands of items per hour. This operational complexity requires automation solutions that can adapt to changing requirements while maintaining consistent performance levels.

Current System Limitations and the Robotic Induction Problem

The "Throw and Sort" Challenge

Contemporary warehouse automation systems suffer from a fundamental flaw that industry practitioners call the "throw and sort" problem. Items lose their individual identity as they move through the fulfillment process, necessitating repeated identification, singulation, and consolidation cycles that consume significant resources while introducing multiple failure points.

The typical fulfillment process in an automated facility involves multiple discrete steps, each requiring specialized equipment and human oversight. Items retrieved from ASRS systems are initially placed into containers or onto conveyor systems where they lose their individual tracking. These items must then be singulated—separated into individual units—before being sorted into appropriate downstream processes.

This singulation process is particularly problematic, as items can overlap, fall behind other items, or become damaged during the mechanical separation process. Following singulation, items enter consolidation processes where multiple items destined for the same customer order are brought together, typically at "mailbox walls"—large arrays of individual compartments where items are manually sorted by human workers.

The Robotic Induction Market Response

The challenges of manual induction processes have created an entire industry segment focused on robotic induction systems—expensive, complex solutions designed to automate the manual placement of items onto sortation equipment. The robotic induction systems market, valued at $4.0 billion in 2023 and projected to reach $5.68 billion by 2032, represents a significant investment in solving a problem that shouldn't exist in the first place.

Modern robotic induction systems employ six-axis articulated robots equipped with sophisticated vision systems and specialized end-effectors designed to handle diverse package types. These systems typically cost $200,000 to $500,000 per installation, require 8-12% of system cost annually for maintenance, and demand 100-200 square feet of floor space including safety zones and maintenance access areas.

While these systems can achieve throughput rates of 1,000 to 3,000 packages per hour with accuracy rates exceeding 99.5%, they add significant complexity to warehouse operations. The integration requirements include sophisticated software connections with warehouse management systems, sortation control systems, and upstream automation equipment, often requiring six to twelve months for complex installations.

The fundamental limitation of robotic induction systems is that they address symptoms rather than causes. By automating the placement of items onto sortation systems, these solutions add complexity and cost while failing to address the underlying "throw and sort" problem that necessitates induction in the first place.

Maintenance and Operational Challenges

Maintenance requirements for traditional MHE systems represent a substantial operational burden that is often underestimated during system design. Conveyor systems require regular maintenance shutdowns, typically occurring weekly or monthly depending on system complexity and utilization levels. These shutdowns not only reduce available operating time but also require specialized maintenance personnel and replacement parts inventory.

The cumulative impact of maintenance activities can represent 5-10% of total facility operating costs, while the capital investment in MHE systems typically accounts for 20% of total facility construction costs. The downstream sortation process presents additional challenges, particularly in facilities processing high volumes of mixed items. Main recirculating sorters operate as bottlenecks that limit overall system throughput, typically processing 16,000 to 20,000 items per hour and effectively capping facility capacity regardless of upstream automation investments.

When downstream processes become congested, items recirculate through the sorter multiple times, eventually being diverted to manual handling processes that significantly increase operational costs. This cascading effect demonstrates how individual system limitations can impact overall facility performance in ways that are difficult to predict during system design phases.

