Fintech Pulse: The Silent Revolution: How Stablecoins and Instant Payments are Reshaping Global Finance

Introduction

The world of finance is undergoing a profound transformation, driven by technological advancements that are challenging traditional banking systems and cross-border transactions. At the forefront of this revolution are stablecoins, a new class of cryptocurrencies designed to minimize price volatility, and instant payment systems, which are enabling real-time money transfers across the globe. This article delves into the rise of stablecoins, their growing impact on the financial landscape, and a comparative analysis of global payment systems, highlighting the stark differences in speed and efficiency between regions like Brazil, with its innovative PIX system, and the United States.

The Ascendance of Stablecoins

Stablecoins emerged as a solution to the inherent volatility of traditional cryptocurrencies like Bitcoin and Ethereum. By pegging their value to more stable assets, such as fiat currencies (e.g., the US dollar), commodities, or even other cryptocurrencies, stablecoins aim to provide the benefits of blockchain technology—decentralization, transparency, and efficiency—without the wild price swings that deter mainstream adoption. Their utility extends beyond simply hedging against volatility; they are increasingly being used for remittances, cross-border payments, and as a reliable medium of exchange in the burgeoning decentralized finance (DeFi) ecosystem.

Rapid Growth and Market Dominance

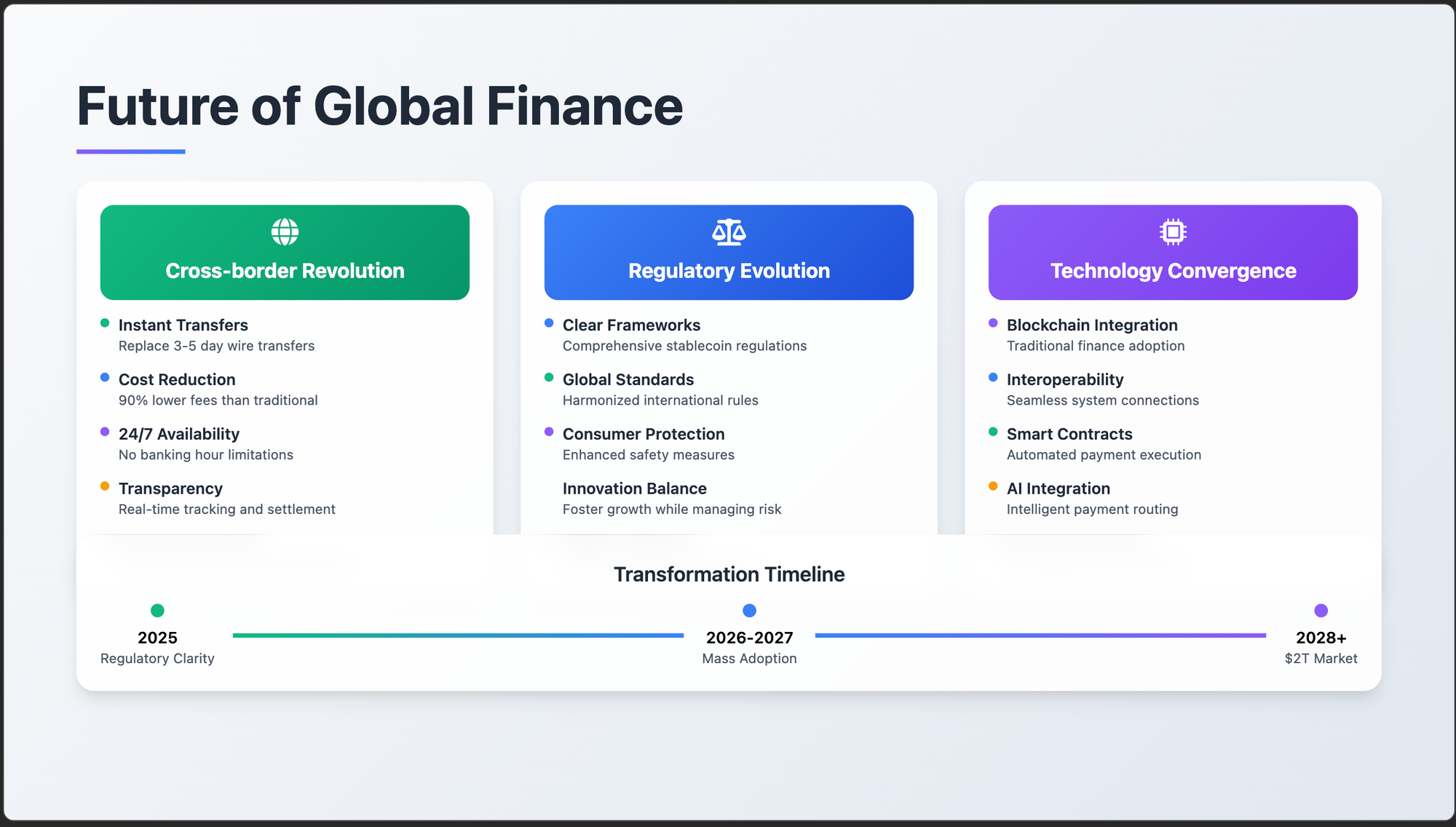

The growth of stablecoins in recent years has been nothing short of remarkable. The average supply of stablecoins in circulation has increased by approximately 28% year-over-year [1]. Originally conceived as a hedge against cryptocurrency volatility, stablecoins have evolved into a cornerstone of financial innovation [4]. Experts predict a significant boom in 2025, driven by growing global use, rising business adoption, and the promise of clearer regulatory frameworks [3]. This rapid expansion is fundamentally rewriting the rules of finance, offering speed, transparency, and cost savings that legacy systems struggle to match [9].

The market capitalization of stablecoins reflects this explosive growth. As of June 6, 2025, the stablecoin market stood at an impressive $247 billion, with projections indicating a potential surge to $2 trillion by 2028 [2]. This represents a staggering forty-five-fold increase since December 2019, when the market capitalization was $232 billion [6]. While some reports from April 2024 indicated a $150 billion market [8], the more recent figures underscore the accelerating pace of adoption and investment in this sector.