Full-Path Automation: A Paradigm Shift

Technology Architecture and Design Philosophy

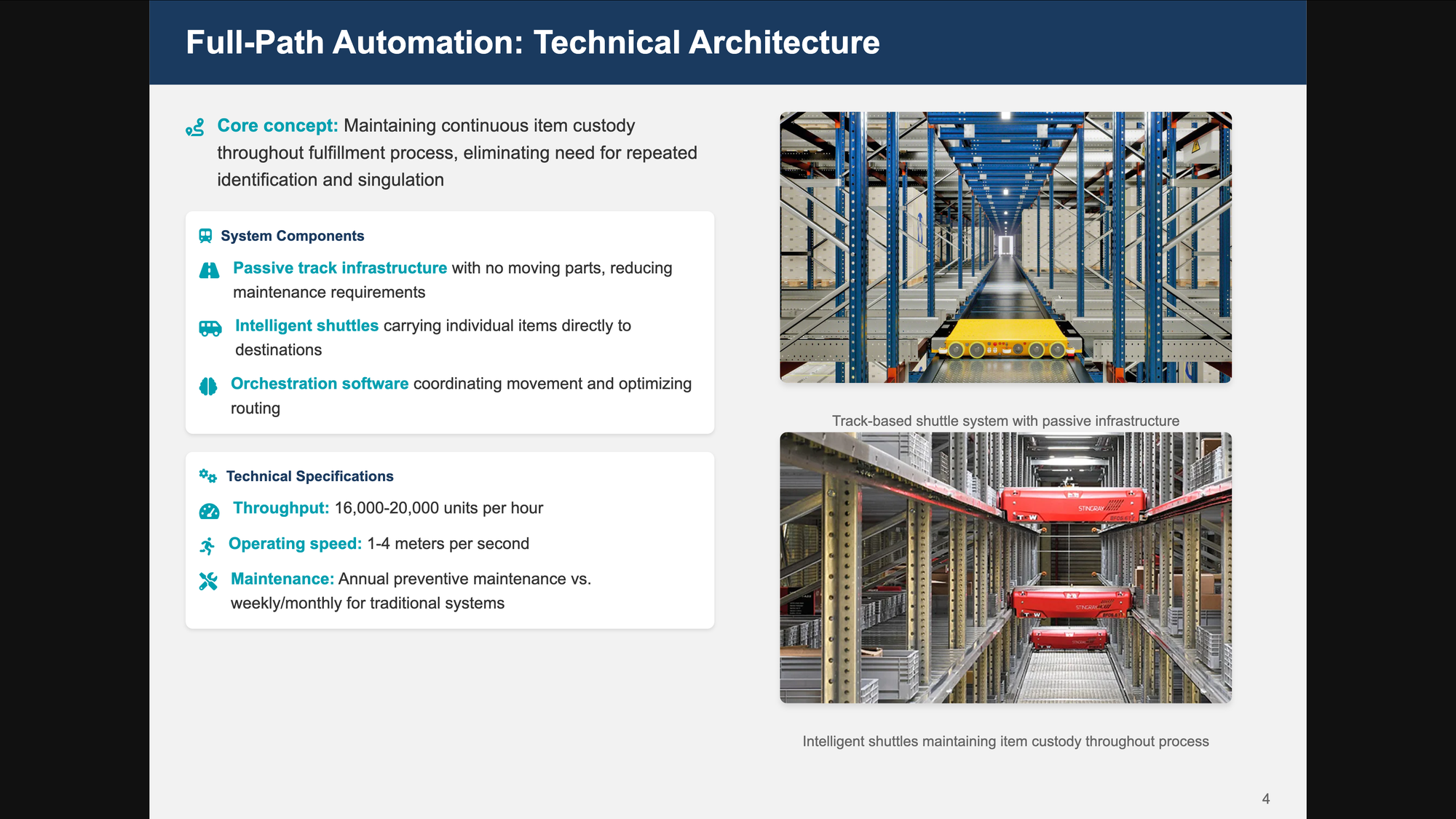

Full-path automation represents a fundamental departure from traditional warehouse automation approaches by maintaining continuous item custody throughout the fulfillment process. The technology architecture consists of three primary components: passive track infrastructure, intelligent shuttles, and orchestration software that coordinates system operations. This architecture eliminates the need for intermediate handling and re-identification processes that characterize traditional systems.

The passive track infrastructure forms the foundation of the full-path automation system, consisting of rails or guide systems that require no moving parts or active components. This design approach significantly reduces maintenance requirements compared to traditional conveyor systems, which rely on motors, belts, and mechanical components that require regular service and replacement. The track system can be configured in complex three-dimensional layouts that optimize space utilization while providing flexible routing options for different item types and destinations.

Intelligent shuttles operate on the track infrastructure, serving as autonomous vehicles that carry individual items or small batches directly to their destinations. These shuttles incorporate onboard intelligence that enables them to navigate the track system, communicate with the central orchestration system, and adapt to changing operational conditions. The shuttle design eliminates the need for mechanical singulation processes, as each item maintains its individual identity and routing information throughout the fulfillment process.

Eliminating Robotic Induction Requirements

Full-path automation technology enables what industry practitioners term "free machine induction"—the ability to accept items directly from upstream processes without requiring specialized placement or orientation. Items entering the full-path automation system maintain their individual identity and routing information, eliminating the need for vision systems, robotic manipulation, or manual placement that characterizes traditional induction processes.

This elimination of induction requirements provides several significant advantages over traditional approaches. System complexity is reduced by eliminating multiple specialized components, improving system reliability by removing failure points associated with robotic components and vision systems. Space requirements are reduced by eliminating the need for robotic work cells and safety zones, while maintenance requirements are simplified by removing complex robotic systems that require specialized service and support.

The economic advantages of eliminating robotic induction systems are substantial when considered across the full system lifecycle. The elimination of $200,000 to $500,000 in robotic induction equipment represents immediate capital cost savings that improve project economics. The elimination of ongoing maintenance costs, which typically represent 8-12% of system cost annually, provides substantial operational savings over the system lifecycle.

Technical Specifications and Performance Characteristics

Technical specifications for full-path automation systems demonstrate significant advantages over traditional approaches. Throughput capabilities range from 16,000 to 20,000 units per hour, matching or exceeding the performance of high-speed sortation systems while operating at significantly lower speeds that enhance safety and reduce mechanical stress. Operating speeds of 1-4 meters per second provide adequate throughput while enabling safe interaction with human workers when necessary.

The cost structure of full-path automation systems compares favorably to traditional alternatives, with total system costs ranging from $1,400 to $1,800 per linear foot. This cost includes track infrastructure, shuttles, and control systems, representing a comprehensive solution that eliminates the need for multiple specialized MHE components. The maintenance profile of full-path automation systems is particularly attractive, requiring only annual preventive maintenance on shuttles compared to weekly or monthly shutdowns required by traditional conveyor and sortation systems.

Energy consumption patterns differ significantly between full-path automation and traditional systems, with implications for both operational costs and environmental sustainability. Traditional conveyor systems operate continuously regardless of load, consuming energy to maintain belt movement and system readiness. Full-path automation systems consume energy only when shuttles are in motion, providing opportunities for significant energy savings in facilities with variable throughput requirements.

Economic Analysis and Market Opportunity

Comprehensive Cost Comparison

The economic case for full-path automation extends beyond simple capital cost comparisons to encompass total cost of ownership considerations that include operational expenses, maintenance requirements, and system reliability factors. Traditional warehouse automation systems often exhibit hidden costs that become apparent only after implementation, including specialized maintenance requirements, system integration complexity, and operational disruptions that impact overall facility performance.

Capital cost analysis reveals that full-path automation systems offer competitive pricing compared to traditional alternatives while providing superior functionality. Motor-driven roller systems and basic sortation equipment typically cost $1,500-2,000 per linear foot, while high-speed shoe sorters and cross-belt sorters range from $2,000-3,000 per linear foot. Full-path automation systems, at $1,400-1,800 per linear foot, provide comparable or lower capital costs while eliminating the need for additional downstream equipment such as merge points and consolidation systems.

The operational cost advantages of full-path automation become more pronounced when considering maintenance requirements and system reliability factors. Traditional conveyor systems require regular maintenance shutdowns that reduce available operating time and require specialized personnel. These shutdowns typically occur weekly for high-speed sorters and monthly for basic conveyor systems, representing significant operational disruptions that impact facility throughput and customer service levels.

Expanded Addressable Market

The integration of robotic induction replacement capabilities significantly expands the addressable market for full-path automation technology. Traditional market analysis has focused primarily on the conveyor and sortation systems market, valued at approximately $9.7 billion globally. However, the inclusion of robotic induction systems adds an additional $4.0 billion in addressable market opportunity, creating a combined addressable market of $13.7 billion.

This expanded market opportunity reflects the comprehensive nature of full-path automation technology, which addresses multiple components of traditional warehouse automation systems through a single integrated solution. Market segmentation analysis reveals that the robotic induction replacement opportunity is particularly attractive in high-volume distribution operations where the cost and complexity of traditional robotic systems create significant operational challenges.

Space efficiency improvements are equally significant. Each eliminated robotic station frees up 100-200 square feet of floor space, providing additional operational flexibility or cost savings. In high-value distribution facilities where space costs can exceed $100 per square foot annually, this space allocation represents a substantial ongoing cost that must be factored into economic analysis.

Competitive Landscape and Strategic Positioning

Traditional Market Leaders

The warehouse automation competitive landscape encompasses several distinct technology categories, each with established players and specific market positions. Traditional material handling equipment manufacturers maintain dominant positions in large-scale warehouse automation projects through their comprehensive system integration capabilities and established customer relationships.

Companies such as Dematic, Vanderlande, BEUMER Group, and Honeywell Intelligrated have developed extensive portfolios of conveyor systems, sortation equipment, and automated storage solutions that address most aspects of warehouse operations. These companies benefit from decades of experience in complex system integration and have established service networks that support ongoing maintenance and optimization requirements.

The robotic systems segment has experienced rapid growth driven by advances in artificial intelligence, computer vision, and mechanical engineering. Amazon Robotics leads this segment with hundreds of thousands of mobile robots deployed across their fulfillment network, while companies like Locus Robotics, 6 River Systems (acquired by Shopify), and Fetch Robotics have developed alternative approaches to goods-to-person automation.