Transaction Volume: Outpacing Traditional Giants

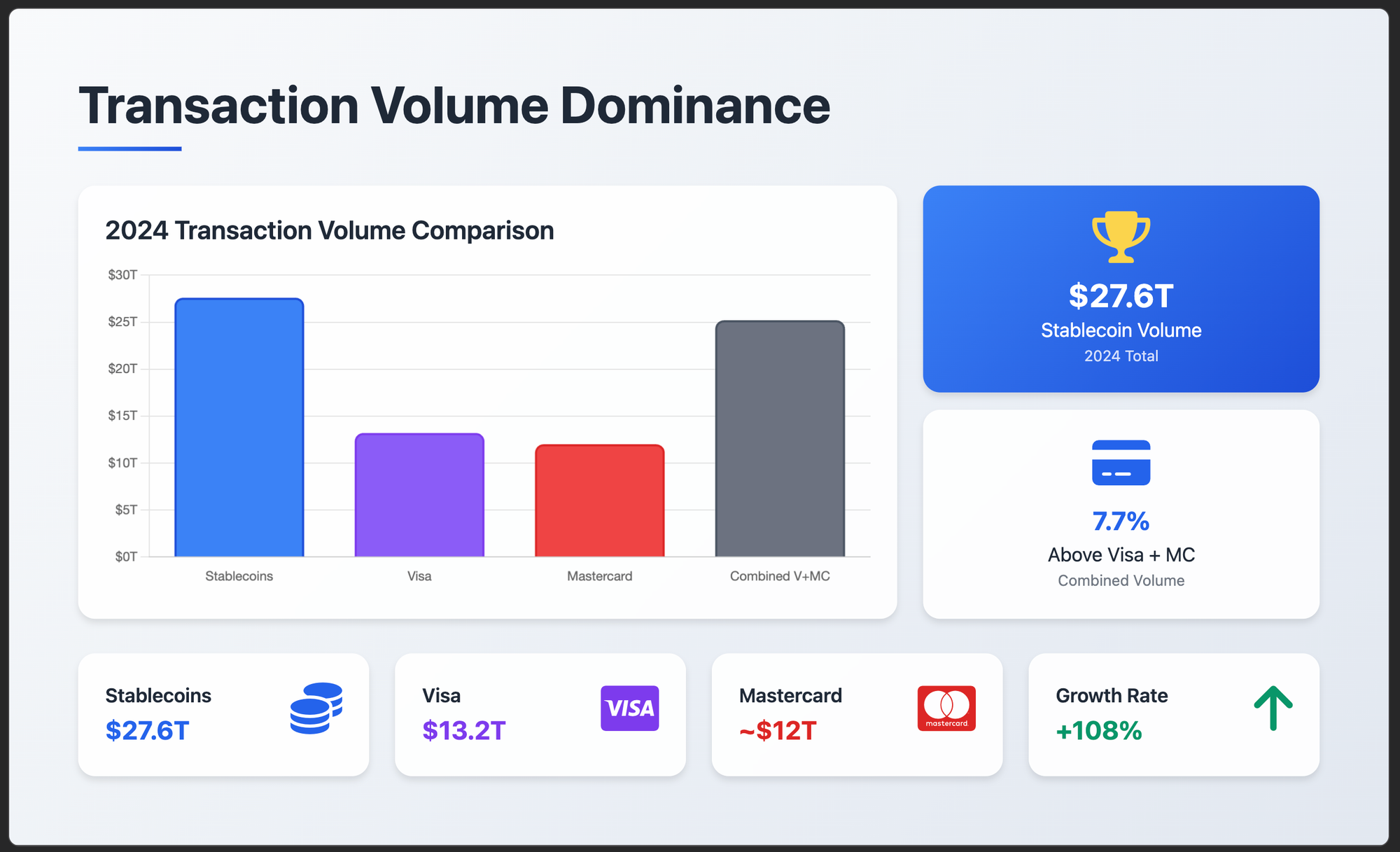

Perhaps one of the most compelling indicators of stablecoin's impact is their transaction volume. In 2024, stablecoins processed a greater transaction volume than even Visa, a long-standing titan in the global payments industry [11]. Total stablecoin volumes reached an astounding $27.6 trillion in 2024, effectively surpassing the combined transaction volumes of both Visa and Mastercard by 7.7% [12, 13, 14, 15, 16]. While some reports from April 2025 cited a figure of nearly $14 trillion in transactions for 2024, still exceeding Visa's $13 trillion [17, 18], the higher figures from more recent sources highlight the immense scale at which stablecoins are being utilized for financial transfers. Even in 2023, the stablecoin market settled over $10.8 trillion worth of transactions, or $2.3 trillion when excluding "inorganic" activity like bots [19]. This demonstrates the significant and growing role stablecoins play in the global financial ecosystem.

Consequences and Ramifications of Stablecoin Growth

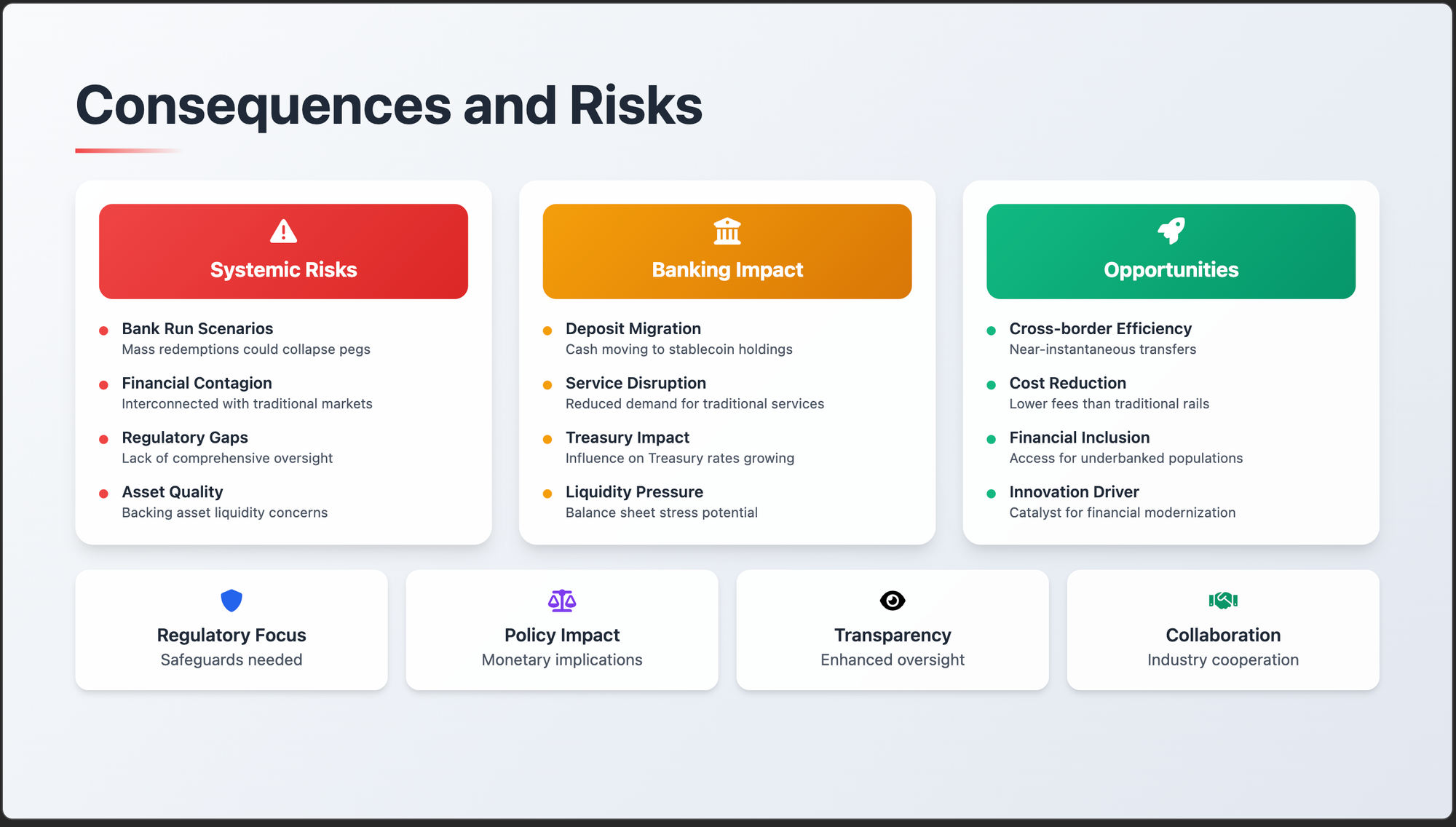

The rapid ascent of stablecoins, while offering numerous benefits, also presents a new set of challenges and potential ramifications for the global financial system. Their increasing integration with traditional markets raises concerns about systemic risk, regulatory oversight, and their impact on monetary policy and financial stability.

Systemic Risk and Financial Stability

One of the primary concerns surrounding stablecoin growth is the potential for systemic risk. If the current trends of stablecoins becoming increasingly intertwined with traditional financial markets persist, they could indeed pose a significant threat to the stability of the financial system [10]. The core of this concern lies in the backing of stablecoins. While designed to maintain a one-to-one peg with a stable asset, usually the US dollar, the quality and liquidity of these backing assets are crucial. If the assets backing a stablecoin drop in value, or if there's a sudden loss of confidence, it could trigger a 'bank run' scenario, where a large number of holders attempt to redeem their stablecoins simultaneously, potentially leading to a collapse of the peg and broader financial contagion [13, 14].