Emerging Technology Providers

The competitive landscape for robotic induction systems includes established players such as Honeywell Intelligrated, Applied Manufacturing Technologies, and major system integrators including Dematic, Daifuku, and Vanderlande. These companies have invested significantly in robotic induction technology development and have established market positions based on their ability to integrate complex robotic systems with existing warehouse automation infrastructure.

However, the fundamental approach of adding robotic complexity to address system limitations creates opportunities for alternative technologies that can eliminate the underlying problems rather than simply automating existing processes. Full-path automation technology positions itself as a comprehensive alternative to traditional warehouse automation approaches rather than simply another component in a complex system architecture.

This positioning provides several strategic advantages in market development and customer engagement processes. The technology enables providers to address a broader range of customer pain points, including not only throughput and efficiency challenges but also the complexity and maintenance burden associated with robotic systems. This broader value proposition can differentiate full-path automation solutions from traditional alternatives that require customers to manage multiple specialized systems and vendor relationships.

Implementation Considerations and Migration Strategies

Integration with Existing Systems

The implementation pathway for full-path automation systems provides flexibility for facilities with existing automation investments. The technology can work alongside existing automation technologies, providing a migration path that protects previous investments while enabling gradual transition to more efficient approaches. This compatibility reduces implementation risk while enabling facilities to realize benefits incrementally rather than requiring complete system replacement.

The orchestration software serves as the central nervous system for the full-path automation system, coordinating shuttle movement, optimizing routing decisions, and integrating with existing warehouse management systems. This software layer enables real-time optimization of system performance, predictive maintenance scheduling, and adaptive responses to changing operational demands.

Integration capabilities allow full-path automation systems to work alongside existing automation technologies, providing a migration path for facilities with significant existing investments. This approach enables facilities to implement full-path automation in specific areas or processes while maintaining existing systems in other areas, reducing implementation risk and capital requirements.

Operational Transformation

Labor cost implications of full-path automation extend beyond simple headcount reduction to encompass skill requirements and operational flexibility considerations. Traditional automation systems often require specialized operators for different system components, creating training requirements and limiting operational flexibility. Full-path automation systems, by maintaining item integrity throughout the process, reduce the need for specialized handling and enable more flexible workforce deployment.

The human factor in current automation systems presents additional challenges that extend beyond simple labor cost considerations. While goods-to-person systems reduce worker movement, they create new skill requirements and introduce ergonomic challenges that can impact worker productivity and retention. Full-path automation systems address these challenges by simplifying operational requirements and reducing the cognitive load associated with managing complex pick sequences.

The economic impact of system reliability differences between full-path automation and traditional approaches is substantial but often overlooked in initial cost analyses. Traditional MHE systems create interdependencies where the failure of any component can impact overall system performance. Full-path automation systems, with their distributed architecture and passive infrastructure, provide inherent redundancy that reduces the impact of individual component failures on overall system performance.

Future Outlook and Market Dynamics

Technology Convergence Trends

The convergence of several market trends supports the growth potential for full-path automation technology. E-commerce growth continues to outpace traditional retail by a factor of three to one, creating sustained demand for warehouse automation solutions. Labor shortages in key distribution markets have driven wage inflation while simultaneously reducing the available workforce for manual operations.

These trends create sustained demand for automation solutions, but also highlight the importance of selecting technologies that can deliver long-term value rather than simply replacing human workers with expensive robotic alternatives. Full-path automation technology addresses these challenges by providing a comprehensive solution that eliminates multiple system components while delivering superior performance characteristics.

The technology development trajectory for warehouse automation increasingly favors integrated solutions that can address multiple aspects of the fulfillment process through unified architectures. Full-path automation technology aligns with this trend by providing a comprehensive platform that eliminates the need for multiple specialized systems while enabling flexible configuration for different operational requirements.

Investment Implications and Strategic Opportunities

The ability to replace robotic induction systems positions full-path automation technology as a comprehensive alternative to traditional warehouse automation approaches rather than simply another component in a complex system architecture. This positioning provides several strategic advantages in market development and customer engagement processes.

The economic value proposition extends beyond simple cost comparisons to include the elimination of entire system components and their associated costs. This comprehensive cost reduction can justify higher initial investment in full-path automation technology while providing superior long-term economics compared to traditional approaches.

The market opportunity for robotic induction replacement represents a significant component of the overall value proposition for full-path automation technology. By addressing this market segment, full-path automation providers can access a broader customer base while providing more comprehensive solutions that address multiple aspects of warehouse automation challenges.

Conclusion

The warehouse automation industry stands at a critical juncture where traditional approaches are reaching their operational and economic limits while new technologies offer the potential for fundamental transformation. Full-path automation technology represents the most promising solution to current industry challenges, addressing both the technical limitations of existing systems and the economic pressures facing warehouse operators.