Regulators and financial institutions are actively studying these risks. The Federal Reserve acknowledges that with appropriate safeguards and regulations, stablecoins have the potential to provide a level of stability comparable to traditional safe assets [12]. However, the lack of comprehensive and harmonized global regulations remains a significant hurdle. The blurring lines between cryptocurrency and traditional finance, driven by stablecoin growth, also carry important implications for monetary policy and transparency [15]. Central banks are grappling with how to incorporate these new digital assets into existing frameworks without disrupting financial stability.

Impact on Traditional Banking and Treasury Markets

The growth of stablecoins also presents a direct challenge to traditional banking institutions. As stablecoins offer faster, cheaper, and more efficient payment rails, there's a potential for a shift in how individuals and businesses conduct transactions. This could lead to a decrease in demand for traditional banking services, particularly for cross-border payments and remittances, where stablecoins offer a compelling alternative. The concern for traditional banks is that if cash deposits begin to migrate into stablecoin holdings, it could put pressure on their balance sheets and liquidity [17].

Furthermore, the increasing influence of stablecoins extends to the US Treasury market. As stablecoin issuers often hold a significant portion of their reserves in short-term US Treasury bills, their growth can have a measurable impact on Treasury rates. The Bank for International Settlements (BIS) has quantified this impact, noting that as stablecoins grow, their relative influence on Treasury rates will increase, potentially creating financial stability risks [16]. This highlights the interconnectedness of the emerging stablecoin ecosystem with the bedrock of the global financial system.

A New Hope for Cross-Border Payments

Despite the potential risks, stablecoins are also seen as a significant opportunity, particularly for cross-border payments. The traditional system for international transfers is often slow, expensive, and opaque, involving multiple intermediaries and complex settlement processes. Stablecoins, leveraging blockchain technology, can facilitate near-instantaneous and low-cost international transfers, bypassing many of the inefficiencies of the legacy system. This potential has led many to view stablecoins as a "new hope" for revolutionizing cross-border payments, offering a more efficient and accessible alternative for individuals and businesses alike [8].

Global Payment Systems: A Tale of Two Speeds

The discussion around stablecoins and their potential to revolutionize payments naturally leads to a comparison with existing global payment systems. While some regions have embraced instant payment technologies, others, like the United States, still rely on systems that can take days to settle transactions. This disparity in speed and efficiency has significant implications for economic activity and financial inclusion.

Brazil's PIX: A Model for Instant Payments

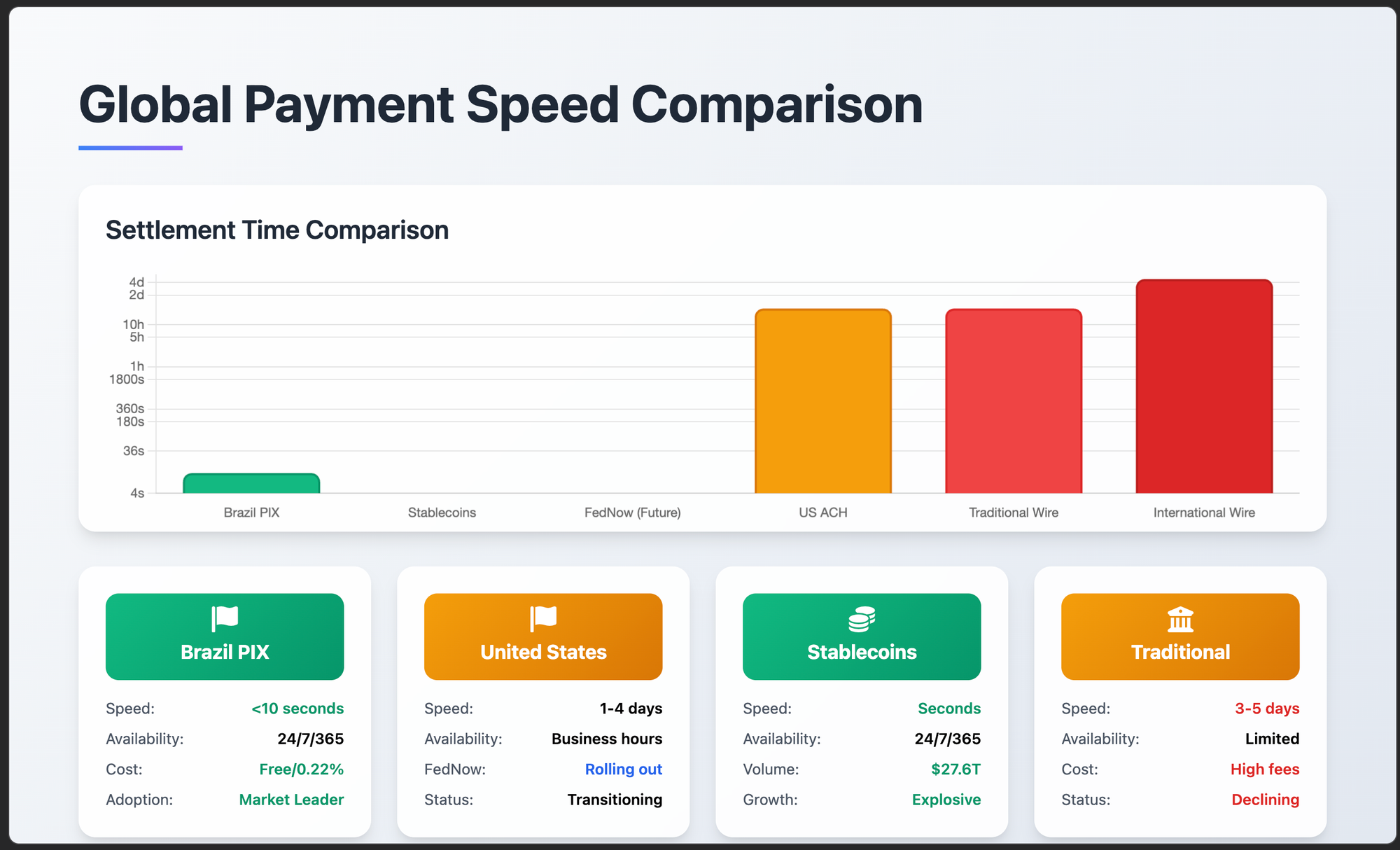

Brazil stands out as a prime example of a nation that has successfully implemented a nationwide instant payment system: PIX. Launched by the Central Bank of Brazil (BCB), PIX is an easy, fast, and affordable solution for both end-users and businesses [20, 21]. Its key feature is the ability to facilitate transactions in less than 10 seconds, 24 hours a day, 7 days a week [23]. This real-time transfer capability applies to Brazilian real between participating financial institutions [24].

The adoption of PIX has been phenomenal. In just three years since its inception, it has become the preferred payment method in Brazil, effectively replacing cash and traditional wire transfers [25]. A significant factor in its widespread success is its cost-effectiveness: PIX is free for consumers and remarkably cheap for merchants, with an average fee of just 0.22% [26]. This combination of speed, convenience, and low cost has made PIX a successful case study for other emerging markets looking to modernize their payment infrastructure [27].

The United States: A Slower Pace of Innovation

In stark contrast to Brazil's rapid adoption of instant payments, the United States has historically lagged in this area. While credit and debit card transactions are often processed instantly at the point of sale, the underlying settlement of funds can still take several business days [28]. Traditional payment networks and banks in the US typically have settlement times ranging from one to four business days [29].