The comprehensive analysis presented in this report demonstrates that full-path automation technology offers superior technical performance, economic advantages, and strategic positioning compared to traditional warehouse automation approaches. By eliminating robotic induction requirements while providing comprehensive automation capabilities, this technology addresses a combined market opportunity of $13.7 billion while delivering measurable operational and economic benefits.

The investment opportunity extends beyond simple market size considerations to include the strategic advantages of comprehensive solutions that eliminate multiple system components and their associated costs. This positioning enables full-path automation providers to access broader customer bases while providing more compelling value propositions than traditional component-based approaches.

The market dynamics supporting warehouse automation growth, combined with the technical advantages of full-path automation technology, create a compelling foundation for investment consideration. The technology addresses real operational challenges while providing clear economic benefits that can justify investment decisions based on quantifiable returns rather than speculative technology adoption.

As the warehouse automation industry continues to evolve, the companies and technologies that can provide comprehensive solutions to fundamental operational challenges will capture the greatest market opportunities. Full-path automation technology, with its ability to eliminate traditional system limitations while providing superior performance characteristics, represents the next generation of warehouse automation solutions that will define the industry's future direction.

References

[1] Global Market Insights. "Warehouse Automation Market Size, Share & Forecast – 2034." https://www.gminsights.com/industry-analysis/warehouse-automation-market

[2] The Business Research Company. "Warehouse Automation Global Market Report 2025." https://www.thebusinessresearchcompany.com/report/warehouse-automation-global-market-report

[3] MarketsandMarkets. "Conveyor Systems Market - Global Forecast to 2030." https://www.marketsandmarkets.com/Market-Reports/conveyor-systems-market-31314058.html

[4] Precedence Research. "Automated Sortation System Market Size, Share & Trends Analysis Report 2024-2034." https://www.precedenceresearch.com/automated-sortation-system-market

[5] S&S Insider. "Automated Sortation System Market to Hit USD 5.68 Billion by 2032, Fueling Growth through Innovative Technologies and Applications." October 15, 2024. https://www.globenewswire.com/news-release/2024/10/15/2963272/0/en/Automated-Sortation-System-Market-to-Hit-USD-5-68-Billion-by-2032-Fueling-Growth-through-Innovative-Technologies-and-Applications-S-S-Insider.html

[6] Warehouse Automation. "5 Ways Robotics Improves Conveyor And Sortation Induction." December 20, 2021. http://www.warehouseautomation.org/2021/12/20/5-ways-robotics-improves-conveyor-and-sortation-induction/

[7] Honeywell Intelligrated. "Robotic Sorter Induction Systems." 2024. https://automation.honeywell.com/ca/en/products/warehouse-automation/solutions-by-technology/robotics/robotic-sorter-induction

[8] Modern Materials Handling. "Six conveyor & sortation trends to watch." https://www.mmh.com/article/six_conveyor_sortation_trends_to_watch

[9] StartUs Insights. "Warehouse Market Report: Top 10 Emerging Technologies & 1,200+ Startups." https://www.startus-insights.com/innovators-guide/warehouse-market-report/

[10] Association for Advancing Automation. "2024 Funding: A Shift to Stability in Automation Investments." https://www.automate.org/market-intelligence/insights/2024-funding-a-shift-to-stability-in-automation-investments

[11] Exotec. "Top Warehouse Trends for 2025." https://www.exotec.com/insights/top-warehouse-trends-for-2025/

[12] Apex Warehouse Systems. "The Top Warehouse Automation Trends for 2025." https://www.apexwarehousesystems.com/the-top-warehouse-automation-trends-for-2025/

[13] Amazon. "Amazon Robotics: Robots in the Fulfillment Center." https://www.aboutamazon.com/news/operations/amazon-robotics-robots-fulfillment-center

[14] SNS Insider. "Warehouse Robotics Market Size to Reach USD 16.58 Billion with 12.67% CAGR by 2032." September 30, 2024. https://www.globenewswire.com/news-release/2024/09/30/2955220/0/en/Warehouse-Robotics-Market-Size-to-Reach-USD-16-58-Billion-with-12-67-CAGR-by-2032-Driven-by-Increased-Automation-in-Logistics-Research-by-SNS-Insider.html

[15] Applied Manufacturing Technologies. "ROBiN Robotic Induction System." 2024. https://appliedmfg.com/advanced-material-handling/robin-robotic-induction-asrs/

This comprehensive analysis was prepared by Bogdan Cristei and Manus AI