The Automated Clearing House (ACH) Network, a widely used electronic funds transfer system in the US, operates 23¼ hours every business day and settles payments four times a day [30]. The Fedwire Funds Service, another critical payment system, operates for 22 hours a day, 7 days a week, allowing for same-day transfers, but with specific cut-off times [31, 32].

However, there is a concerted effort to accelerate payments in the US. The Federal Reserve's FedNow Service, launched recently, is a new payment rail designed to enable faster bank payments for financial institutions of all sizes, 365 days a year, with the goal of achieving real-time settlement [33]. While a significant step forward, the widespread adoption and full integration of FedNow across the entire US financial ecosystem will take time. The current landscape still means that many everyday transactions, particularly bank-to-bank transfers, are not instantaneous, creating a noticeable difference when compared to systems like PIX.

Conclusion

The rise of stablecoins and the emergence of instant payment systems like Brazil's PIX are fundamentally reshaping the global financial landscape. Stablecoins, with their ability to combine the stability of traditional currencies with the efficiency of blockchain technology, are rapidly gaining traction, processing trillions of dollars in transactions and challenging the dominance of legacy payment networks. While they present potential risks to financial stability and traditional banking models, their promise for faster, cheaper, and more transparent cross-border payments is undeniable.

The comparison of payment systems highlights a clear divergence in innovation. Countries like Brazil have demonstrated the immense benefits of real-time payment infrastructure, fostering greater financial inclusion and efficiency. The United States, while making strides with initiatives like FedNow, still has a journey ahead to achieve the same level of instantaneous settlement. As stablecoins continue to mature and regulatory frameworks evolve, they are poised to play an even more significant role in bridging these gaps, ultimately contributing to a more interconnected, efficient, and accessible global financial system.

References

[1] World Economic Forum. (2025, March 26). Stablecoin surge: Reserve-backed cryptocurrencies are on the rise. https://www.weforum.org/stories/2025/03/stablecoins-cryptocurrency-on-rise-financial-systems/

[2] Reuters. (2025, June 6). Stablecoins' step toward mainstream could shake up parts of US Treasury market. https://www.reuters.com/business/finance/stablecoins-step-toward-mainstream-could-shake-up-parts-us-treasury-market-2025-06-06/

[3] Cointribune. (2025, June 12). Stablecoins on the Rise: 2025 Set to Be a Game-Changer. https://www.cointribune.com/en/stablecoins-on-the-rise-2025-set-to-be-a-game-changer/

[4] Fintech Futures. (2025, June 1). The future of payments: stablecoins and the rise of digital money. https://www.fintechfutures.com/blockchain-crypto-digital-assets/the-future-of-payments-stablecoins-and-the-rise-of-digital-money

[5] FT.com. (2025, June 7). Why we should worry about the rise of stablecoins. https://www.ft.com/content/e5701ff2-d976-451f-9ca2-68cd5f833c1a

[6] Liberty Street Economics. (2025, April 23). Stablecoins and Crypto Shocks: An Update. https://libertystreeteconomics.newyorkfed.org/2025/04/stablecoins-and-crypto-shocks-an-update/

[7] ScienceDirect. (2024). 10 years of stablecoins: Their impact, what we know, and what we don't. https://www.sciencedirect.com/science/article/pii/S0165176524004233

[8] Convera. (2024, April 26). The rise of stablecoins: A new hope for cross-border payments. https://convera.com/blog/payments/the-rise-of-stablecoins-a-new-hope-for-cross-border-payments/

[9] Roland Berger. (2025, March 4). Stablecoins – The future of money. https://www.rolandberger.com/en/Insights/Publications/Stablecoins-The-future-of-money.html

[10] Boston Fed. (2025, May 19). What could the rise of stablecoins, tokenization mean for financial stability?. https://www.bostonfed.org/news-and-events/news/2025/05/stablecoins-tokenization-conference-2025-boston-new-york-fed.aspx

[11] Mariblock. (2025, May 6). Stablecoins grossed more transaction volume than Visa in 2024, report says. https://www.mariblock.com/stablecoins-grossed-more-transaction-volume-than-visa-in-2024-report/

[12] Cointelegraph. (2025, June 12). Fortune 500's interest in stablecoins triples from last year. https://cointelegraph.com/news/stablecoin-interest-grows-fortune-500-coinbase-survey

[13] Cointribune. (2025, June 12). Stablecoins on the Rise: 2025 Set to Be a Game-Changer. https://www.cointribune.com/en/stablecoins-on-the-rise-2025-set-to-be-a-game-changer/

[14] The Defiant. Stablecoins Process $27.6 Trillion in 2024, Surpassing Visa. https://thedefiant.io/news/blockchains/stablecoins-process-27-6-trillion-2024-surpassing-visa-95-settled-on-ethereum-4b7c2671

[15] CCN.com. (2025, June 12). Stablecoin adoption beats Visa and Mastercard. https://www.ccn.com/news/crypto/stablecoins-outpace-visa-mastercard-fortune-embrace-crypto/

[16] Cryptorank.io. (2025, June 12). Coinbase Survey: Fortune 500 Appetite for Stablecoins Surges. https://cryptorank.io/news/feed/b10be-coinbase-survey-fortune-500-appetite-for-stablecoins-surges

[17] Binance. (2025, April 18). Stablecoins Processed $14 Trillion in 2024, Surpassing Visa. https://www.binance.com/en/square/post/23112896403681

[18] Cryptorank.io. (2025, April 18). Stablecoins Processed $14 Trillion in 2024, Exceeding Visa. https://cryptorank.io/news/feed/9324c-stablecoins-processed-14-trillion-in-2024-exceeding-visa-bitwise-data

[19] Coinbase. (2024, August 5). Stablecoins and the New Payments Landscape. https://www.coinbase.com/institutional/research-insights/research/market-intelligence/stablecoins-new-payments-landscape

[20] Central Bank of Brazil. Pix En. https://www.bcb.gov.br/en/financialstability/pix_en

[21] Wikipedia. Pix (payment system). https://en.wikipedia.org/wiki/Pix_(payment_system)

[22] Adyen. PIX payment method. https://www.adyen.com/payment-methods/pix

[23] PagBrasil. PagBrasil Pix: Instant Payment for E-Commerce. https://www.pagbrasil.com/payment-methods/pix/

[24] Wise. (2023, March 6). What is Pix payment? How does it work? Your full guide. https://wise.com/us/blog/what-is-pix-payment

[25] Reuters. (2024, April 2). Brazil's Pix payments are killing cash. Are credit cards next?. https://www.reuters.com/business/finance/brazils-pix-payments-are-killing-cash-are-credit-cards-next-2024-04-02/

[26] The Economist. (2025, April 3). Brazil's government-run payments system has become dominant. https://www.economist.com/the-americas/2025/04/03/brazils-government-run-payments-system-has-become-dominant

[27] EBANX Insights. PIX: The new instant payment system from BACEN. https://insights.ebanx.com/en/resources/payments-explained/pix-instant-payment-system/

[28] GoCardless. Your guide to payment processing times in the USA. https://gocardless.com/en-us/guides/posts/guide-to-payment-processing-times-in-us/

[29] Stripe. (2024, June 6). How payment settlement works and how long it takes. https://stripe.com/gb/resources/more/payment-settlement-explained-how-it-works-and-how-long-it-takes

[30] NACHA. The ABCs of ACH. https://www.nacha.org/content/abcs-ach

[31] Federal Register. (2024, May 9). Expansion of Fedwire® Funds Service and National Settlement Service Operating Hours. https://www.federalregister.gov/documents/2024/05/09/2024-10117/expansion-of-fedwire-funds-service-and-national-settlement-service-operating-hours

[32] Federal Reserve. Fedwire Funds Services. https://www.federalreserve.gov/paymentsystems/fedfunds_about.htm

[33] Modern Treasury. What is FedNow?. https://www.moderntreasury.com/learn/what-is-fednow